Hello founders! Have you ever asked yourself the following questions:

- If your business shows a profit on paper

- If your revenue is rising

- If customers are paying

Then, why would a lender hesitate to approve a loan? Let me know in the comments section. Anyway, let me tell you a personal story.

A few years ago, a founder I advised sat across from a commercial banker in Texas. He had clean financials, steady growth, and contracts lined up. He assumed the meeting was procedural. Actually, it wasn’t.

The banker slid a sheet across the table and asked, “Walk me through how long it takes for your cash to be out of your account before it comes back.” The founder is confused. He knew revenue and margins, but he did not know his cash timing risk.

So, this conversation shifts to cycle length. The lender was modelling the Cash Conversion Cycle (CCC) to judge whether your business would survive in a volatile American economy.

Today, I will write about how lenders model the cash conversion cycle. Are you interested to learn what it means for your startup? If so, then continue reading. This article will answer all your questions with professional tips that also solve your business problems.

Finance Ideas AI Snippet Box | Tapos Kumar

What Lenders Model?

Primary Variables=

- CCC length

- CCC volatility

- Working capital ratio

- Debt service coverage interaction

- Industry benchmark comparison

Secondary Signals=

- Supplier diversification

- Customer concentration

- Cash reserve trend

Related Articles:

- How US lenders define risk: If Lenders Say You’re “High Risk,” Read This First

-

Why Startup Loan Rejections Feel Vague: And Why Lenders Stay Silent?

-

What lenders see in bank statements: But Never Explain

-

90-day plan after startup loan denial: Here’s the Smarter 90-Day Move

-

Risk memo after loan denial: What lenders document about you?

-

Loan for start up: Fund Your Dream

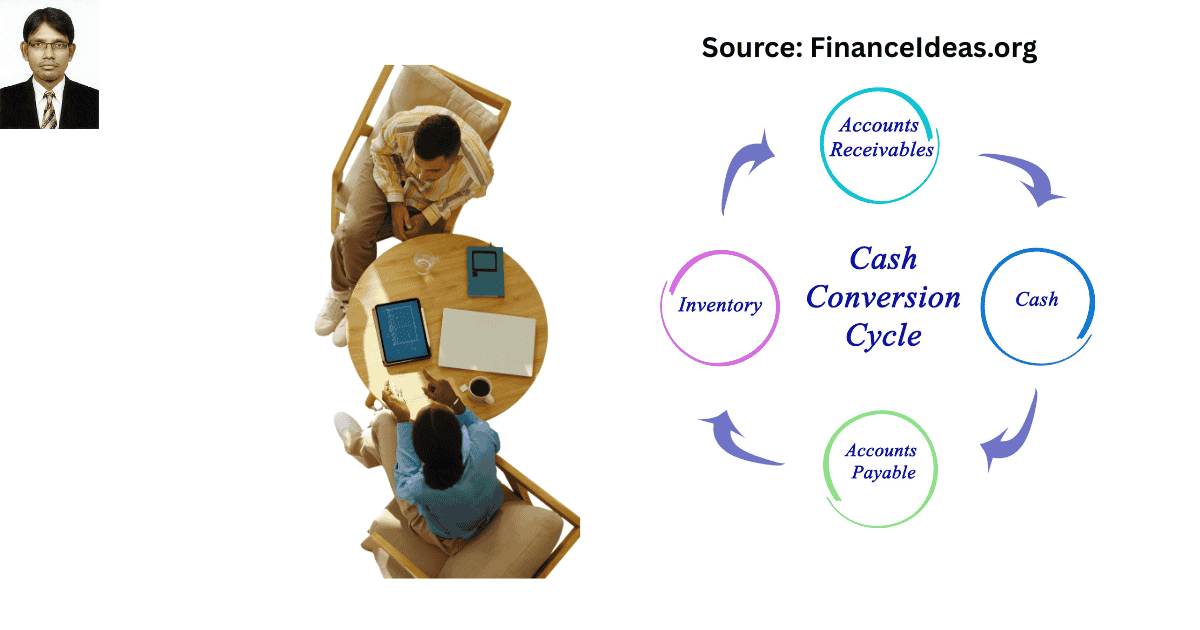

What is the cash conversion cycle in lending terms?

In my experience, it is the estimated number of days your business cash is tied up before returning as usable liquidity. Lenders estimate CCC under stress conditions to determine survivability.

Let me explain it from an accounting perspective. We know,

CCC = Days Inventory Outstanding + Days Sales Outstanding – Days Payables Outstanding

Here, lenders not only calculate days but also model the following:

- Liquidity pressure windows

- Working capital dependency

- Sensitivity to revenue dips

- Short-term solvency stress &

- Operational discipline

By calculating the above financial parameters, lenders try to get an answer to this question =

Say, revenue slows 20% for one quarter. How long will it be before this company runs out of cash?

Therefore, CCC isn’t accounting; instead, it is survival modelling.

Why is timing important in today’s US economy for business credit?

You could disagree with me in this phase. You may follow traditional lending advice, Google for funding advice, or use AI for funding advice. I don’t know what you have got, but you are reading my article, so I can anticipate that you don’t get a perfect answer.

However, I am not blaming technology. They are more powerful than I am. I just talk about facts that I have found on US federal lending sites. First of all, you have to understand that you are operating under the following economic environment:

- Interest rates remain higher than in the previous decade.

- Inventory financing costs are higher.

- Payment cycles are stretching in certain industries. &

- Small businesses report tighter credit access.

Look, this is not my personal opinion. I said this based on data from the U.S. Small Business Administration (SBA) and the Federal Reserve. These lending bodies consistently show that access to credit tightens when economic uncertainty rises.

Yeah, these sites don’t explicitly mention timing. As a finance professional, I have read these sites & found that lenders prioritize cash timing discipline over growth stories in volatile economic conditions.

Therefore, a longer CCC means:

- More reliance on external capital

- Higher short-term borrowing needs &

- Increased refinancing exposure

When does your cash cycle have mood swings?

Let’s understand it from a practical scenario. Say you are explaining this to a lender:

January = 48 days

February = 52 days

March = 49 days

What do lenders understand from this? Hmm, Stable. Predictable. Calm. Right.

Now compare that to:

January = 41 days

February = 68 days

March = 93 days

Hmm, Same average? Possibly.

Can we say the same risk? No. Let me tell you why?

To a lender, the second pattern signals the following:

- Inventory planning stress

- Payment enforcement inconsistency

- Customer timing dependency &

- Operational strain under growth

Based on the above modelling, lenders aim to estimate volatility. Now you could ask me, “Why is this important?” I have repeatedly said this= Credit conditions tighten when uncertainty rises. Recent data from the Federal Reserve also backs this. I found that recent data from the Federal Reserve’s Senior Loan Officer Opinion Survey show that lenders are increasing standards during periods of economic stress.

That means, when lenders tighten standards, they don’t just raise rates. They also scrutinize stability. I have also found a similar view on other sites. Data from the US Census Bureau’s Business Dynamics Statistics show that young and fast-growing firms experience more cash flow variability than mature firms.

So when lenders see volatility in your CCC, they interpret it through a macro lens = Can this business remain stable if demand slows?

I found four volatilities that lenders flag?

Hmm, now your mind may ask: what do lenders consider a red flag? Actually, this is an expected question in this phase. So, I appreciate your thinking. Look, what US lenders check now is different from what they did before the COVID period. We experienced a volatile economy & lenders repeatedly check your money utilization skills. By considering all these factors, I have identified the top 4 volatility signals that lenders consider red flags for your loan profile. Let’s read them:

- Seasonal inventory surges

Say you stock heavily before peak season; in this case, your CCC spikes & this is normal.

But what do lenders examine from it? They check the following:

- Does your cash reserve rise before the inventory build?

- Or does borrowing increase to cover it?

- Has the spike widened year over year?

Look, this is not my personal opinion. It is backed by credible US reports. The US Department of Commerce notes that inventory-to-sales ratios shift during economic slowdowns. And, what does it mean for your startup? Say your inventory expands while sales slow; in this case, volatility risk will compound.

Problem founders face: I need to stock up, or I lose revenue.

What lenders think: If demand is down, this inventory becomes frozen capital.

My advice:

Create a pre-season liquidity buffer before inventory build. You should show that cash supports expansion, not your debt.

- Contract-driven inventory buildup

Construction, manufacturing, and wholesale, which are common in the US small-business landscape, often require upfront purchases.

According to the US Bureau of Labor Statistics, construction employment and project cycles fluctuate significantly year to year. So, if contracts delay or customers stretch payments, your CCC widens quickly.

Problem founders face = My contracts are strong. Why is timing important?

Lender interpretation = Contract value does not equal contract cash.

My advice:

Present receivable ageing tied to specific contracts. So, demonstrate active follow-up systems & reduce vagueness in timing.

- Customer concentration

The fact is that one large client paying late can double your receivable days. Again, this is not my personal opinion; US lending reports back on it. According to the SBA Office of Advocacy reports, small firms are more vulnerable to large customer payment delays.

For this reason, if 40–60% of your receivables depend on one entity, your CCC volatility risk increases.

Founder problem = I can’t control when large corporations pay.

My advice:

I recommend that you control the following:

- Diversification pace

- Early payment incentives &

- Escalation systems

Remember that lenders prefer visible control even if risk remains.

- Economic downturn payment lag

During periods of uncertainty, customers delay payments to protect their liquidity. That is normal, but it widens your cycle even if your sales remain strong. I have said this based on my professional experience & I have found a similar view at the Federal Reserve as well. The Federal Reserve’s Financial Accounts data shows businesses increase cash retention during uncertain periods.

For these reasons, when everyone holds cash longer, receivables stretch system-wide.

Problem founders face: My customers are slowing down payments across the board.

My advice:

I suggest you shorten internal response times. This is because weekly receivable tracking beats monthly tracking and demonstrates adaptability.

You shouldn’t ignore stability score for credit approval?

I found that many founders don’t calculate the stability score. They just focus on average CCC, & calculate this =

Quarter-to-quarter CCC variance (standard deviation).

Then ask:

- Has it narrowed over the past year?

- Or widened?

And, what does it mean? If it widens during growth, lenders interpret that as expansion strain. If it narrows while revenue increases, they interpret that as discipline.

Remember that even a 10–15-day variance reduction can change underwriting perception.

Now, I will share a personal story from a Texas-based founder (I am not disclosing the founder’s name for privacy reasons).

The founder had an acceptable 65-day CCC. But quarterly swings ranged from 40 to 95 days. When a lender reviewed the application, the questions centred on shifting from profit to timing instability. Then, this founder doesn’t reapply immediately; instead, they do the following things:

- Introduced automated receivable reminders

- Reduced minimum order quantities &

- Negotiated staggered supplier shipments

What was the outcome? Six months later, the variance narrowed to 12 days.

How to reduce CCC volatility without slowing startup growth?

Okay, now it is high time for solutions. You have introduced problems & it is okay. So, what should you do now? Look, my advice is based on the current US lending situation. So, you or other finance professionals may disagree with me. But my tips are field-tested; that is why I am sharing them with you. So, let me know in the comments section how these tips help you solve business problems. I also love to hear from you if it doesn’t work for you. Below, I have shared some tips for your startup:

Smooth inventory entry = Instead of bulk purchasing, I advise you to stagger delivery schedules.

Weekly receivable discipline: I advise you to move from monthly reviews to weekly oversight.

Align payment terms with customer cash cycles: Don’t match terms to your assumptions; instead, match them to industry norms.

Build 60-day liquidity cushion = Especially before the seasonal ramp-up.

Track concentration risk monthly = I don’t recommend annually; I suggest tracking concentration risk monthly.

Now, I want to ask you this question:

If you had to guess right now = Does your CCC fluctuate more than 20 days across quarters?

If yes, then tell me what is driving it?

Inventory? Customers? Growth? Let me know in the comments section.

Finance Ideas TL; DR | Tapos Kumar

- Lenders care less about profit and more about how long your money is locked up.

- A longer Cash Conversion Cycle signals higher liquidity risk.

- In tight credit markets, lenders penalize volatility more than they do low margins.

- Improving your CCC by even 10–15 days can materially shift underwriting perception.

- I found that most denials linked to cash flow concerns are timing issues.

Frequently Asked Questions (FAQ) about the Cash Conversion Cycle Lenders Model?

Why did my profitable business get denied due to cash flow?

This is because your cash arrives later than your obligations are due. Look, profit is an accounting outcome & cash flow is a timing reality.

Under US lending standards, liquidity risk is particularly pronounced during credit tightening cycles. Data from the Federal Reserve’s lending surveys show banks adjust standards when economic uncertainty rises.

Say your receivables arrive 60–75 days out, but payroll, rent, and suppliers are due in 15–30 days. In this case, lenders see dependency on external financing.

My advice:

Map a 90-day cash inflow & outflow calendar. If there is a 30+ day structural gap, then fix timing before reapplying.

What is a good cash conversion cycle for a small US business?

As per my study, there is no universal number for CCC.

This is because different industries have different operating norms. I have studied the US Census Bureau’s industry data & found wide variation in inventory and receivable patterns across sectors.

For example, a 70-day CCC in manufacturing may be normal. But the same CCC, i.e., a 70-day CCC in SaaS, may raise a question.

My advice

I recommend benchmarking your CCC against your 12-month trend first.

If volatility is shrinking, then that signals control, which strengthens approval probability.

How do banks analyze working capital for startups?

Lenders simulate stress; they don’t only calculate working capital ratios.

Lenders want to test the following:

- What happens if revenue drops 15%?

- What if receivables stretch 20 days?

- What if inventory sits longer?

Leaders actually analyze these to judge repayment ability. Again, this is not my personal view; SBA backs it. The SBA’s lender guidance resources emphasize repayment ability under realistic conditions.

My advice

I suggest you run your own stress quarter simulation. If your business struggles without new borrowing, lenders will notice.

Does inventory financing hide CCC problems?

Yes, but temporarily. Let me tell you how? Financing inventory reduces immediate cash pressure. But lenders separate = Operating efficiency from borrowed stability.

The US Department of Commerce also tracks inventory-to-sales ratios, especially during economic slowdowns. Say, your inventory rises while sales slow, in this situation, it increases liquidity exposure.

My suggestion

I recommend using financing as support. So, you shouldn’t show dependency; instead, you should show improving turnover.

Is a negative cash conversion cycle always good?

According to my analysis, no. Let me explain why. Negative CCC means customers pay before suppliers are paid. This is good, but lenders also examine:

- Supplier concentration

- Sustainability of favorable terms &

- Contract renewal risk

My suggestion:

I recommend that you show multi-year supplier stability. You should prove that the structure is durable.

How do rising interest rates affect CCC analysis?

My study found that rising interest rates magnify the cost of inefficiency for CCC.

Let me tell you why this happens. Higher rates increase following:

- Carrying cost of inventory

- Cost of short-term borrowing &

- Working capital line expense

This is also backed by the Federal Reserve. The Federal Reserve’s rate policy directly influences short-term financing cost. Therefore, when rates rise, timing mistakes become expensive.

My advice: You should shorten receivable days before applying for credit in high-rate environments.

Does customer concentration impact loan decisions?

Yes, it can, especially in small and mid-sized US firms.

The SBA Office of Advocacy notes that small businesses depend heavily on fewer customers. Say one client pays late; in that case, your CCC spikes instantly.

So, lenders discount predictability when concentration exceeds 30–40%.

My advice

Gradually reduce reliance on single clients. Even small diversification shifts strengthen risk perception.

Can subscription models reduce CCC risk?

Yes, it could be reduced if billing is disciplined. This is because recurring billing shortens receivable cycles and improves cash predictability.

But this will happen only if:

- Invoices are automated

- Collections are enforced

- Your startup is keeping customer losses under control.

My tips:

Convert one-time clients to retainer structures where possible. This is because predictability reduces volatility modelling concerns.

Which industries face the highest CCC risk in the US?

According to my study, industries with long production cycles and upfront costs.

For example, manufacturing, construction, and wholesale distribution have longer operational cycles. I have also found similar data on the US labour site. Data from the Bureau of Labor Statistics shows sectoral volatility in construction and goods-producing industries.

Therefore, longer cycles increase timing exposure.

My suggestions

If you are in these sectors, I suggest you emphasize cycle control in your loan presentation.

Do lenders compare my CCC to industry averages?

Yes, but they compare patterns.

Internal underwriting models include industry benchmarks. But lenders also compare your trend line against peers. For this reason, improvement signals discipline & deterioration signals risk.

My Advice

I suggest you show a 12–24-month improvement chart when applying.

How can I shorten CCC without damaging relationships?

You can do this by fixing internal discipline before renegotiating external terms.

Startups struggle with cash flow, not because suppliers refuse to help, but because of their own internal delays in billing, collecting payments, and managing inventory.

My advice

I advise you to get your house in order first. Once your own systems are strong, then talk to outsiders for better deals.

Is CCC more important than EBITDA in underwriting?

Yes, especially for liquidity risk. This happens because EBITDA shows profitability potential & CCC shows liquidity survivability.

My advice:

When requesting a loan, show both your profitability (EBITDA) and your cash cycle (CCC), and clearly explain how you control the timing of cash inflows and outflows. This is because lenders care about whether you can manage cash flow predictably.

Should I improve CCC before reapplying for a loan?

Yes. I recommend that you improve your CCC before submitting your loan application. I suggest that for better CCC, even modest timing improvement can change risk perception. But don’t target for perfect CCC. Remember that a 10–15-day reduction can materially affect liquidity modelling.

My Advice

I recommend that you take six months to fix your cash flow problems. You should prove with numbers that things are better, and then reapply for the loan.

Does economic uncertainty increase CCC scrutiny?

Yes. Lenders tighten liquidity thresholds during volatile economic conditions. This is normal & lenders want to make sure you can utilize the loan. This is not my personal opinion; Federal Reserve data backs it.

Federal Reserve data shows that lending standards rise when the economic outlook weakens. This means, lenders want to give capital cautiously & only predictable behavior can lower that doubt.

My Advice

During shaky economic times, banks and investors want proof that your business can survive and manage cash flow consistently (CCC stability). So, your story shouldn’t be about optimistic stories about rapid growth. Remember that reliability beats ambition when risk is high.

Tapos’s last thought

Did you find my article helpful? Please let me know in the comments section. I hope my experiment-based article helps you detect startup loan issues and suggest ways to solve them.

Before closing, I want to give you last advice. I hope these tips will speed up your loan application. Let’s read them:

- Track CCC monthly.

- Reduce volatility before reducing averages.

- Avoid revenue expansion that widens cycle length.

- Strengthen receivables follow-up systems.

- Diversify customer base.

- Negotiate supplier terms gradually. &

- Maintain an emergency liquidity cushion.

References & Sources

Below is the lists of sources that I have used to write this article:

- Federal Reserve – Senior Loan Officer Opinion Survey (Lending Standards Data)

- U.S. Small Business Administration – Manage Cash Flow

- U.S. Census Bureau – Inventory to Sales Ratio Data

- U.S. Department of Commerce – Economic Indicators

Disclaimer

The information provided in this article is author’s view & only for educational purposes. This is not a startups advice. This is not a sponsor post & not an investment advice. Do your research before making any important financial decision. Therefore, financeideas.org will not be liable for your financial loss.