“I didn’t know how I would pay for groceries, let alone the electric bill, until Thursday. But my paycheck wasn’t arriving until Monday.”

That is what one of my clients (a school teacher) told me during a budgeting seminar. Her increasingly familiar story highlights the growing need for short-term financial lifelines that don’t come with the crushing interest rates of payday loans. Apps like Dave and Brigit are stepping into this space.

As a finance professional who has advised startups and families, I have seen how these apps are impacting Americans in real time. Here is how do you compare dave app vs Brigit, why they are not your typical payday loan, and how to use them smartly.

Key takeaways:

- Download both apps and compare interfaces. Try a test advance.

- Use the budgeting features actively. Don’t ignore alerts.

- Create a 3-month emergency fund. Use these apps only as a backup.

- Review monthly subscriptions. Cancel what you don’t need.

Related Articles

-

Predictive Spending: Your App Knows When You Will Break Your Budget—Here is How

-

AI Budgeting for Couples: Why Smart Couples Use AI to Avoid Money Fights?

-

Bill Negotiator Bots vs. Human Budgeting: Do Bill Negotiator Bots Really Work? I Tested Them.

-

AI subscription fatigue overwhelm : Feeling Overwhelmed? AI Can See It Before You Do

-

Micro-AI Budget Nudges vs. Monthly Plans: Why 60-Second AI Nudges Are Killing Spreadsheets in Budgeting

What Are Cash Advance Apps Like Dave and Brigit?

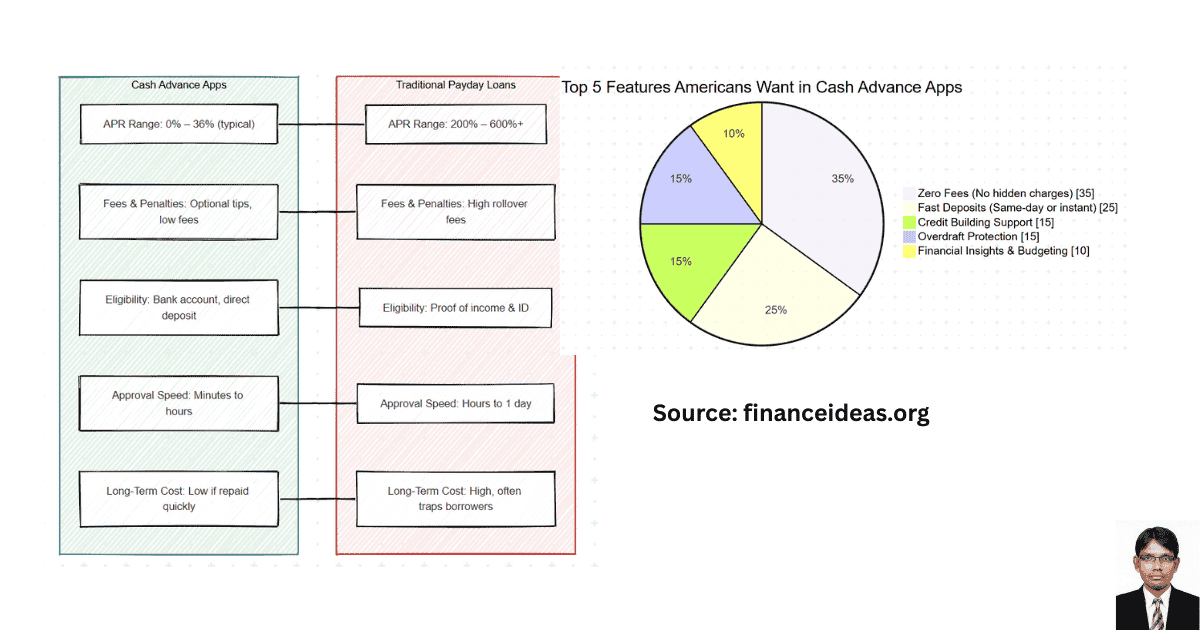

Dave and Brigit apps give users small, interest-free cash advances against upcoming paychecks to cover expenses like rent, groceries, or emergencies.

- Dave: Offers up to $500 with no interest, just a small tip, and an optional monthly subscription ($1 monthly). It also includes a budgeting tool and alerts for upcoming bills.

- Brigit: This option offers up to $250, requires a $9.99 monthly subscription for cash advances, and comes with a suite of budgeting and credit monitoring tools.

Unlike payday loans, which often trap borrowers in a cycle of high-interest debt, these apps operate more like temporary cash flow bridges.

Dave vs Brigit: My Side-by-Side Comparison?

Below, I have given a feature comparison so you can make quick decisions.

| Feature | Dave | Brigit |

| Advance Limit | Up to $500 | Up to $250 |

| Fees | $1/month + optional tip | $9.99/month (no tips) |

| Credit Check? | No | No |

| Extra Tools | Budgeting, overdraft alerts | Credit builder, budgeting |

| Speed of Delivery | Instantly (with fee) | Instantly (with fee) |

| Who It’s Best For | Freelancers, gig workers | Salaried employees |

How Do Dave and Brigit Compare to Traditional Payday Loans?

In my professional experience, Dave and Brigit offer a smarter and safer path compared to traditional payday loans. Why? These apps give users access to small cash advances without charging interest, requiring credit checks, or applying aggressive collection tactics. Unlike payday lenders that often trap people in cycles of high-interest debt, Dave and Brigit act as short-term financial tools—designed to bridge a gap until payday, not profit from your financial stress.

By replacing predatory fees with transparent memberships or optional tips, both platforms offer a more ethical and user-focused solution for urgent cash needs.

The Real-World Difference: Dave vs Payday Loans

Let me share a real story.

John, a rideshare driver in Phoenix, once took a $300 payday loan to fix his car. Due to fees and interest, he ended up repaying $460.

Now, using Dave, he can get a $300 advance with zero interest and pay back on payday. That is a savings of over $160, and it doesn’t damage his credit or put him into collections.

The difference? Payday loans profit from your desperation. Dave and Brigit are built around your paycheck.

What Makes Dave & Brigit Apps “Better”?

I encountered a common question from a user: If I used it right, what makes Dave and Brigit better? So, if you are a serious reader, then asking similar questions is expected. Below, I have given a short description by identifying key consumer usage to highlight what makes these apps better.

No Predatory Interest: Traditional payday loans charge APRs upwards of 300%. These apps do not.

No Credit Damage: There are no hard credit pulls.

Smart Alerts: They warn you about overdrafts or upcoming expenses.

Financial Tools Built-In: Budgeting, credit building, and alerts help prevent future crises.

However, remember that these apps are not magic; so, use them responsibly. Why? “These apps are not a replacement for financial planning.” They are tools, not solutions. For those who need advances every paycheck, it is time to reassess budget. That is where their built-in tracking tools shine.

I had a client who used Brigit to cover groceries for two months. Then, using Brigit’s budgeting dashboard, she discovered she was overspending $120 per month on subscriptions she forgot she had. Problem solved without more debt.

Are Dave vs Brigit the Best Cash Advance Apps?

Dave and Brigit lead the market, but others like Earnin, MoneyLion, and Albert are catching up. Still, Dave’s flexibility and Brigit’s credit-building make them top-tier choices.

Concluding Thought

Now judgement day come & It is high time to make final decisions from dave app vs Brigit. So, which apps should you pick? Look, I always provide neutral analysis which means give both perspective & you have to decide. Therefore, my advice is:

- Choose Dave if you want higher limits and are a gig worker or freelancer.

- Choose Brigit if you value budgeting tools and want to improve your credit.

Keep in mind that either is vastly safer than payday loans. But neither replaces the need for an emergency fund.

Frequently Asked Questions (FAQ)

What is the Brigit app?

Brigit is a financial app that manage personal finance & allows users to track expenses, budget effectively, and access cash advances before their next paycheck.

What is the Dave app?

The Dave app is a financial tool designed to help users avoid overdraft fees and access small cash advances.

How quickly can I receive funds from Dave & Brigit apps?

Standard transfers are free and may take Dave 1 to 3 business days. Express transfers are available for a fee and can deliver funds within minutes.

Brigit offers instant cash advances, typically delivering funds within minutes. Keep in mind that the timing may vary based on your bank.

Can using Dav & Brigit apps help improve my financial habits?

Yes. Both apps offer tools to help users manage their finances. Dave provides budgeting tools and side hustle suggestions. At the same time, Brigit offers budgeting tools and smart alerts to help users avoid overdraft fees.

Are there any risks of using cash advance apps?

Yes, cash advance apps have some associated risks. Yeah, these apps can provide quick financial relief, but you should use them responsibly. Relying heavily on cash advances can lead to a cycle of debt. Additionally, some users have reported issues with fees and customer service.

How do these apps (Dave and Brigit) compare to traditional payday loans?

In my professional experience, Dave and Brigit offer a smarter and safer path compared to traditional payday loans. Why? These apps give users access to small cash advances without charging interest, requiring credit checks, or applying aggressive collection tactics. Unlike payday lenders that often trap people in cycles of high-interest debt, Dave and Brigit act as short-term financial tools; designed to bridge a gap until payday, not profit from your financial stress.

By replacing predatory fees with transparent memberships or optional tips, both platforms offer a more ethical and user-focused solution for urgent cash needs.

References & Sources

Below is the lists of sources that I have used to write dave app vs Brigit article:

- Dave App Official Website

- Brigit App Official Website

- How Apps Like Dave Are Helping Americans Avoid Payday Loans

Disclaimer

This is not a Sponsored post for dave app vs Brigit & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, Finance Ideas will not be liable for this.