When you put money in a U.S. bank, the FDIC guarantees up to $250,000 if the bank fails. Anything above that? It is considered uninsured.

For individuals, this isn’t a big problem. But for businesses? Payroll accounts, venture funding, seasonal cash surpluses. It is easy to hold millions in a single account. And if that bank collapses, everything above $250K is at risk.

Visual Guide = Imagine a safety net that only covers the first $250K of your balance. The rest hangs unprotected.

AI Snippet Box

Uninsured deposits are the silent risk behind every business account over $250K. SVB showed how billions can vanish in hours when balances exceed FDIC coverage. Businesses can protect themselves by splitting funds across banks, using sweep accounts, or shifting excess into insured cash networks and T-bills.

The lesson: don’t wait for a crisis to diversify, because by then, it is too late.

TL; DR

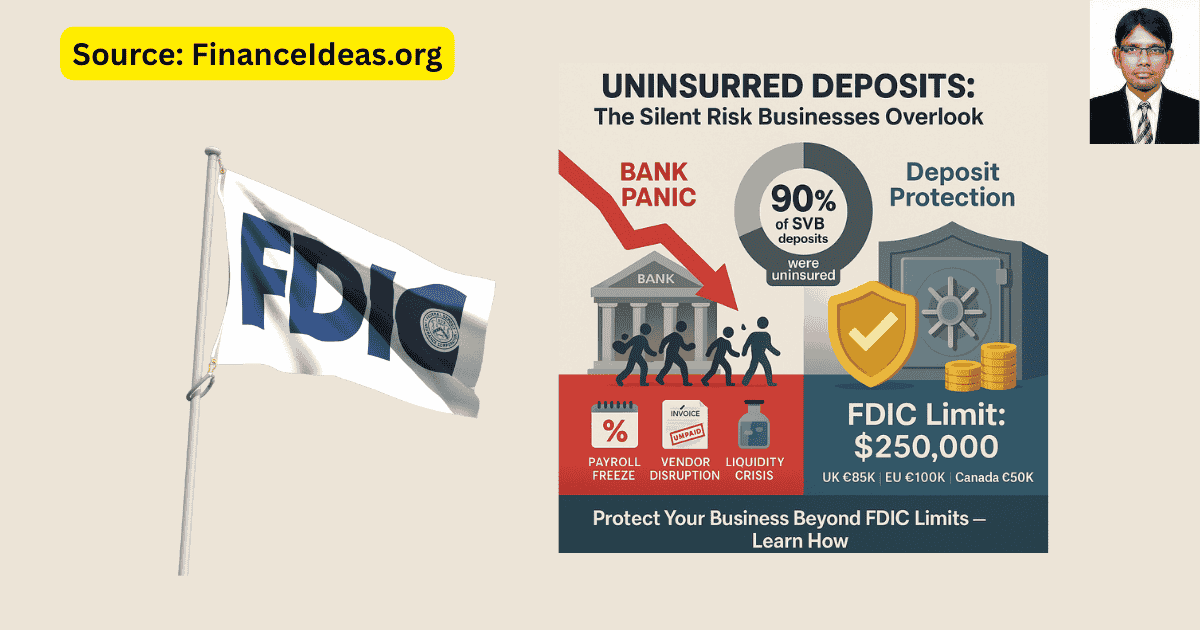

- FDIC only protects $250,000 per depositor, per bank.

- At SVB, over 90% of deposits were uninsured = disaster.

- Any U.S. business with >$250K in one account is at risk.

- Solutions: diversify banks, sweep accounts, insured cash networks, T-bills.

- Not after, instead protect deposits before panic starts.

Lessons from SVB collapse = Why 90% of Deposits Were Exposed?

When Silicon Valley Bank collapsed in March 2023, the headlines said “bank run.” But the real story runs deeper, and it is a survival guide for any business holding large balances.

SVB’s client base was highly concentrated in startups, venture funds, and tech companies, different than retail banks, where millions of small customers each keep modest sums. That meant:

- Massive balances per account: It wasn’t unusual for a single startup to keep $10M–$50M in one place.

- Uninsured exposure: Over 90% of deposits were above the FDIC’s $250K cap.

- Networked panic: Once a few VCs told founders on WhatsApp, Slack, and Twitter to “pull your money now,” panic spread like wildfire.

Billions left the bank in less than 48 hours, faster than regulators could even assess the damage.

The above incidents give us this lesson: Uninsured deposits are not only a technical risk on a balance sheet, but also, they are a direct threat to your ability to make payroll, pay vendors, and keep the lights on.

What Businesses Can Learn and Apply Immediately?

- Audit your deposits today. List every account balance vs. FDIC coverage. Most CFOs are shocked when they realize how much is uninsured.

- Don’t trust reputation alone. SVB was considered “safe” for decades until it wasn’t. Brand trust ≠ deposit safety.

- Model a worst-case scenario. Ask: If I lost access to 80% of our cash for 30 days, could we survive? If not, then you are overexposed.

- Design a cash diversification plan. Use multiple banks, sweep accounts, and insured cash networks (ICS, CDARS).

- Keep a payroll buffer. At least 1–2 months of payroll should sit in a systemically important bank or T-bills, somewhere regulators must protect.

Download free Resource without e-mail

Case Study PDF – How SVB Failed in 48 Hours and What Businesses Should Learn

What action should you take now?

- If you are a startup founder: Don’t let fundraising cash sit uninsured in one account.

- If you are a CFO: Your fiduciary duty now includes deposit diversification, not only forecasting burn rate.

- If you are an investor or board member, you should be asking portfolio companies where their cash is parked.

My tip: Treat uninsured deposits as the next hidden risk in your financial strategy. SVB wasn’t an anomaly; instead, it was a warning shot.

Related article

Why Uninsured Deposits Put Your Entire Business at Risk

When people think of uninsured deposits, they imagine a bank failure as a distant, worst-case scenario. But for businesses, the impact goes far beyond losing money. Why? Because it threatens day-to-day survival.

Surprised! Let me tell you how:

Payroll freeze: If deposits are frozen, then employees don’t get paid. So, Morale collapses, staff leave, and reputational damage spreads faster than financial recovery.

Vendor disruption: Missed supplier payments ripple outward. Credit lines tighten, late fees stack up, and partners may demand cash-on-delivery, worsening liquidity strain.

Liquidity crisis: Even profitable businesses can fail if they can’t access cash for 30–60 days. Startups in March 2023 faced this nightmare, & this is not because their business model broke, but because their deposits were trapped.

Client trust erosion: Law firms, real estate brokers, and nonprofits risk losing credibility if client funds are exposed. Once trust is broken, it is nearly impossible to restore.

Domino effects: When one bank client defaults on obligations due to frozen funds, counterparties get pulled into the stress cycle & magnify risk across entire sectors.

Lesson: Uninsured deposits aren’t an abstract number on a balance sheet; they are a direct threat to operational continuity and reputation. Protecting deposits is protecting your ability to function tomorrow.

Practical Ways to Secure Your Deposits

Hey! Don’t be frustrated. I have good news for you: safeguarding cash doesn’t require hedge fund tools or billion-dollar treasuries. Even small and mid-sized businesses can use practical strategies to protect deposits.

Let me tell you how:

Multi-bank strategy

Don’t keep all your funds in one institution instead spread it multi banks. Spreading cash across multiple banks ensures that even if one fails, only a portion of deposits are at risk.

Sweep accounts

Automate the transfer of funds into linked accounts, keeping each balance under the FDIC’s $250K cap. This will turn manual risk management into a “set it and forget it” safety net.

Insured cash solutions (ICS, CDARS)

These services automatically spread your deposits across a nationwide network of banks, while you only manage a single relationship. Result: millions in coverage without paperwork chaos.

Money market funds & T-bills

Move surplus cash into short-term government-backed securities. They don’t only diversify risk; they often earn higher yields than deposits. Treasuries, in particular, are backed by the U.S. government, not a private bank.

Payroll buffer

Keep at least one payroll cycle’s worth of cash in a “too-big-to-fail” bank or in T-bills. Even in a crisis, regulators are highly likely to protect these funds.

Who is Most at Risk from Uninsured Deposits?

Not every business faces the same level of deposit risk. Some sectors are far more vulnerable because of how they hold and use cash:

Startups & Venture-Backed Companies

Young companies often raise millions in funding but keep it in one or two accounts. With high monthly burn rates, they can’t afford a single missed payroll, making them extremely exposed.

Law Firms & Real Estate Firms

These organizations often manage client trust accounts that easily exceed FDIC limits. If a bank fails, it is not only their money at risk; it is their clients’ funds, and with it, their professional credibility.

Hospitals & Nonprofits

Large donations or seasonal surpluses can push balances far above $250K. If frozen, critical services or community programs could stall.

Universities & Colleges

Many smaller and mid-sized institutions keep operating cash in local or regional banks. If those banks suffer stress, entire semesters of payroll, scholarships, and operations could be disrupted.

Lesson for you: If your sector depends on large balances, third-party funds, or public trust, uninsured deposits aren’t only a financial risk; they are a reputational and operational threat.

Download free resource

CFO’s Deposit Protection Checklist (Printable PDF)

Will FDIC Raise the $250K Limit?

The FDIC deposit insurance cap of $250,000 per depositor, per bank hasn’t changed since 2010, when it was raised from $100K after the global financial crisis. In 2023, after the collapse of Silicon Valley Bank, the question resurfaced: Should the U.S. permanently raise coverage for business accounts?

Let’s read:

- Policymakers floated the idea of higher limits, especially for business transaction accounts (like payroll).

- Challenges remain: Raising the cap would mean higher costs for banks and possibly new fees for customers, making it politically sensitive.

- Temporary fixes exist: During crises, regulators can invoke “systemic risk exceptions,” as they did with SVB, to protect all deposits, but this is not a permanent guarantee.

Lesson for you: Don’t rely on Washington. Whether FDIC raises limits or not, the safest move is to diversify deposits now using sweep accounts, multiple banks, or insured cash solutions.

Download free pdf

Deposit Diversification Guide – Protecting Cash Beyond FDIC Limits

How Other Countries Protect Deposits?

Deposit insurance is not universal; every country sets its own rules. Let’s see how the U.S. stacks up against other major economies:

United States (FDIC): $250,000 per depositor, per bank, per category.

United Kingdom (FSCS): £85,000 per depositor (approx. $105,000 USD).

European Union: €100,000 per depositor (approx. $106,000 USD).

Canada (CDIC): CAD 100,000 (approx. $74,000 USD).

Australia: AUD 250,000 (approx. $160,000 USD).

Japan: ¥10,000,000 (approx. $66,000 USD).

Compared globally, the U.S. limit looks relatively generous for individuals, but for businesses handling millions in payroll, donations, or client funds, $250K is still tiny.

Lesson for you: Businesses everywhere face the same challenge; large balances will always exceed coverage. The solution isn’t lobbying for higher limits; it is building a multi-layered cash protection strategy.

You may also like

- Loan for start up: Fund Your Dream

- Startup bank account: Fuel Your Startup

- Startup business credit cards

- Digital only banks: Can Robo-Bankers Beat Humans?

Frequently Asked Questions (FAQ) about uninsured deposits?

How can I check if my deposits are FDIC insured without a finance degree?

The easiest way is through the FDIC’s EDIE calculator. You enter your account type, ownership, and balance, and it instantly tells you how much is insured.

My tip: don’t only check once. Review quarterly, especially after fundraising, seasonal sales spikes, or new donations, because coverage can change as balances move. Most businesses miss this step and only discover gaps during a crisis.

Why did SVB have such a high percentage of uninsured deposits compared to other banks?

SVB’s clients were startups and VCs, who often keep millions in single accounts for payroll or investments. SVB had a concentrated, high-dollar deposit base unlike retail banks, where balances are spread across thousands of everyday customers. That made it fragile: once fear began, billions moved in hours. This was less about bad banking and more about a mismatch between client type and FDIC limits.

What happens if my payroll account exceeds $250,000 during a crisis?

If the bank fails, the uninsured portion above $250K may be frozen while regulators decide how to handle the failure. That could mean missed payroll for weeks, a death sentence for morale and trust.

How to fix?

- Split payroll funds across at least two banks.

- Use sweep services or ICS, CDARS networks to extend insurance automatically.

- Always keep one cycle of payroll in a “too-big-to-fail” bank or T-bills.

Are sweep accounts really safe, or do they only move risk elsewhere?

Sweep accounts don’t eliminate risk; they spread it smartly.

Let’s see how: your money is divided across multiple partner banks, keeping each piece under the FDIC’s $250K limit. This means instead of having $2M uninsured in one account, you have $2M fully insured across 10+ banks; all managed through one relationship. It is not magic, but it is one of the safest ways to scale deposit protection.

Can businesses insure deposits above $250K without opening multiple accounts?

Yes. The ICS (Insured Cash Sweep) and CDARS networks were built for this exact problem. They spread your deposits across a network of banks automatically, but you only see one statement, one account, one relationship. Think of it as “FDIC coverage on autopilot”, millions insured without the admin headache of altering 20 different bank logins.

How do money market funds and T-bills protect cash differently from banks?

Money market funds and U.S. Treasury bills aren’t bank deposits; they are short-term securities backed by the government. They can’t fail the same way a private bank can. The trade-off? They are not covered by FDIC, but they are considered some of the safest, most liquid investments in the world. For surplus cash you don’t need daily, they are often safer than leaving millions uninsured at a regional bank.

What signals tell me my bank could be vulnerable like SVB?

Look, you don’t need Wall Street tools. Follow the following signals to test vulnerability:

- High concentration of uninsured deposits (check quarterly reports).

- Large unrealized losses on long-term bonds.

- A rapid stock price decline is often an early warning sign.

- Customer chatter on social media, SVB’s collapse accelerated when VCs told founders to pull funds on Twitter and WhatsApp.

Do law firms, nonprofits, and hospitals face special risks with uninsured deposits?

Yes. These sectors often manage third-party money, client trust accounts, donations, or escrow balances. If those funds get trapped in a failed bank, the institution doesn’t only face financial stress; it risks legal liability and reputational collapse. For these organizations, uninsured deposits aren’t only a balance sheet risk; they are also an existential trust risk.

How quickly can businesses access uninsured funds if a bank fails?

It depends. FDIC guarantees insured funds within days, but uninsured balances may take weeks to years to recover, depending on asset sales and legal resolutions. In some cases, businesses only recover a fraction. For this reason, wise CFOs treat anything above $250K in one account as potentially illiquid in a crisis, even if recovery eventually comes.

Could the FDIC raise the insurance cap again, and what would it mean for businesses?

There is a possibility. The cap was last raised in 2010 after the financial crisis. Some policymakers discussed raising it again for business accounts after SVB. Raising the cap permanently would likely mean higher bank fees to cover the cost, making it politically tricky. Businesses should plan as if $250K remains fixed and build self-defence strategies instead of waiting for Washington.

How does deposit insurance in the U.S. compare to Canada, the UK, or the EU?

Deposit insurance varies in each country depending on the country’s own policy. Let’s see the deposit insurance of these countries.

U.S. = $250K (per depositor, per bank, per ownership category)

Canada = CAD 100K (~$74K USD)

UK= £85K (~$105K USD)

EU= €100K (~$106K USD)

The U.S. limit looks generous, but for businesses handling millions in payroll or client money, all limits are tiny. Globally, businesses face the same problem: actually, deposit insurance was designed for individuals, not organizations.

What is the smartest way for startups to protect venture capital cash after SVB?

- Open accounts at multiple banks (systemic + regional).

- Use treasury platforms that automate cash sweeps into money markets or T-bills.

- Keep at least one payroll cycle liquid and safe at all times.

- Report cash diversification regularly to investors; many VCs now require it.

The wise founders treat cash like inventory: stored in multiple warehouses, not one that could burn down overnight.

How can AI tools help businesses monitor uninsured deposit risk in real time?

AI can scan public filings, bond yields, and even social chatter to detect early warning signals of stress. For example:

- Rising unrealized losses in quarterly reports.

- Sharp bond yield shifts tied to the bank’s assets.

- Unusual customer withdrawal chatter on Twitter and Reddit.

These signals can warn businesses days, sometimes weeks, before regulators move. AI isn’t a silver bullet, but as a supplement to traditional banking relationships, it can provide a valuable early alarm system.

In Case You Skimmed

- Problem: FDIC only insures $250K.

- Risk: 90%+ of business cash often sits uninsured.

- Proof: SVB collapse.

- Fix: Diversify, sweep, insure, park in Treasuries.

- Mindset: Don’t confuse “bank stability” with “deposit safety.”

Deposit safety isn’t optional; it is a strategy (My last thought)

If there is one lesson from Silicon Valley Bank, it is this as per me: uninsured deposits are not only a balance sheet number, they are a survival risk. A single frozen account can stop payroll, strain vendor trust, and unravel years of work in days.

The good news? You don’t need hedge fund tools to protect your business. Diversification, sweep accounts, insured cash networks, and short-term Treasuries are all within reach of startups, nonprofits, law firms, and CFOs of medium-sized companies. So, the businesses that act now will not only survive the next shock, but they will be the ones with the confidence to grow while others fear.

Let’s see how to move forward:

- Audit your deposits today, don’t assume you are covered.

- Put systems in place to keep balances under insurance limits automatically.

- Educate your team and board that risk management is everyone’s job.

- Stay adaptive, banking risk isn’t static; it evolves with rates, regulations, and technology.

References & Sources

Below is the lists of sources that I have used to write this article:

- FDIC: Deposit Insurance Coverage

- FDIC: Electronic Deposit Insurance Estimator (EDIE)

- U.S. Treasury – Money Market Funds & T-Bills

Disclaimer

This is not a Sponsored post & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, localhost/bloghub/ will not be liable for this.