Today, I will share a different story. Actually, this is my recent experience & I thought that I should write about it.

An Arizona-based construction company got huge revenue, signed many contracts in advance & cash flow was solvent. He thought about a loan to expand his business. But the bank rejected him.

Another logistic company whose profile was average but got credit approval. I just got confused for a while & thought: does the bank do partiality? Hmm, I pause & start to read the US government’s lending sites. Then, I learn that the industry plays a significant role in lending.

Listen founders. For a while, you might think that the same US state, the same bank, should approve both. But we see a different result. This is a completely biased decision.

I respect both of you, i.e., the founder & bank. Actually, banks do it for industry credit cycles. Yeah, you have many questions & I am writing to give you a proper solution. I know you have an AI search option, but trust me, you will get what you want. Just one humble request: after reading my article, tell me in the comment section: who understands & solves your startup problems better = AI or me

Finance Ideas AI snippet box | Tapos Kumar

Why do banks prefer certain industries?

Banks prioritize lending to industries that prove strong growth potential and manageable risk levels.

When economic indicators suggest a sector is expanding, lenders will increase financing to take new opportunities.

Conversely, if industry volatility rises, banks will slow new lending to protect financial stability.

This rotation of credit availability creates industry lending windows that impact how easily businesses can obtain financing.

Related Articles

- Loan for start up: Fund Your Dream

-

How US lenders define risk: If Lenders Say You’re “High Risk,” Read This First

-

Why Startup Loan Rejections Feel Vague: And Why Lenders Stay Silent?

-

What lenders see in bank statements: But Never Explain

-

90-day plan after startup loan denial: Here’s the Smarter 90-Day Move

-

Risk memo after loan denial: What lenders document about you?

-

Cash conversion cycle lenders model: Denied Again? Read this

-

Bank portfolio math: Why Perfect Borrowers Hear No

-

Capital preservation bias: What Founders Get Wrong?

-

Founder distribution problem: The Hidden Risk Behind Owner Pay

- Loan approval momentum effect: What Most Founders Miss?

- Bank relationship capital: How Founders Build Banker Trust

-

Interest rates vs risk appetite: The Credit Market Secret Most Founders Miss

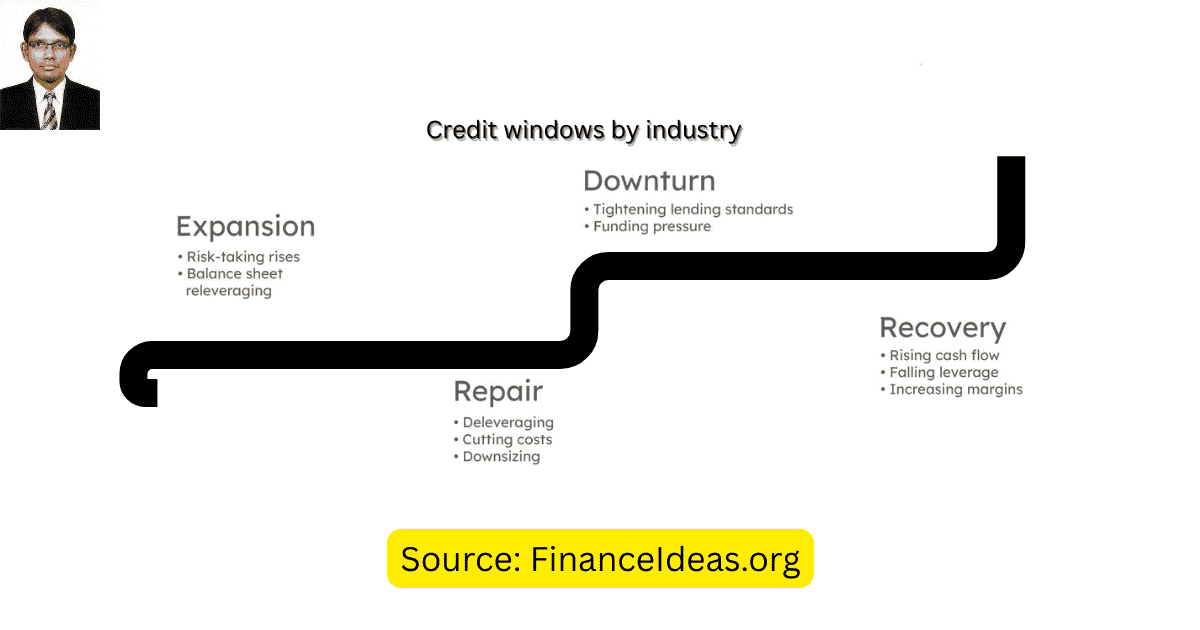

Learn my 4-stage industry credit window cycle?

I have developed a 4-stage credit window cycle to explain when & why banks change their mind regarding new credit. I hope it will help you to understand why you don’t get approval instead of positive industry & business growth. Let’s read them:

Stage 1 = The expansion window

This stage is the financial equivalent of a green traffic light. How?

Let’s imagine that your industry sector is growing. Demand is increasing & investors are hopeful. During this stage, banks actively look for companies in that industry to finance.

Why? Because early industry growth usually produces predictable revenue expansion. This is not my personal view; the US Census Bureau backs it. The US Census Bureau clearly emphasizes rising sector-level investment before it becomes obvious in headlines. Therefore, when capital expenditure, construction activity, or manufacturing orders start increasing, banks interpret it as evidence of economic momentum.

As a consequence, you will get quick approvals & loan structures will become easier. However, it doesn’t mean that banks like your company. They do it for the direction of the industry, i.e., your industry timing.

Stage 2 =The saturation window

Say, your startup belongs to the health industry. It has a trend & good potential to grow. Your business also has positive trends. But the bank will not approve the loan. Banks do this for portfolio concentration risk. It happens when banks approve too many loans in one industry.

Now the question is, are banks doing wrong or making biased decisions? No, because banks do what the lending council instructs.

The Financial Stability Oversight Council clearly warns of how excessive exposure to a single sector can increase systemic risk.

Therefore, banks apply similar internal monitoring. Once a sector becomes a large portion of their loan portfolio, they begin to slow down new approvals

So, what should you do? Hmm, I advise you to focus on multiple financing options. It is not wise to rely on a single bank relationship. How can you expand financing options? You can expand it by focusing on the following:

- regional banks

- credit unions

- industry-focused lenders

Stage 3 = The caution window

In this phase, you will notice the following economic signals:

- Demand growth slows.

- Operating costs rise.

- Market instability increases.

From my perspective, these signals don’t mean industry collapsing. But banks became cautious about approving further credit. As a result, you experienced delayed loan approvals, banks request more documentation & collateral requirements increase. As a lender, you may think that banks do this out of distrust, but they do it for early warning signals.

So, what should you do? You can clearly explain the following things to strengthen your profile:

- revenue resilience

- customer diversification

- long-term contracts &

- cash flow stability

If you do the above, then the bank will notice predictability, which increases the approval chance.

Stage 4 = The credit pause

In this phase, banks temporarily step back from the industry. If banks notice that the risk accumulates, then they pause to finance that sector. This doesn’t mean industry is collapsing; instead, banks do this to observe how conditions evolve.

I have found similar things in the office of the Comptroller of the Currency. They clearly mentioned the importance of adjusting credit risk during periods of uncertainty.

Banks follow similar guidance internally. For this reason, when economic uncertainty rises, banks reduce new loan sanctions until positive signals emerge.

By considering the above facts, I recommend you focus on the timing strategy.

The timing strategy includes the following:

- strengthening cash reserves

- extending existing credit lines &

- exploring non-bank financing options

Why am I saying this? Because eventually, the cycle resets, and when industry conditions stabilize, banks begin lending again.

How can founders recognize a lending window before banks announce it?

Hmm, understood. Are there any signals that help me understand the advanced lending window? Yes, there are. After months of study, I have identified some signals that help you understand the lending window before a bank announcement. Let’s read them:

Watching capital flow before lending expands

According to my study, one of the earliest signals that an industry is entering a favorable credit window is rising investment activity.

Private investors tend to move earlier than banks because they accept higher risk in exchange for higher returns.

Once investors begin funding expansion in a sector, say, new factories, new software platforms, new distribution infrastructure, then banks begin paying attention.

The US Bureau also supports my analysis. The US Bureau of Economic Analysis

found that sector-level capital spending trends before lending patterns visibly change.

Say, capital expenditures begin rising in a specific industry. This refers to companies inside that sector that expect future demand to increase. And, banks take that signal as a potential expansion opportunity.

My advice for you:

You can monitor the following:

- capital expenditure growth in your sector

- venture investment patterns

- industry equipment purchases

Imagine that those indicators start rising together. In this case, it signals that the financing opportunity will improve soon.

Hiring surges signal the next lending cycle

There is a usual rule in the industry. The rule is = When demand grows, companies must hire workers to meet that demand. The US Bureau of Labor Statistics found similar things in their study. They found that hiring acceleration occurs before revenue statistics fully capture industry growth.

Banks monitor these employment changes carefully. Say, your sector begins adding workers consistently. Lenders, i.e., banks, take this as a signal that:

- companies expect sustained demand

- expansion projects will require financing &

- Industry activity could remain strong for several years

My advice for you:

Check industry-wide job growth. If you noticed that employment expands across multiple companies in the same sector, then it indicates that the credit window will soon open wider.

When banks start showing up at industry events

Imagine that banks are interested in financing a sector. In this case, their presence starts appearing in indirect ways. They begin:

- sponsoring industry conferences

- publishing research reports about that sector &

- hosting webinars or panels focused on that market

Banks perform these events to set internal lending strategies. Actually, this is not a biased or personal decision that banks take. Regulatory bodies instruct it.

Regulatory guidance from the Federal Deposit Insurance Corporation also instructs banks to understand industries profoundly before expanding lending risk.

My advice:

Notice whether banks suddenly appear more frequently at conferences in your industry. If so, then it indicates that they are studying the sector because they expect lending opportunities to grow. So, take this as a signal to begin building relationships early.

Supply chains tell the future before headlines do

My analysis found that one of the most reliable early signals of industry expansion appears inside supply chains. How?

When suppliers begin investing in additional capacity (for example, larger factories, new distribution centers, advanced logistics systems), it usually means they expect demand to increase. I just read manufacturing and production statistics studied by the Federal Reserve. I found that they, i.e., the Federal Reserve, also found changes through indicators like industrial production and capacity utilization.

Banks monitor these signals because supply chain expansion suggests industry growth may continue long enough to justify long-term financing commitments.

My advice for you:

I recommend that you closely monitor suppliers and partners.

Say, you noticed that suppliers begin expanding production capacity or opening new facilities. This incident indicates that the industry growth cycle is gaining momentum.

Finance Ideas TL; DR | Tapos Kumar

Credit availability is not evenly distributed among industries. Banks rotate lending appetite between industries based on economic position, portfolio risk, and growth expectations.

This creates credit windows, which are periods when financing becomes easier for businesses in certain sectors and challenging for others.

Frequently Asked Questions (FAQ) about industry credit cycles?

Are industry lending cycles predictable?

In my view, industry lending cycles are not predictable. However, there are some economic indicators that disclose early signals. These economic indicators include sector investment growth, production output & business expansion activity. Banks use them to predict future demand for credit.

My suggestion:

I recommend that you monitor the following industry signals:

- new facility construction

- equipment investment

- hiring acceleration

If you noticed that these indicators appear together, then financing conditions will improve soon.

How long do favorable lending windows last?

Hmm, it varies depending on industry. Some industry lending cycles last several years, while others change quickly depending on economic conditions.

Credit conditions change as industries move through different economic stages. I also found similar things in the national bureau. The National Bureau of Economic Research

found that industries expand and contract at different speeds. For example, infrastructure or manufacturing experience involves long financing cycles. But technology sectors change quickly.

My tips:

I suggest you consider favorable credit conditions as temporary opportunities. If lenders appear supportive today, it will be wise to explore financing before conditions tighten again.

Why does financing sometimes disappear unexpectedly?

This happens because banks stop giving out loans as fast when they see trouble in an industry.

The FDIC (a government agency that watches banks) says banks often change how much money they are willing to lend when the economy looks shaky.

This can happen if:

- People buy less stuff

- New government rules come in

- Companies can’t get the parts they need &

- Prices shoot up quickly

When banks see these warning signs, they will stop giving new loans for a while to think about the risks.

My advice:

Banks usually give hints before they stop lending. You might notice the following signs months before:

- Investors are putting in less money

- Companies hiring fewer workers &

- Businesses in your industry are losing value

So, prepare for this signs & avoid loan difficulty.

Do different banks favors different industries?

Yes. Every bank has its own lending strategy and sector expertise. I found similar insight in regional economic research from the Federal Reserve Bank of Chicago. This study shows that many lenders specialize in industries common within their geographic markets.

For example:

- Agricultural banks focus on farming businesses

- Technology-focused banks serve innovation hubs

- Manufacturing lenders support industrial regions

My suggestion:

Don’t apply in every bank; instead, identify lenders that already finance companies similar to yours. Remember that industry familiarity can significantly increase approval chances.

Can businesses secure financing during sector tightening?

Yes. During sector tightening, lenders typically prioritize companies with strong financial stability.

I have studied the SBA site (a government agency that helps small businesses) & found that banks look at a few important things when times are uncertain. These include answers to the following questions:

- Does the business make money regularly?

- Does the business have enough money coming in to pay bills on time?

- Is the business’s debt small enough that it can credibly be paid back?

- Does the business have many different types of customers, instead of relying on just one or two?

My tips:

If your sector faces tighter credit conditions, strengthen the signals lenders value most. For example, you can do the following:

- improve cash flow documentation

- reduce unnecessary liabilities &

- diversify revenue streams

Do lenders follow investor behavior?

Yes. When private investors put money into businesses, it usually shows they believe things will get better, and banks often start lending more afterward.

Investors are the first to bet that an industry will grow, so their actions give an early clue about the future. If investors fund new companies or help existing ones grow, banks see that as proof the industry has good long‑term potential.

My suggestion:

If big investment firms start putting money back into your type of business, it is a sign that people feel more positive about your industry. Banks often copy that signal and start giving out more loans, too.

Why does credit become selective during industry transitions?

This happens because banks become cautious when industries shift between growth and uncertainty.

During periods of change, banks reassess demand stability, operating costs & long-term profitability. Until trends become clearer, Banks will approve fewer loans or require stronger documentation.

My advice:

When an industry is changing, being ready is very important. Because business owners who show:

- easy‑to‑understand financial records,

- good predictions about future sales,

- and honest, open business practices,

They are more likely to get loans, even when banks are being picky.

Can founders anticipate lending shifts?

Yes, by watching the economy and how investors are spending money.

As a business owner, you should keep an eye on hiring trends, infrastructure investment, investor funding activity, and lender research publications. These will help you detect industry changes months before lending policies change.

My advice:

Think of getting a loan as choosing the right time. Understanding industry signals can help you approach lenders when conditions are most favorable.

Why do many founders misunderstand lending cycles?

Because public discussion focuses heavily on interest rates.

Look, interest rates are only one part of lending decisions. Banks also consider sector stability, economic viewpoint & portfolio concentration. These factors impact lending approvals more than rate changes.

My tips:

Don’t focus on interest rates only; instead, estimate how lenders currently perceive your industry.

Tapos’s Last Thought

How was my article? Did you find it helpful? I have studied for about 1 month; then write it to solve your problems. I am interested in knowing whether my article helps you. If you can manage a few seconds, then please, say it in the comment box.

Why do I request you? In this AI era, machines have just started to replace humans. Hmm, US news headlines say this. CNN, Fox, and CBS are all predicting that Artificial intelligence will replace humans and mass layoffs will happen for this. This is a political debate & I don’t want to talk about it.

So, who understands and solves your problems better: AI or me? Comments below & I wish you a successful startup.

References & Sources

Below is the lists of sources that I have used to write this article:

- U.S. Bureau of Labor Statistics (Industry Employment Data)

- U.S. Small Business Administration (Office of Capital Access)

Disclaimer

The information provided in this article is author’s view & only for educational purposes. This is not a startups advice. This is not a sponsor post & not an investment advice. Do your research before making any important financial decision. Therefore, Finance Ideas will not be liable for your financial loss.