Let me share with a client’s story, he was a 60-year-old engineer from Pennsylvania, sold his rental property for $480,000 in 2024, he faced a classic dilemma: Should he invest in a mutual fund to chase higher returns or go with an annuity for guaranteed retirement income?

The stakes were higher than ever, with inflation running high (hovering around 3.4% in early 2025) and market volatility shaking retiree confidence. My client had spent decades building wealth, and now he needed a strategy to protect it, grow it, and convert it into predictable income. If you are in my client’s shoes, then this article is for you. Why? My article guides you how to make financial decisions for annuity that support today’s American economy.

Let’s start with the following:

Why Today’s Americans Need a Fresh Look at Annuities vs Mutual Funds

Today’s retirees are battling:

- Persistent inflation is shrinking their spending power

- Unpredictable market corrections affecting 401(k) and IRA balances

- Low interest rates in traditional savings vehicles

- The risk of outliving savings as lifespans stretch into the 90s

So, where do annuities and mutual funds fit into this?

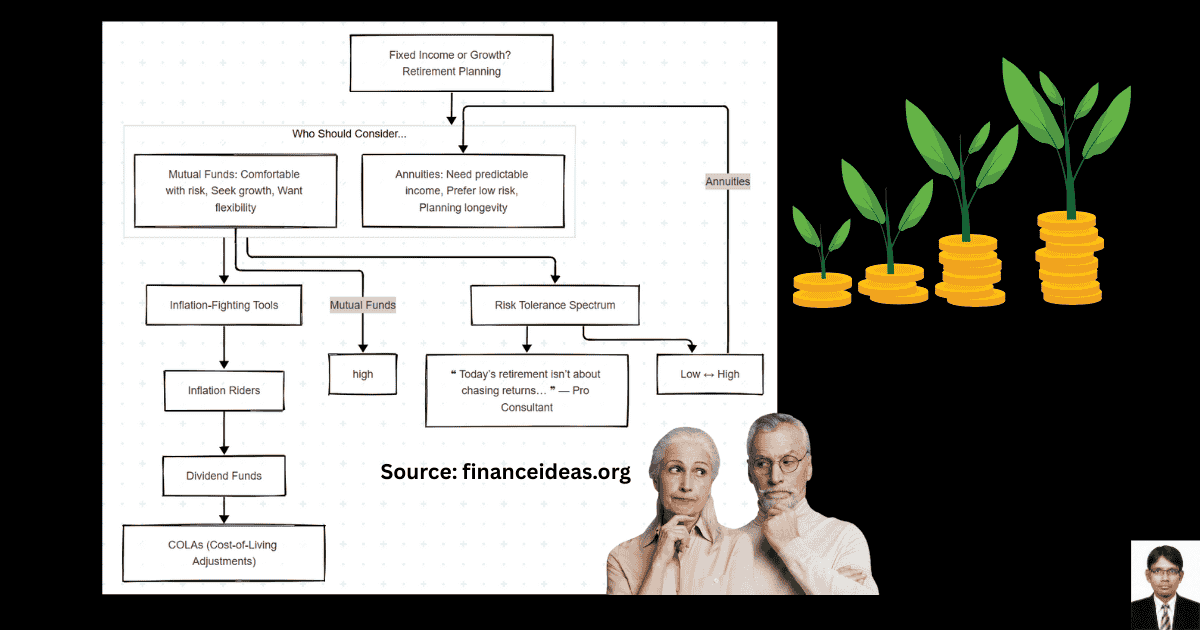

Annuities: They offer inflation-protected income streams (if appropriately structured) and eliminate longevity risk.

Mutual funds: They provide market access and liquidity, but without guarantees.

Below is the table. I have given a side-by-side comparison of Annuity Funds and Mutual Funds for better understanding.

| Feature | Annuity Fund (Fixed or Indexed) | Mutual Fund |

| Primary Goal | Income security & longevity protection | Capital growth and liquidity |

| Inflation Defense | Moderate to high (with riders or COLA) | High (growth potential if market outpaces inflation) |

| Risk Exposure | Low to moderate (depends on type) | Moderate to high (market-driven) |

| Returns | Moderate; often 3–6% with downside protection | Varies; S&P 500 average equivalent to 7–10% long-term |

| Fees | Higher (admin fees, surrender charges, riders) | Lower (0.5–1.5% average expense ratio) |

| Tax Benefits | Tax-deferred until withdrawal | Taxed annually unless in retirement accounts |

| Liquidity | Limited; withdrawal penalties common | High; can liquidate at any time |

| Payout Options | Guaranteed lifetime income, period certain, lump sum | No income guarantees; must sell shares to withdraw |

| Best For | Americans seeking retirement income safety | Those pursuing long-term growth & liquidity |

I hope you have understood the significance of Annuities and mutual Funds in the present inflation era. But the question remains: What should you do if you are in my client’s situation? As a finance professional, I can understand your intention to read my article. And you are in the right article to ask such a question. Let’s continue client’s story.

What did my client choose between a mutual fund & annuity?

My client’s financial advisor showed him two simulations:

- Mutual Fund Route: Invest $480,000 in a balanced portfolio. Assume a 6% return and a 20% downside risk in a bear market. If inflation hits 4%, his purchasing power deteriorates.

- Annuity Route: Put $350,000 into a fixed indexed annuity with a 6% income rider and inflation adjustment. The rest ($130,000) remains in mutual funds for emergency and discretionary use.

In my opinion, my client made the best decision for maximum output. Why? He opted for the hybrid plan. The annuity gave him income predictability and peace of mind in a rising cost environment, while mutual funds offered inflation-beating potential.

My Financial tips for annuity vs mutual fund?

Keep in mind that “Today’s retirement isn’t about chasing returns. It is about preserving freedom in an unpredictable economy.” Therefore, you should

- Use annuities to cover essential inflation-adjusted expenses such as housing, food, utilities, and healthcare.

- To balance your mutual fund exposure with less volatility, you can consider dividend-paying funds, bond-ladder funds, or managed volatility funds.

- Check for inflation riders in annuities because they are crucial Today.

- Consider Qualified Longevity Annuity Contracts (QLACs). According to the IRS resource, they reduce RMDs and provide future income.

- Don’t abandon mutual funds entirely. Why? They still offer growth potential to offset rising costs.

Key Takeaways [Bookmark this now]

- Inflation, longevity, and volatility are reshaping retirement strategies.

- Keep in mind that Annuities = income protection & Mutual funds = growth potential.

- In today’s American economy, the best strategy blends security & flexibility.

- Always compare riders, fees, and inflation adjustments before committing.

- A hybrid approach reduces emotional stress during market drops.

Frequently asked questions (FAQ) about annuity vs mutual fund?

Are annuities a hedge against inflation?

As per my experience, fixed and indexed annuities with inflation riders can help mitigate inflation, but they must be selected carefully.

Can mutual funds beat inflation better than annuities?

I would say potentially yes, but without guarantees. Mutual funds can outperform inflation, but they also come with downside risk.

Are annuities safer for income in uncertain times?

Yes. Annuities offer contractual guarantees regardless of market performance, which is key during economic uncertainty.

What should I prioritize: growth or income?

In the present economy, income stability is more valuable for retirees than growth, which can be pursued with excess capital.

You may also like

- How does an indexed annuity differ from a fixed annuity

- Private placement variable annuity: Why the Top 1% Use This Hidden Annuity to Avoid Taxes?

- Charitable gift annuity vs Charitable remainder trust

Concluding Thought

Now it is verdict time for annuity vs mutual fund. What is best for you now? If you are like most Americans nearing retirement, you are not just choosing between two financial tools. You are choosing between:

- Worry-free sleep or market anxiety

- Guaranteed checks or performance-based results

- Income security or liquidity flexibility

You don’t have to pick one. Instead,

Use annuities for peace of mind and mutual funds for growth and options. This is not a product war; instead, it is a personal retirement mission.

“When inflation eats into your future, income guarantees become more than smart & they become necessary.”

Hello, respective reader! Please, share it with someone struggling with the same choice if you found my article helpful.

Have questions about annuities or your retirement options? Drop your comment below.

Share or Cite This Article?

We love backlinks, and we reward credit. You may quote, summarize, or reference this article in your blog, newsletter, or research as long as you include a do-follow link back to the particular article & localhost/bloghub/.

Remember, reproducing this content without attribution is prohibited.

For Media, academic, or press use? Contact at kumartaposbanarjee@gmail.com

[Read our full content use policy on the home page]

References & Sources

Below is the lists of sources that I have used to write this article:

- AM Best – Insurance Company Credit Ratings

- Morningstar – Historical Performance of Mutual Funds and Market Indexes

Disclaimer

This is not a Sponsored post & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, localhost/bloghub/ will not be liable for this.