Say, you are talking to a bank for startup financing. Everything works perfectly, i.e., calls were happening, and e-mails were answered. Then, slowly, things changed. Replies took longer. More questions came in. Ultimately pause. You don’t get any official e-mail.

Months later, another company with the same profile, i.e., same revenue, market share like yours, got loan approval from the bank.

As a founder, you perhaps experienced such incidents. Do you know why this happened? I am asking you because, according to my study, about 70% US founders don’t know the exact reasons. Yeah, you could be remaining 30%, or you can just ask AI for an answer.

If you know, I would be happy if you share it in the comments. So, pause reading & comments below. Are you done? I hope so; now want to disclose the reason. It happens for the internal risk ladder. It means the bank internally ranks borrowers & this ranking decides whether you get a loan.

Yeah, you have many questions & I am writing this article to answer them professionally. So, take some filtered drip coffee & start reading.

Finance Ideas AI snippet box | Tapos Kumar

What is the internal risk ladder?

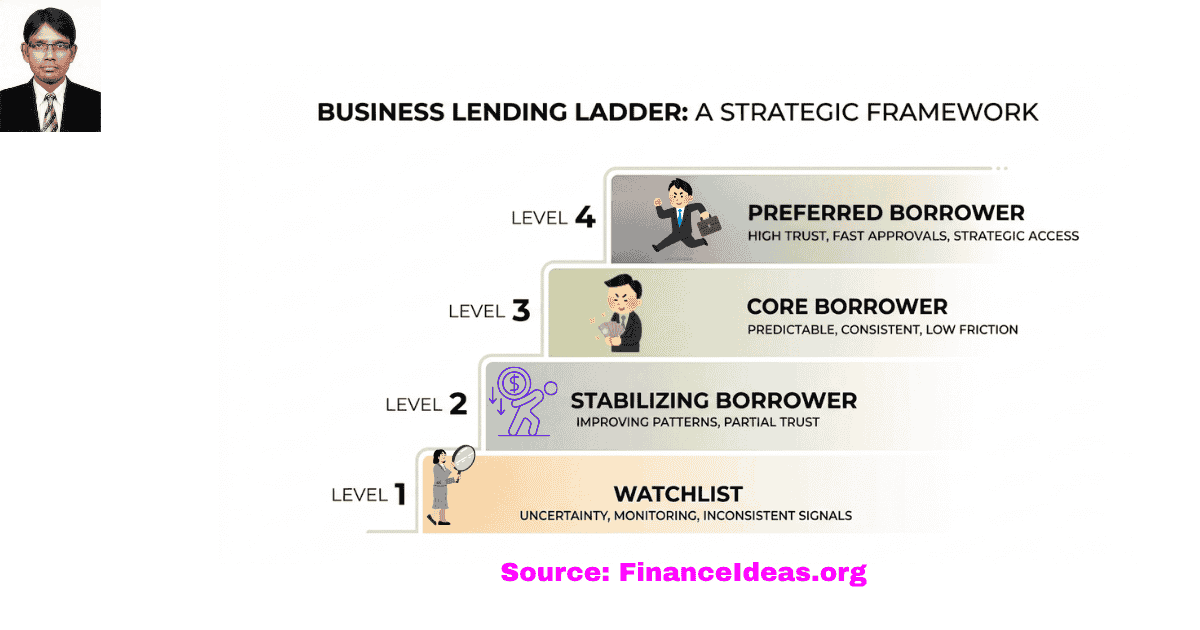

The internal risk ladder is a bank’s internal classification system that ranks borrowers based on observed behavior, financial patterns, and risk predictability.

It typically includes:

- Watchlist (heightened monitoring)

- Stabilizing borrower (recovering or improving)

- Core borrower (reliable and consistent)

- Preferred borrower (low-friction, high-trust)

Movement on this ladder can affect approval speed, documentation requirements & easy credit.

Lesson:

Banks don’t treat all approved borrowers equally; your internal tier determines how you are treated after approval.

Related Articles

- Loan for start up: Fund Your Dream

-

How US lenders define risk: If Lenders Say You’re “High Risk,” Read This First

-

Why Startup Loan Rejections Feel Vague: And Why Lenders Stay Silent?

-

What lenders see in bank statements: But Never Explain

-

90-day plan after startup loan denial: Here’s the Smarter 90-Day Move

-

Risk memo after loan denial: What lenders document about you?

-

Cash conversion cycle lenders model: Denied Again? Read this

-

Bank portfolio math: Why Perfect Borrowers Hear No

-

Capital preservation bias: What Founders Get Wrong?

-

Founder distribution problem: The Hidden Risk Behind Owner Pay

- Loan approval momentum effect: What Most Founders Miss?

- Bank relationship capital: How Founders Build Banker Trust

-

Interest rates vs risk appetite: The Credit Market Secret Most Founders Miss

-

Industry credit cycles: The Lending Window Most Founders Miss

-

Financial statement stability optics: How Banks Read Your Financials?

Is startup loan approval the starting point?

Yeah, you feel like a winner after getting a loan approved by a bank, but it is not the end of the story. Approval is only a snapshot of that moment. Afterward, the bank keeps watching your business, re‑evaluating you as things change, just like a teacher checking in on a student throughout the school year.

So, what do Banks recheck? Banks recheck your behavior & categorize them into

Watchlist → under closer monitoring

Stabilizing → showing signs of recovery

Core → steady and reliable

Preferred → trusted, low‑friction clients

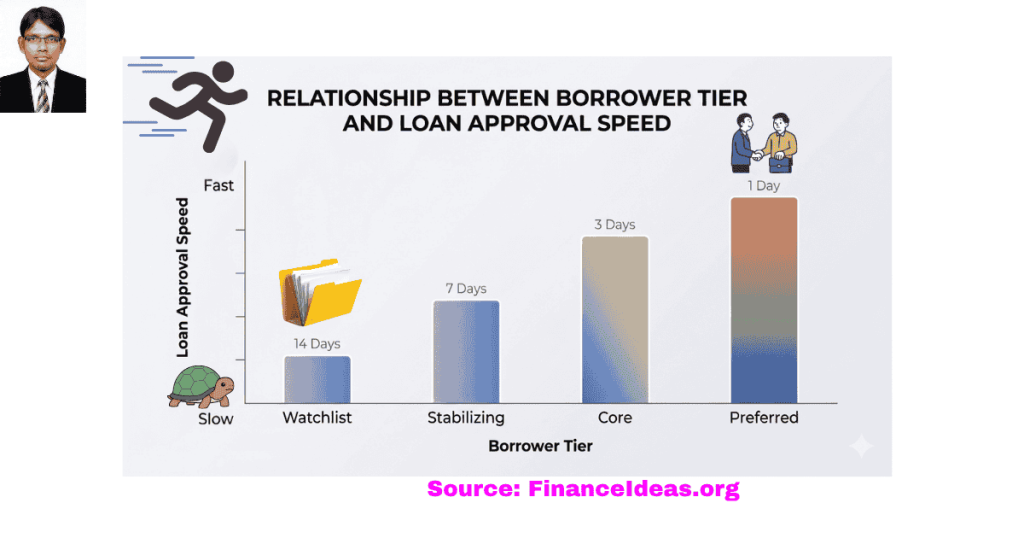

Your business behavior will decide where you sit on this ladder. Then, based on that ladder, banks will decide how fast your requests move, how much paperwork you face, and how easy the terms will be.

Hmm, now you could ask me; are there any signals that help me to understand it? Yes, let me tell you how.

You, as a founder, will notice that approvals take longer, bankers ask for extra details, and communication seems more formal.

Say, last year, your credit extension was approved in two days. This year, it has dragged on for weeks with more questions. That is a sign you have slipped down a tier.

Now you may ask why banks do it? Banks do it for credit security & it is instructed by US lending regulatory bodies. Banks noticed your behavior that includes irregular reports, shrinking margins without explanation, sudden jumps in credit usage, or silence during operational changes. Individually, they don’t impact on credit but cumulatively negatively impact on loan approval.

My advice:

Don’t try to prove that you are a stronger applicant. You should focus on clear business behavior disclosure. For example:

- Margins dipped because we are renegotiating supplier contracts.

- Credit usage increased as we prepared for expansion.

Remember that banks prefer a clear indication because it restores confidence. And in banking, confidence is more important than financial numbers.

What will happen after gaining the lender’s confidence?

After following my advice, you get fewer follow‑up questions, quicker responses, and easy renewals. It feels like the bank is finally on your side, and the relationship becomes easier.

Banks will do these because banks now understand you. Risk teams see stable financial behavior, consistent management decisions, and communication that matches your actual results.

The internal risk team of banks will debate less on your financial solvency & justification. In simple words, banks require less effort to understand it, which indirectly increases the loan approval chance.

Banks are instructed by lending regulatory bodies to look for clear documentation, consistent borrower behavior, and transparent communication. Therefore, if you operate your business according to these instructions, then you have a positive chance of getting an easy loan.

Besides, you can negotiate terms more confidently, introduce new credit requests strategically, and even discuss timelines or structures. Internally, you will be a solvent applicant in front of the bank.

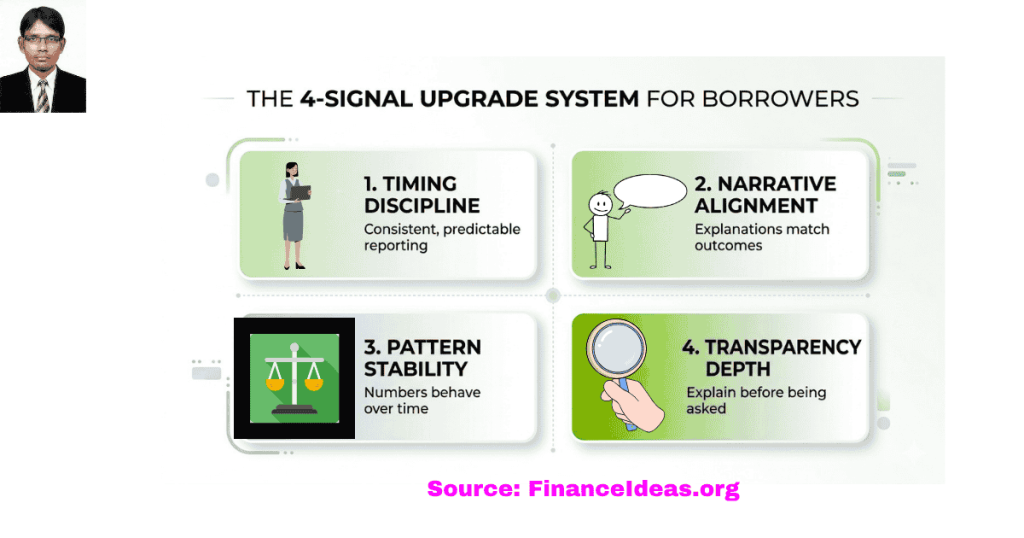

What are the 4 signals that help founders to be high‑trust?

I have conducted a survey about how US founders can lower internal risk for funding. My survey found that many founders try to fix everything when dealing with lenders. According to me, this is the wrong approach. This is because banks don’t evaluate everything equally. They care most about signals that reduce their internal friction, i.e., the things that make it easier to understand and approve.

By considering these facts, I have identified 4 signals that make you a trusted borrower in front of banks. Don’t worry, these are field-tested & I am discussing these signals with solutions. Let’s start:

- Timing discipline = Are you predictable on the calendar?

Remember that even strong numbers lose credibility if reports arrive inconsistently. Lenders consider this =If timing varies, what else varies?

Say, you always send monthly reports on the 5th, stick to that schedule. Don’t let it drift to the 7th one month and the 10th the next.

My tips: Send updates on fixed dates, and if possible, deliver earlier than expected. This is because predictable timing shows operational discipline.

- Story alignment = Do your words match your results?

I found that founders often overpromise, then adjust explanations later. Banks consider this a mismatch between expectations and reality.

Imagine that you forecast 10% growth but deliver 8%. In this condition, you need to explain clearly why and show how the forecast connects to reality.

My tips: Understate projections slightly, and make sure your explanations match actual outcomes. Remember that alignment builds credibility faster than growth.

- Pattern stability = Do your numbers behave like a system?

Random swings in performance create uncertainty. If this happens to your business then banks consider this= Is this controllable or just luck?

For example, if sales dip, explain it was due to seasonal demand. This will help lenders to understand that it does not happen by random drop.

My tips: Show cause‑and‑effect behind changes, and break down performance into segments so patterns are visible. Remember that stability is about being explainable.

- Transparency depth = Do you explain before being asked?

Waiting for questions makes lenders feel like something was hidden. Banks consider this = If we have to ask, what else don’t we know?

Therefore, if you increase credit usage, tell the bank upfront = We are preparing for expansion, so that utilization will rise temporarily.

My tips: Share context before reviews, and explain decisions with results. Remember that transparency reduces friction faster than performance improvements.

Finance Ideas TL; DR | Tapos Kumar

- Getting approved by a bank is just a moment in time. But after that, the bank keeps watching and re-evaluating you. Your status can change as your business changes.

- Your position inside the bank changes gradually over time.

- Small behavioral signals trigger tier movement.

- Where you sit on the bank’s internal ladder (preferred, core, stabilizing, or watchlist) decides how quickly they process things for you, how much paperwork they demand, and how flexible they will be with terms.

- Business owners don’t realize their ranking has changed until they suddenly face slower approvals, stricter requirements, or less favorable loan conditions.

Free Download resources

Frequently Asked Questions (FAQ) about the internal risk ladder?

Will a bank tell me my internal risk tier?

No. Internal classifications are part of ongoing risk monitoring systems. They exist to help lenders comply with supervisory expectations. Disclosing them would reduce flexibility in how banks manage evolving risk.

Do these:

Banks will never tell you about internal risk. But you can estimate them by checking the following questions:

- Is response time slowing?

- Are questions increasing?

- Are approvals requiring more justification?

Can I be profitable and treated as risky?

Yes. I always say this = Profit is a snapshot & risk is a pattern. Therefore, a profitable business with unpredictable swings can trigger more concern than a modest but stable one. This is because repayment depends on consistency.

Do these:

I suggest you focus on consistent behavior. How can you do that? You can do these by even revenue where possible, explain variability early & align Profit with cash flow timing.

How fast can I move up internally for credit?

Quickly. Banks don’t need years to re-evaluate you. They need consistent behavior across a few cycles.

Therefore, a change in reporting discipline, communication timing & explanation can change perception within one or two review periods.

Do these:

Pick this behavior to standardize immediately = same reporting date in every cycle. Remember that consistency compounds faster than growth.

What causes the fastest drop in trust in the internal risk ladder?

According to my analysis, it is an unexplained change. You have presented a profile, but the bank later found a change. Such incidents create a perception gap & kill trust quickly.

My tips:

Do this = If it changes internally, explain it externally, before it appears in numbers.

Are my communications tracked in the internal risk ladder?

Yes. Interaction history becomes part of the relationship management records. They check

- How often do you communicate

- how early you flag issues &

- How consistent are your updates

These patterns help banks, i.e., lenders, interpret your financial data more accurately.

Do these:

Treat communication like financial data that includes structured, consistent & intentional. Every update should shape your profile.

Can one mistake change my position in the internal risk ladder?

Yes, if it is unexplained. Yeah, a single event doesn’t impact. Still, a single unexplained event can change perception, especially in environments where forward-looking risk monitoring is expected.

Do these:

Respond in layers, i.e., acknowledge immediately, explain the cause & show the timeline for normalization.

Why do some loan approvals get almost effortless?

This is because internal uncertainty is already low. The decision is partially formed when you apply for a loan. So, make your patterns, i.e., business behavior, clear and consistent, which means fewer internal debates, fewer validation steps & faster approvals.

My tips:

I suggest you lower the uncertainty before applying for a loan.

Can a strong history offset a weak period in the internal risk ladder?

Yes. Consistent past behavior creates a reference point. Say a dip occurs. In this situation, lenders want to know = Is this temporary or structural? Strong history, i.e., reliable behavior, helps them interpret it as temporary.

Do these:

I advise you to build your credibility reserve early. You can do these by consistent reporting, aligned projections & stable patterns.

Does this system for loans matter even when the economy is strong?

Yes. Risk monitoring doesn’t pause during growth. In fact, strong economies are when patterns are established, trust is built & positioning is strengthened. Banks do this because downturns disclose what was built earlier.

My tips:

I suggest you use stable periods to standardize reporting, build a communication rhythm & strengthen internal perception.

Tapos’s Last Thought

Did you find my article helpful? Share your personal experience in the comments box. I love to learn from others’ views. Also, it would be helpful for me if you say who is better to understand you = AI or Me.

Before closing, I want to share the last tips. Banks don’t make decisions for one incident. They build an interpretation of your business over time. That means your position inside the system matters just as much as your performance.

So, follow my recommended steps.

Step 1 = Diagnose your current position

Ask yourself: Are responses slower? Are the questions more detailed? Are approvals slow? If yes, then you don’t have a credit problem; you have a positioning problem.

Step 2 = Decide what you need

Your strategy depends on your position:

If friction is rising → focus on detail.

If you are stable but stuck → reinforce patterns.

If things feel easy → expand leverage.

Step 3 = Know the four realities of credit tightening

Borrowers don’t all experience the same market change. So, check these:

Watchlist → delays and reduced flexibility.

Stabilizing → deeper reviews and conditional approvals.

Core → steady movement with caution.

Preferred → access when others struggle.

References & Sources

Below is the lists of sources that I have used to write this article:

- Federal Reserve: Senior Loan Officer Opinion Survey (SLOOS)

- Office of the Comptroller of the Currency (OCC) : Safety and Soundness

- U.S. Small Business Administration (SBA): Access to Capital

Disclaimer

The information provided in this article is author’s view & only for educational purposes. This is not a startups advice. This is not a sponsor post & not an investment advice. Do your research before making any important financial decision. Therefore, Finance Ideas will not be liable for your financial loss.