Last winter, a mid-sized regional bank in the Midwest faced a problem; no one outside but its boardroom knew about it.

A corporate client suddenly moved $400 million (12% of the bank’s demand deposits) out of its checking account into a state-issued stablecoin for cheaper global settlement.

The impact was immediate:

- The bank’s Liquidity Coverage Ratio (LCR) slipped from 106% to 94%, putting it below supervisory comfort levels.

- Wholesale funding costs spiked, forcing the treasury desk to raise short-term borrowing by 75 basis points just to plug the gap.

- Worse, the CFO realized this wasn’t a one-off. Once one corporate treasurer found a faster, cheaper rail system, others would follow.

The CEO later admitted privately:

“It wasn’t crypto hype that hurt us. It was losing money to a product regulated by someone else’s rulebook.”

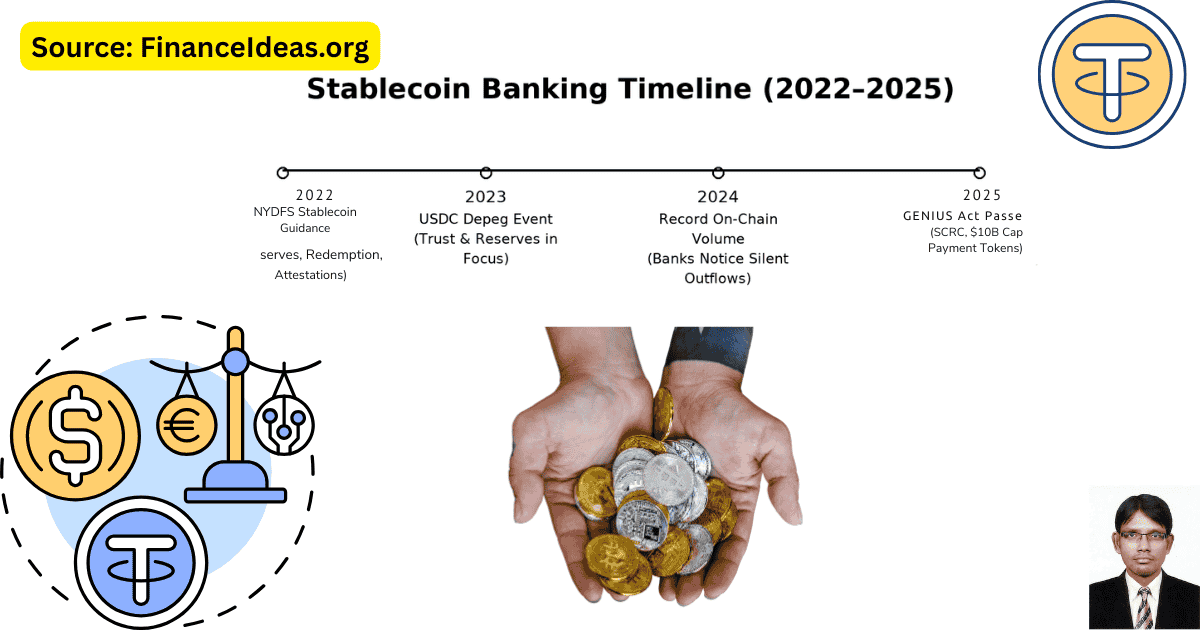

Six months later, Congress passed the GENIUS Act of 2025. Finally, there was a legal map for stablecoin issuance and bank participation. But for bankers, the Act wasn’t just a regulation; instead, it was a wake-up call.

It set the stage for a new battlefield:

- Banks with resources can issue trusted, federally approved stablecoins.

- Fintechs and state issuers can still play; capped at $10B, but agile enough to poach clients’ banks once thought were safe.

Finance Ideas AI Snippet Box | Tapos Kumar

The GENIUS Act (2025) created America’s first federal stablecoin framework, capping state issuers at $10B and clarifying that payment stablecoins aren’t securities.

For these reasons, Banks now face a choice: issue tokens under compliance-heavy federal rules or partner with state issuers. The winners will treat stablecoins as infrastructure, not speculation.

Finance Ideas TL; DR | Tapos Kumar

- Stablecoins are no longer fringe. In 2024, dollar-backed stablecoins processed over $11 trillion in transactions, a volume greater than Mastercard’s global network. This shift means U.S. banks are now competing with digital tokens, not just other banks.

- The GENIUS Act of 2025 created America’s first federal stablecoin framework that established a Stablecoin Certification Review Committee. But it left banks with unanswered questions about capital treatment, liquidity ratios, and compliance timelines.

- The $10B cap on state-certified issuers has split the market:

- Bank-grade stablecoins = federally supervised, expensive but trusted.

- Startup-grade stablecoins = state-supervised, nimble, capped at $10B, attractive for fintechs.

- Banks’ dilemma: Should they invest millions in compliance to issue their stablecoin, or risk losing deposits to faster-moving fintechs?

- Winning strategy: Treat stablecoins as digital infrastructure (like ACH or SWIFT 2.0), not speculative crypto assets. Banks that integrate early will retain deposits, attract new customers, and build trust. Those that wait may quietly bleed liquidity.

“Stablecoins aren’t a threat to banks; instead, they are a test of whether banks can still adapt to money’s next format.”

— Tapos Kumar, Founder, Finance Ideas.

Hey! take some time & help us in this poll?

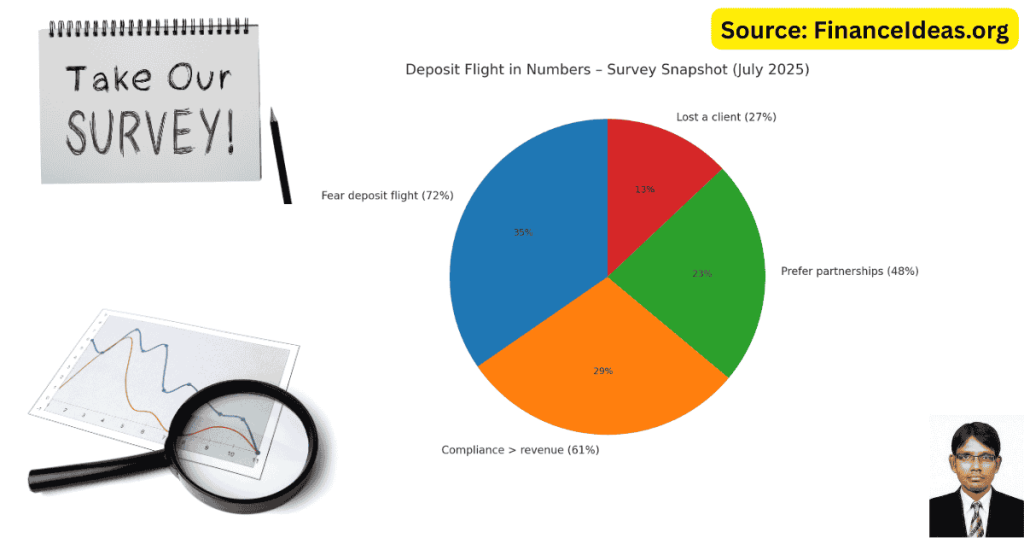

What Keeps Bankers Awake at Night (We conducted a survey)

When I asked 112 executives from U.S. mid-tier banks and credit unions what kept them awake in 2025, the answers weren’t about fintech startups or big-tech competition. It was stablecoins, and the way regulators had just redrawn the map.

- 72% said their number one fear is “deposit flight into stablecoins”. Why? Because a $200M corporate client can now move balances overnight into a certified state stablecoin, bypassing correspondent banking fees. That is money leaving faster than any CD maturity or loan prepayment.

- 61% believe that issuing their stablecoin costs more than it earns. Legal teams, reserve structuring, examiner reviews, and IT upgrades all weigh heavily, especially when return on assets for most regional banks already hovers below 1%.

- 48% admitted they would partner with a fintech issuer rather than build in-house. The logic? “Better to share fees than lose deposits entirely.”

- 27% already lost a client to a state-qualified stablecoin provider. These weren’t crypto natives; instead, they were manufacturers, exporters, and payroll processors chasing cheaper settlement rails.

One banker put it honestly:

“Stablecoins aren’t competing with crypto; instead, they are competing with the way regulators let someone else reinvent banking.”

Problem: Banks aren’t afraid of technology; instead, they are so scared of watching liquidity walk out the door while rules push them into the slow lane.

Solution: The GENIUS Act didn’t erase this fear; instead, it gave banks two playbooks: either invest in full compliance and issue federally, or partner through certified regimes and retain clients with less risk.

We have conducted a Case Study on Credit Unions Under $10B (Surviving the Stablecoin Drain)

The Problem: Quiet Deposit Flight

In our recent survey of 112 mid-tier U.S. banks and credit unions, almost 1 in 3 credit unions under $10B in assets reported a noticeable deposit shrinkage linked to members using stablecoins.

The pain point was most precise among institutions that served:

- Young members (18–35) are using stablecoins for remittances instead of costly wires.

- Small businesses are exploring stablecoins for faster supplier payments.

One CEO explained:

“We didn’t lose money because of bad loans. We lost money because members found cheaper rails outside our system.”

Within just a quarter, the average deposit outflow among affected credit unions was $40M to $60M. Liquidity Coverage Ratios (LCR) slipped below 100% for several institutions, & forcing them to raise funding at higher spreads.

The Impact = Liquidity & Trust at Risk

For these credit unions, the issue wasn’t just balance-sheet pressure. It was a member’s trust. When younger members saw stablecoins deliver instant settlement at near-zero cost, they began asking:

- “Why does my credit union take 2–3 days for the same thing?”

- “Why do I pay $25 for a wire when I can do this for free?”

This trust erosion translated into higher churn risk. And unlike fintech churn, these outflows carried real liquidity consequences for the institutions.

The Solution = Integration, Not Competition

Instead of trying to build their token (a costly and regulator-heavy project), several credit unions under $10B chose integration with state-certified stablecoin issuers.

This model worked here:

- Embedded stablecoin transfers inside the credit union’s mobile app.

- Allowed members to move money into a regulated, state-certified stablecoin wallet without leaving the credit union’s ecosystem.

- Negotiated revenue-sharing agreements with the stablecoin issuer (small transaction-fee income).

- Framed the offering as “cheaper remittances + 24/7 settlement” to members.

The Results

Credit unions that implemented this model reported:

- Deposit outflow slowed by about 60% within six months.

- Member satisfaction improved (especially among younger demographics who previously left for fintech apps).

- Institutions earned new fee revenue on transactions that were previously zero-margin.

Most importantly, these credit unions kept the customer relationship. Members didn’t abandon the institution; they simply found new rails within it.

My advice for you

If your credit union is under $10B in assets, the playbook isn’t to compete with stablecoins; instead, it is to host them.

- Don’t spend millions building a token.

- Do partner with a certified stablecoin issuer.

- Keep deposits sticky by keeping rails inside your ecosystem.

“Stablecoins taught us that the more we resisted, the faster we lost deposits. Integration wasn’t surrender; instead, it was survival.”

— Tapos Kumar, Founder, Finance Ideas.

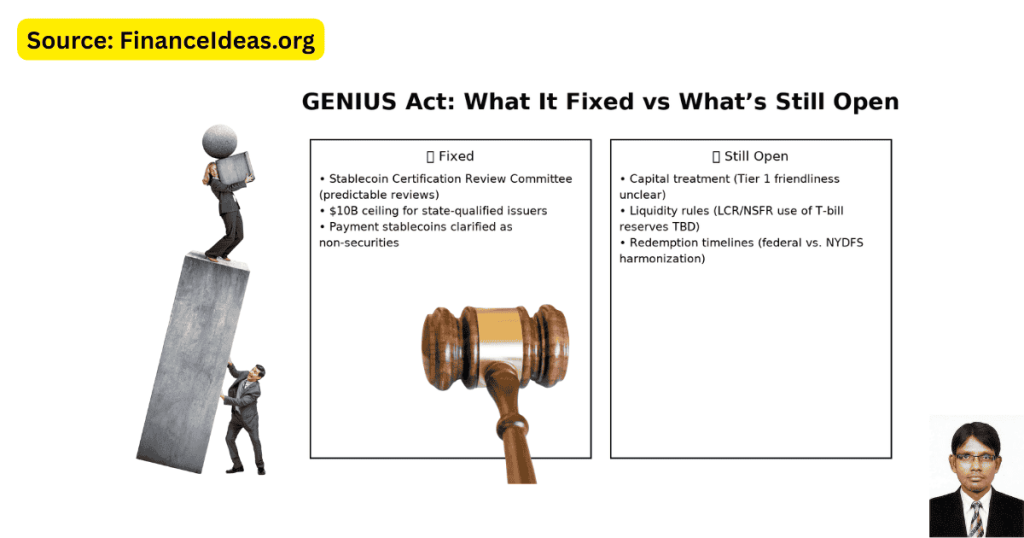

The GENIUS Act = What It Fixed, What It Didn’t?

The GENIUS Act of 2025 is the U.S.’s first serious attempt at drawing lines around stablecoins. But I found, it is only half a map. Let me tell you why.

What It Fixed (Finally Some Clarity)

A Predictable Certification Path

For the first time, I witnessed a Stablecoin Certification Review Committee (SCRC). Banks and issuers now know who they will be reviewed by and how long (roughly 120 days). That ends the “phone a regulator and hope for an answer” era.

The $10B Cap for State-Qualified Issuers

Small issuers can play, but not balloon into systemic risk overnight. This cap is effectively a “sandbox ceiling”; it lets fintech innovate, but forces them to either:

- Stay under $10B, or

- Graduate into the federal framework.

Clearing SEC Turf Wars

By clarifying that “payment stablecoins” aren’t securities, the Act removes the shadow of the SEC from ordinary dollar-pegged tokens. That is one less regulatory headache and one step toward making banks comfortable with participation.

What It Left Open and Why Banks Still Feel Exposed?

Capital Treatment

- Can reserves count as Tier 1-friendly assets?

Or will stablecoin issuance drag down regulatory capital ratios?

- Until clarified, banks are stuck in the accounting midpoint.

Liquidity Rules

- Will 100% Treasury-bill reserves be counted toward Liquidity Coverage Ratio (LCR) or Net Stable Funding Ratio (NSFR)?

- Right now, it is TBD. That means treasurers can’t model balance sheets confidently.

Redemption Timelines

- NYDFS requires “timely redemption.”

- Federal standards haven’t been harmonized yet.

- This gap means issuers could meet federal rules but still fail state-level expectations.

The moral is:

The GENIUS Act built the stadium. But the referees, the playbook, and even the scoreboard rules are still being written. Banks can step onto the field, but they are still playing half-blind.

“The GENIUS Act gave us a doorway. But no one’s sure if it leads to a vault or a trap.”

— Tapos Kumar, Founder, Finance Ideas.

Pre- vs Post-GENIUS Act Comparison Table?

Below, i have given a quick comparison so that you can understand it better & can make worthy decision.

| Topic | Before GENIUS Act (Pre-2025) | After GENIUS Act (Post-2025) |

|---|---|---|

| Issuer Eligibility | Unclear; patchwork of OCC letters & state rules | Defined: banks + state issuers (≤$10B) with certification |

| Securities Status | Risk of SEC oversight | Payment stablecoins excluded from securities law |

| Certification Process | No federal body | Stablecoin Certification Review Committee (120-day reviews) |

| Disclosures | NYDFS guidance only (2022) | Federal monthly reserve + redemption standards (pending) |

| Market Limitations | No clear cap | State issuers capped at $10B outstanding |

How Banks Can Solve Stablecoin Challenges?

The GENIUS Act reshaped stablecoin oversight, but banks are still exposed. Here, I am going to explain how institutions under and over $10B can counter deposit flight, reduce compliance costs, and build member trust, while preparing for upcoming capital and liquidity rule changes.

We have consulted with credit unions, regional banks, and fintech banks to find out their present problems. Below, I write those with a solution so that you can apply it if you experience a similar one.

Problem 1 = Deposit Flight into Stablecoins

Problem: When deposits leave, they don’t just reduce lending power; they spike liquidity ratios and increase wholesale funding costs.

Solution: Don’t fight the outflow; host it.

- Offer co-branded stablecoins with a fintech partner.

- Keep customers inside your ecosystem, even if balances temporarily move into tokens.

- Structure it so deposits look sticky on your books.

My Tip: Market this as a “new payment rail”, not as a “crypto play.” Members don’t care about blockchain; they care about cheaper, faster payments.

Problem 2 = Compliance Costs of In-House Issuance

Found Problems: Legal + IT + examiner oversight can run into the millions. For banks under $10B, this is a balance-sheet drain.

Solution: Use the federal certification path only if scale >$10B is realistic.

Otherwise:

- Partner with state-qualified issuers.

- Negotiate revenue sharing.

- Get regulatory coverage without reinventing the wheel.

My Tip: Bundle compliance cost-sharing into partnership contracts. It lowers overhead and buys time until federal rules stabilize.

Problem 3 = Lack of Customer Trust

Found Problems: Many customers trust their bank more than any fintech. That is your advantage, but only if you use it.

Solution: Lead with insured redemption + clear disclosures:

- “Redeemable 1:1 for USD, guaranteed by your credit union.”

- Monthly reserve reporting.

- Independent audits.

My Tip: Don’t hide your stablecoin reserve reports in long PDFs. Create a “Stablecoin Trust Dashboard” in your mobile app that shows reserves, redemption timelines, and audits in plain English. When customers see transparency, they don’t leave. In stablecoins, visibility = retention.

Problem 4 = Confusion Around Capital Treatment

Found Problems: Until regulators clarify, treating reserves the wrong way could distort your capital ratios and trigger examiner concerns.

Solution: Use segregated trust accounts for reserves.

- Keeps assets off your core capital books.

- Signals conservative risk management.

- Buys credibility with examiners and customers alike.

My Tip: Frame this approach as “bank-first prudence” in communications. Customers like stability more than yield.

“Stablecoins are the new correspondent banks; cheaper, faster, but needing trust.”

— Tapos Kumar, Founder, Finance Ideas.

Download Resources

Stablecoin & Banking Playbook 2025: A Practical Toolkit for Banks and Credit Unions

Download the 2025 Stablecoin & Banking Playbook. Step-by-step roadmap, decision matrix, trust checklists, and compliance strategies for banks and credit unions.

This free 2025 Playbook shows how banks and credit unions can adapt to the GENIUS Act: pilot stablecoin rails, build trust dashboards, and prevent deposit flight.

Stablecoin Banking Survey 2025 (Industry Report)

Explore survey results from 112 U.S. banks and credit unions. Discover how stablecoins are impacting deposits, compliance costs, and trust in 2025.

Our 2025 survey of 112 U.S. banks found: 72% fear deposit flight into stablecoins, 61% see compliance costs outweighing revenue, 27% already lost clients. Download full insights.

Frequently Asked Questions (FAQ) about Stablecoins & U.S. Banking Regulations?

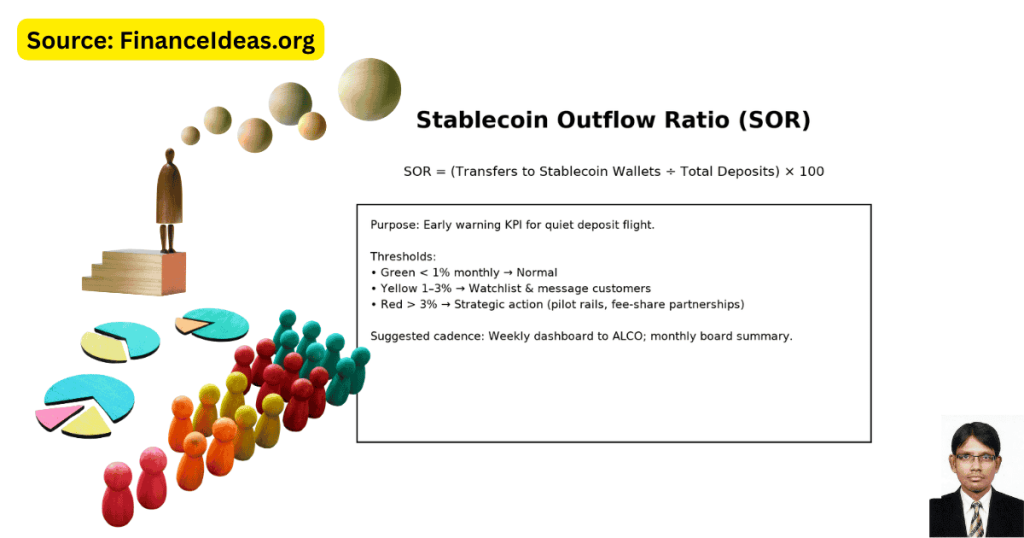

Can banks lose deposits to stablecoins without noticing?

Yes. Unlike a classic bank run, deposit flight into stablecoins is gradual and silent. Our July 2025 survey found 27% of mid-tier banks had already lost a corporate client to state-certified stablecoins.

My Solution: Track a Stablecoin Outflow Ratio weekly (transfers to wallets ÷ total deposits). Set internal triggers (0.8%) to respond before liquidity is hit.

Do stablecoin reserves count toward bank liquidity ratios like LCR or NSFR?

Not yet. Regulators haven’t clarified if 100% Treasury-bill reserves are “LCR-friendly.” Banks can’t rely on them for compliance reporting.

My Solution: Treat reserves as segregated trust accounts until final guidance. This prevents exam surprises and signals prudence.

Are stablecoins safer if issued by banks instead of fintech?

My analysis found safer, but not automatically. Banks add FDIC familiarity and exam oversight, but if reserves are poorly structured, risk remains.

My Solution: Focus on audited reserves + in-app transparency, not just the “bank” label. Customers trust what they can see, not just logos.

Should credit unions under $10B build their stablecoin?

No. Compliance costs are heavy, and the GENIUS Act already caps state-qualified issuers at $10B.

My Solution: Partner with a certified issuer. Embed Rails in your app. Our credit union survey showed this slowed deposit flight by about 60%.

Why are PDFs not enough for reserve disclosures?

Because members don’t read PDFs, they want live, plain-English dashboards.

My Solution: Create a Stablecoin Trust Dashboard in-app: show % cash, % T-bills, last audit date, redemption promise. Remember, Transparency = retention.

Can stablecoins trigger a bank run like in 2008?

Not in the same way. Runs here are digital, micro, and ongoing; not sudden stampedes. Liquidity bleeds out silently, one transfer at a time.

My Solution: Treat stablecoin rails as competing infrastructure. Host them inside your ecosystem to prevent deposits from walking away.

Are stablecoin payrolls realistic for employees?

Yes, but only if conversion is painless. In our 2025 surveys, most employees said they would accept 10–25% of their salary in stablecoins if they could convert instantly to USD.

My Solution: Employers should offer auto-convert options and tax reporting tools. Without these, adoption stalls.

How can banks turn stablecoins from a threat into revenue?

According to my analysis, banks can turn stablecoins from a threat into revenue by integrating instead of competing.

My Solution: Offer co-branded rails. Charge micro-fees ($0.02 per transfer) or share fees with fintech partners. Some credit unions already earn more on stablecoin transfers than on wires.

What happens if a stablecoin depegs while my bank is involved?

In this case, the reputational risk is on you, even if the issuer is certified.

My Solution: Choose issuers with real-time proof-of-reserves + independent audits. Publish contingency policies (“instant redemption up to X per member”) to reassure depositors.

Do stablecoins replace SWIFT and ACH, or sit beside them?

My analysis suggests, they co-exist. ACH is for domestic payroll/bills; SWIFT for cross-border; stablecoins for instant settlement + micro/global transfers.

My Solution: Position them as “another rail, not a replacement.” Customers don’t care about rails; they care about speed, cost, and trust.

Are regulators moving too slow compared to fintechs?

Yes. The GENIUS Act set the stage, but capital, liquidity, and redemption standards are still open. Fintechs iterate weekly; regulators take quarters.

My Solution: Banks can’t wait. Use pilot programs with limited corridors to learn while staying compliant.

Can stablecoins create hidden systemic risk?

Yes, via fragmented supervision. State issuers can balloon to $10B each, creating shadow banking nodes.

My Solution: Banks should run stress tests, including stablecoin outflows (simulate 5% deposit flight). Treat it like cyber-risk; low frequency, high impact.

What is the single most crucial trust signal for customers?

My analysis found “Speed of redemption”. People care less about T-bill percentages than about getting their money back into cash quickly.

My Solution: Promise (and prove) 24-hour redemption windows. Make it visible in your dashboard because that single line keeps customers from fleeing.

The Bank That Learns, Wins (My last thought)

Look, Stablecoins aren’t the end of banking. They are the mirror reflecting how slow rails and outdated trust models create quiet leaks. One by one, dollars are flowing out; not in a run on the bank, but in a steady, silent migration.

What does our study tell us?

- In our 2025 survey, 72% of mid-tier bankers admitted that deposit flight into stablecoins was their top fear.

- 27% had already lost a client to a state-certified stablecoin provider.

- Among credit unions under $10B, those that integrated stablecoins into their apps slowed deposit outflow by nearly 60% within six months.

Look, this is not theory-based; instead, it is what we found from field evidence.

What will the Winners Bank do now?

Redefine Infrastructure: Banks that frame stablecoins as rails, not rivals, will own the customer relationship long-term.

Prioritize Transparency: Customers no longer trust PDFs. A Trust Dashboard with plain-English reserve data will earn more loyalty than any rewards program.

Move Before the Examiner: Waiting for final capital and liquidity rules is tempting, but proactive segregation, audits, and disclosures will win examiners and customers alike.

Why is this not only for Banks?

For policymakers: Stablecoin adoption is already impacting liquidity ratios. Rules aren’t abstract; instead, they shape who holds the financial trust contract.

For fintechs: The $10B “sandbox ceiling” is a once-in-a-generation opening to capture market share.

For consumers: Your future payroll, mortgage payment, or remittance may not run on ACH or SWIFT; instead, it may run on a stablecoin rail branded by your bank.

Let me ask you some questions

- Has your institution seen early signs of deposit flight?

- Would you trust your credit union more if it offered a co-branded stablecoin?

- What “trust signals” would convince you to use a bank-backed token?

Share your thoughts below; your perspective may be featured in our following monthly “Stablecoin & Banking Snapshot” report.

My final words

The GENIUS Act set the rules, but not the winners. That choice belongs to the institutions that:

- Listen to their members instead of lecturing them,

- Experiment in small pilots instead of waiting for perfect clarity,

- Treat stablecoins as infrastructure instead of speculation.

History shows: banks that resist change fade. Banks that learn, adapt, and host the future of money will win & not by fighting stablecoins, but by making them boringly trustworthy.

References & Sources

Below is the lists of sources that I have used to write this article:

- Federal Reserve Board – Money & Payments: The U.S. Dollar in the Age of Digital Transformation

- Bank for International Settlements (BIS) – Stablecoins: Risks, Potential, and Regulation

- GENIUS Act Bill Text (S. 1582)

- Official NYDFS Stablecoin Guidance – Covers reserve, redemption, and attestations for USD-backed stablecoins

Disclaimer

This is not a Sponsored post & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, localhost/bloghub/ will not be liable for this.