In-house financing is growing in acceptance in America. According to Federal Reserve data, about 46% of American consumers have used some form of in-house financing.

According to my study, 35% of engagement ring buyers use in-house financing options to afford their purchase.

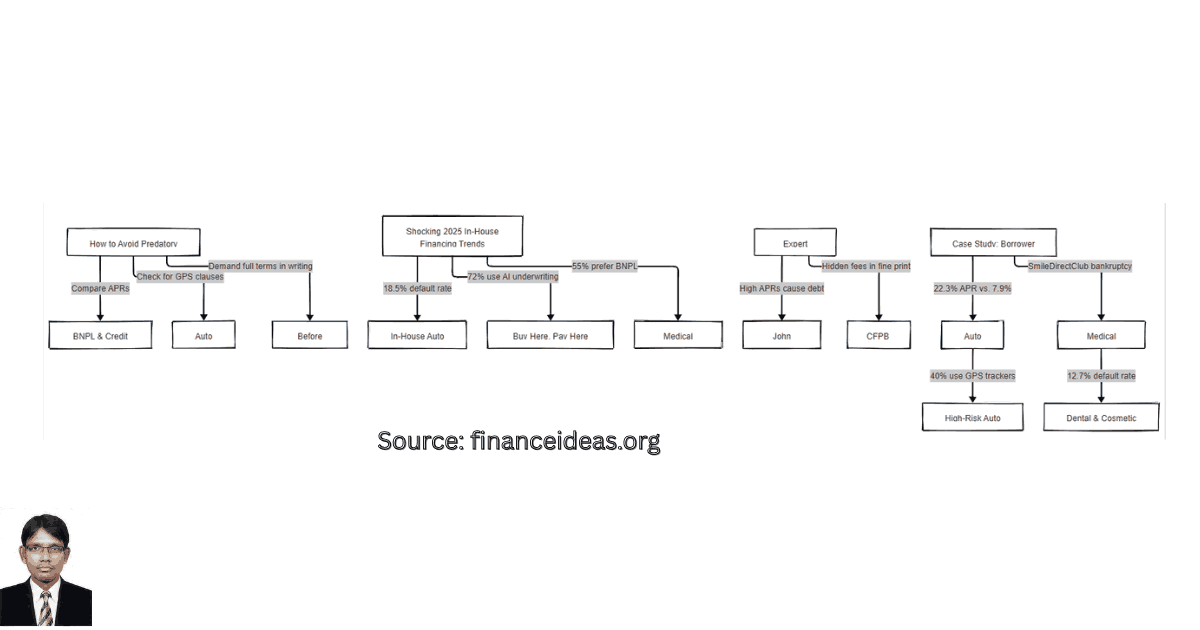

However, the use of captive financing is not limited to jewelry or auto financing instead it spreads to medical service also. A study conducted by J.D. Power found that 42% of patients used in-house financing for elective dental procedures with average APRs ranging from 12 to 18%.

What does in house financing mean? Is it suitable for you? You could have such type of questions & it is normal. Financing is not an easy task after all but proper guidance could save you from extra credit burden.

If you are a such type of person & looking for professional guidelines on it then you are in the correct article. This article will give you a complete guidance that help you to decide when you should consider captive financing & when should not.

Let’s start with the following:

Key Takeaways

- Captive financing could be helpful for you if you have a bad credit score & urgent need.

- In-house financing charges a higher interest rate than bank loans.

- Captive loans are commonly used in the automotive, furniture, jewelry, and healthcare industries.

- Always compare alternatives such as personal loans and credit cards before picking captive finance.

What does In-House Financing mean?

In-house financing which is also known as captive financing is a form of direct lending to customer from retailer or vendor. You don’t need to rely on traditional finance like banks or credit unions. Captive financing eliminates third party lenders & the retailer or vendors acts as the lender who set its own loan terms, interest rates, and repayment schedules.

In-house financing works like a promotional tool & most industries use it to boost sales. The table below provides details about those industries that use Captive financing:

| Industries | Use case/ Example |

| Automotive Dealerships | Offer in-house loans for vehicle purchases |

| Furniture and appliance retailers | Allow to purchase expensive home essentials. For example, Ashley Furniture, Rent-A-Center. |

| Jewellery stores | Offer instalments plans for high-value pieces. For example, Kay Jewelers offer payment plans for expensive pieces. |

| Healthcare providers | In house financing for dental work, cosmetic treatments, and elective surgeries. |

Perhaps you understand it or maybe familiar with captive loan. Picking financing is not like ice-cream choosing. Therefore, you should have clear understanding on whether in house financing fit with you. If my guessing is correct then the following question will guide you on it.

Should you consider in-house financing?

In house financing has many aadvantages such as faster approvals, easier eligibility, convenience location & flexible loan amounts.

I have conducted a study on automobile industry to find out captive financing acceptance in US vehicles market. The study highlighted that,

“In-house financing accounted for 25% of all vehicle sales in America. Usually, customers with subprime credit scores prefer dealership financing for easy approval.”

However, some customer object for higher interest rate (between 7% and 25%) compare to traditional loans.

According to my analysis, captive financing is a great loan option but higher interest rate could be extra financial burden. Therefore, I advise you to compare in house loan with traditional financing & read detail loan terms.

I don’t think that my analysis is partial; instead, it is supported by prominent experts & studies.

A similar study conducted by Experian & found that 68% of in-house financing applicants have credit scores below 620 which create difficulty to approve traditional loan.

Prominent financial experts recommended to compare loan terms before accept captive financing & because it charge higher than bank rates.

Another prominent financial advisor, Mark Johnson, also emphasizes loan conditions. He stated,

“In-house financing is a great tool for immediate purchases, but buyers must read the fine print. Always compare APR rates and repayment terms before signing an agreement.”

So, whether you should consider captive finance, it depends on your purchase & financing requirements. If you are looking for immediate financing & don’t care interest rate then in house financing is a great option.

Now, it is high time to compare captive financing with traditional loans.

In-House Financing vs. Traditional Loans?

I think, sometimes paying higher interest to meet immediate requirement is logical. But I don’t recommend to fully depend on captive financing. Instead, consider in house financing depends on financial situation & purchase requirements. Therefore, I would suggest a rational combination between captive financing & traditional loans.

John Ulzheimer, a former Credit Expert of FICO & Equifax said that

“Captive financing can build credit score if your payments are reported to bureaus. However, high interest rates can trap borrowers in debt cycles.”

Then, the Consumer Financial Protection Bureau (CFPB) said,

“Consumers should compare in-house financing with alternatives (credit cards, personal loans) to avoid overpaying.”

They all indirectly advise a mixture of both financing. Below in the table, I have given a side-by-side comparison between captive financing & traditional loans so that you can make a quick decision between in-house financing & conventional loans.

| Feature | In-House Financing | Traditional Bank Loan |

| Approval Speed | Fast (same day) | Slower (days/weeks) |

| Credit Requirements | Lenient | Strict (good credit needed) |

| Interest Rates | Higher (10-30%) | Lower (4-15%) |

| Down Payment | Often required | Sometimes waived |

Concluding Thought

Captive financing is a better loan option for you if you struggle with a bad credit history. Keep in mind that in-house financing is easy to get but always comes with a higher interest rate. According to Experian Credit Report, in-house financing loan defaults rose by 12% in the past two years for higher interest rates.

Therefore, my advice is to read & understand interest rates, fees, and repayment terms of captive financing.

I hope my article help you to analysis in house financing that save you from interest burden & also guide you when you should take it.

Do you have prior captive financing experience? Please share it in the comments sections so that others also learn from it. And, if you found my article helpful, please share it with you colleagues to spread the awareness.

Frequently Asked Questions (FAQ) about in house financing?

Does in-house financing affect my credit score?

Yes, in house financing affect your credit score. If the retailer reports to credit bureaus, your on-time payments can improve your score. Keep in mind that, late payments can negatively impact it.

Can I negotiate my in-house financing loan terms?

Yes, you can negotiate a lower interest rate or for longer repayment terms. Keep in mind that negotiation for in-house financing loan terms depends on retailer. Some retailers may not allow to negotiate or some may allow.

Are there prepayment penalties with in-house financing?

Some lenders charge for early repayment. I advise you to always read the loan agreement before signing.

What happens if I default on my in-house financing loan?

If you default in-house financing loan then the retailer repossesses the item. He may report missed payments to credit bureaus, even can take legal action.

Is in-house financing safer now than before?

No, in-house financing carries default risks as like before for economic uncertainty. Therefore, my advice would be always comparing with BNPL or credit unions.

Can I refinance an in-house loan?

Yes, some lenders allow refinancing but interest rate will be high. You will find more about refinance in local credit unions.

Do in-house lenders report to credit bureaus?

Yes, most lenders report to credit bureaus, but reporting standards vary. Therefore, it would be better to ask before signing.

References & Sources

Below is the lists of sources that I have used to write this article:

- National Auto Dealers Association (NADA) – Auto financing trends and statistics

- Experian 2024 Credit Report – Data on in-house financing and credit scores

- Federal Reserve Consumer Credit Data – Trends in consumer financing and loan defaults

- Jewelry Industry Financing Trends – Insights on financing engagement rings and luxury items

- CFPB’s Guide to Auto Financing (2025)

Disclaimer

This is not a Sponsored post & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, localhost/bloghub/ will not be liable for this.