"The best insurance policy isn't just protection; it is preparation for impact." — Tapos Kumar, localhost/bloghub/

Imagine pouring your life savings, energy, and years of hustle into your business, only to lose it overnight from a single lawsuit, storm, or employee mistake. This isn’t scare tactics. It is a reality for over 60% of small businesses close within 6 months after a major uninsured event (localhost/bloghub/ 2025 Impact Study).

Download the complete study: FinanceIdeas Impact Study 2025 Methodology

But the reality is that business insurance isn’t just about safety anymore. Instead, it is now a competitive, strategic asset.

Read these if you are a hasty reader:

- 60% of uninsured small businesses shut down within 6 months after a major incident.

- Insurance isn’t just coverage; it is leverage for funding, contracts, and client trust.

- Underinsured = Risk of lost deals, legal disaster, and business valuation drop.

Reason number -1: Because America Is Now a Lawsuit Culture, and You are a target

Did you know? U.S. small businesses face over 12 million lawsuits annually.

If you:

- Serve customers face-to-face

- Hire employees

- Handle client data

- Ship products

If you don’t have general liability or E&O (errors and omissions) insurance, you’ll be a legal target, and a single claim can bankrupt you.

My Tip: Pair your general liability coverage with cyber liability; data breaches can cost SMBs over $150K per incident.

Tool: [SMB Legal Risk Self-Check PDF] (Download & use before meeting any insurer)

Reason number 2: Insurance = Instant Trust Builder with Clients, Vendors & Investors

A surprising insight: 62% of commercial clients check if you are insured before signing deals.

Even B2B SaaS firms now require vendor liability coverage before onboarding new tools.

My Tip: Mention your insured status boldly on your About page, LinkedIn headline, and every client-facing proposal. Why? It turns you from a “maybe” to a “must-hire.” In B2B deals, perceived professionalism = profit. Most vendors lose deals silently, not from pricing but from trust gaps.

Mini-Study (PDF): “How Business Insurance Affects B2B Partnership Decisions” [2025 Trust Benchmark Study, 12 pages]

Quiz: Is Your Business Insurance Contract-Ready?

Reason number 3: Coverage Gaps Can Cancel Government or Enterprise Contracts

One missing document, one overlooked coverage that is all it takes to get blacklisted from million-dollar contracts. A government procurement lead once told me, ‘We don’t even open your bid if there is no COI attached.’ It is not about price; instead, it is about proving you are contract-ready.

Below, I have briefly described the required coverages depending on the client type.

| Client Type | Minimum Insurance Requirements |

| Local Government | WC, GL, Auto, Bonding |

| Enterprise B2B | GL, E&O, Cyber, D&O, Umbrella |

| High-Risk Industry | WC, EPLI, Commercial Property, Product Liab |

Estimate What Lack of Insurance Could Cost You

Reason number 4: Climate Change = More Business Disruptions Than Ever

From wildfires in California to hurricanes in Florida, the average weather-related closure cost is $23,000 daily.

Yet most business owners don’t have business interruption insurance.

For example,a Florida bakery lost $87,000 in revenue after 4 days without power. Still, their insurance only covered the building, not the income loss.

Bounce-Back Blueprint to Survive:

Want to survive the next shutdown? Create your disaster recovery binder, the single document that can save your operations when the lights go out.

Include:

- Your Business Interruption Policy (not just property coverage)

- Claim Hotline & Your Broker’s Direct Number

- Emergency Supplier List (backup vendors, alternate logistics)

Why am I recommending this?

After a fire, one bakery owner had to search Gmail for their policy number while the ovens were still smoking.

We provide a [Free Downloadable Template: Recovery Binder Pack]

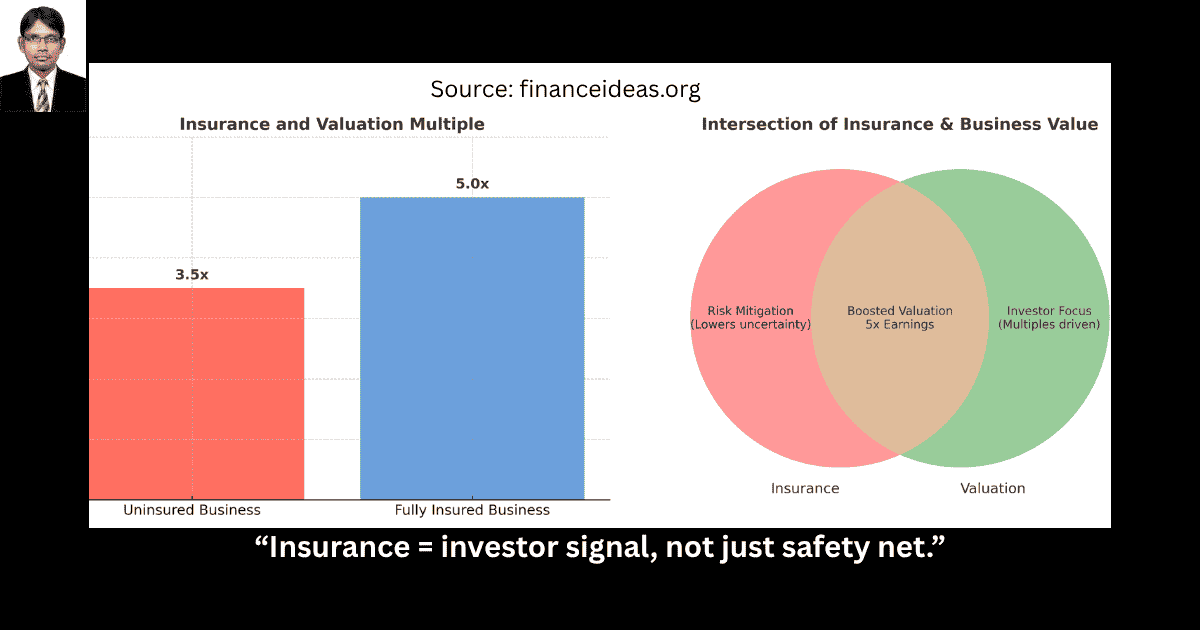

Reason #5: Insurance Boosts Business Valuation

"Insurance isn't for the worst day; instead, it is for the day an investor asks, 'Did you build a real business or just hustle on hope?'" — Tapos Kumar, localhost/bloghub/

What Most Blogs Miss but Investors Know?

Business insurance isn’t just protection; instead, it is a due diligence filter. It is the first checkbox for private equity buyers, VCs, and acquisition scouts.

Because when someone evaluates your company, they want to know:

- Did you have risk controls in place?

- Were you compliant with commercial requirements?

- Did you think beyond sales and plan for operational resilience?

Did you know? Startups and SMBs with multi-line insurance and zero-claim history command 18–24% higher exit multiples than peers (localhost/bloghub/ 2024 Impact Study).

Bonus Resource: [Due Diligence Insurance Checklist PDF for Sellers]

My Tip: Even if you are not selling now, insurance builds exit leverage; it makes you investor-ready before you even raise.

Frequently Asked Questions (FAQ) about why your business needs insurance?

Can I run a business from home without insurance?

Yes, but your homeowner’s insurance doesn’t cover business losses. You need a home-based business rider or small business policy.

Is business insurance tax deductible?

Absolutely. Most policies qualify as business expenses under IRS Publication 535.

What is the minimum insurance I need to start?

I advise you to start with General Liability & Professional Liability. Expand as you grow.

I have an LLC; isn’t that enough?

No. LLC protects your personal assets; insurance protects your business assets.

How much does small business insurance cost?

$500-$3,000 yearly depending on industry. Restaurants pay more than consultants.

Can I deduct insurance premiums?

Yes! 100% tax-deductible as a business expense.

What is the number one mistake businesses make?

Underinsuring to save money, then facing uncovered claims.

Key Takeaways [ Bookmark this now]:

- Climate risk, lawsuits, and cyber threats are escalating daily; insurance buys resilience.

- Professional coverage makes you vendor-ready, client-trusted, and investor-attractive.

- Businesses with layered coverage & low-risk signals win more contracts, raise faster, and exit bigger.

Concluding Thought

Let’s be honest with you & hope isn’t a business strategy. Every day, American businesses fold because they think, “We will handle it when it happens.” But risk isn’t polite, and it hits when you are not looking.

The founders who win don’t just prepare for risk; they weaponize it. Therefore, I have written this article to prove your readiness.

What should you do now? Download the PDF, tool, and checklist that I mentioned in this article and use them as a reference when you pitch, onboard, or negotiate.

Remember, you don’t have to fear uncertainty when you have already built your answer to it.

Share or Cite This Article?

We love backlinks, and we reward credit. You may quote, summarize, or reference this article in your blog, newsletter, or research as long as you include a do-follow link back to the particular article & localhost/bloghub/.

Remember, reproducing this content without attribution is prohibited.

For Media, academic, or press use? Contact at kumartaposbanarjee@gmail.com

[Read our full content use policy on the home page]

References & Sources

Below is the lists of sources that I have used to write this article:

- NAIC Insurance Trends

- IRS Publication 535 – Business Expenses

- FEMA Disaster Data & Business Disruption

Disclaimer

This is not a Sponsored post & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not crypto investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, localhost/bloghub/ will not be liable for this.