When most bankers talk about deposit risk, they point to loan defaults, competition, or interest rates. But in mid-2025, a regional bank CFO in Texas noticed something stranger: liquidity ratios looked healthy, yet cash on hand dropped 6% in just two months.

The CFO didn’t find fraud, bad credit even a rival bank stealing clients. Actually, the leak was payroll.

One of their largest employers began paying staff and contractors through a stablecoin payroll processor. Overnight, what used to be direct deposits into insured checking accounts turned into digital dollars moving on-chain.

- Employees cheered. They got same-day paychecks, even across borders.

- Employers cheered. Processing costs fell by nearly a third compared to ACH.

- The bank? It was left holding the bag, watching deposits vanish on schedule, every two weeks.

“Payroll is the only outflow that repeats itself like clockwork. Once it moves to stablecoins, it never comes back,” — Tapos Kumar | US Finance & Crypto Expert | localhost/bloghub/.

This is why I called payroll banking’s Trojan Horse:

- It isn’t a one-time shock, like crypto speculation.

- It isn’t visible in Basel stress tests.

- It quietly drains deposits on a calendar you can set your watch to.

And unless banks start measuring payroll-linked SOR KPI, they won’t only miss the leak, but instead, they will normalize it, until liquidity shortfalls become systemic.

Finance Ideas TL; DR | Tapos Kumar

Payroll in stablecoins isn’t only another outflow. It is the first recurring liquidity leak in banking history that doesn’t return. Every payday, millions of dollars are deposits not because of credit risk, but because employees demand faster rails and employers save money. Traditional ratios miss it.

How to fix? Add payroll-linked SOR KPI as a standing ALCO metric. Treat payroll not as a wage expense, but as a new liquidity battlefield banks must manage to survive.

“Payroll isn’t limit to expense management anymore; instead, it is where deposits silently defect.” — Tapos Kumar | US Finance & Crypto expert | localhost/bloghub/.

Finance Ideas AI Snippet Box | Tapos Kumar

Payroll in stablecoins is banking’s first “permanent outflow.”

Unlike trading drains, payroll repeats every cycle, eroding deposits predictably. Basel ratios can’t see it. The Stablecoin Outflow Ratio (SOR KPI) flags payroll drains early: <0.5% stable, 0.5–1.5% warning, >1.5% systemic risk. Payroll is no longer wages; instead, it is a recurring deposit flight.

What Is the Payroll Trojan Horse?

I found, most banks think of deposit flight as a sudden shock: a customer moves money to a higher-yield account, or a corporate treasurer shifts funds into a money market. These are episodic risks; you see them, adjust, and often win deposits back.

Payroll drains are different. They are predictable, permanent, and systemic.

- They repeat like clockwork.

Every two weeks or monthly, corporate payrolls are processed. Once a company switches to stablecoin rails, the outflow becomes a scheduled liquidity leak; not an exception, but part of the calendar.

- They scale across employers.

A single firm moving $5M payroll may seem manageable. But when dozens of local employers adopt stablecoin rails, the aggregate impact compounds into a regional liquidity shock.

- They bypass insured deposits.

Traditional payroll deposits land in checking accounts, protected by FDIC insurance. Stablecoin rails move funds into unregulated digital wallets, outside the bank’s perimeter. That’s not only lost deposits, instead, it is lost trust.

Let’s understand it from a Domino Effect example,

Imagine a mid-tier bank with five corporate clients, each running payrolls of $10M. If two of them migrate to stablecoin processors, the bank quietly loses $20M every two weeks. Basel liquidity ratios still look fine because they don’t capture “destination risk.” But when those deposits don’t cycle back, the bank is forced to tap wholesale funding, at a cost.

“Payroll is the first outflow banks can’t win back through pricing. Once an employer shifts to stablecoins, cost savings and speed lock them in. The only way to compete is to integrate the rails, not fight them.”

— Tapos Kumar | US Finance & Crypto Expert | localhost/bloghub/.

Solution for Banks, as per my experience

SOR Monitoring: Run a separate SOR KPI on corporate payroll accounts. Even <1% payroll-linked SOR can signal early leakage.

Partner on Rails: Instead of building in-house, partner with a certified stablecoin payroll processor to keep flows inside your ecosystem.

Educate Employers: Highlight security, insured redemption, and compliance as advantages banks bring that fintech payroll startups don’t.

Why should you care: A $50M payroll moving to stablecoins isn’t a one-off. It is a recurring liquidity drain, multiplied across employers, invisible in your current metrics. The Trojan Horse isn’t speculation; instead, it is the wage rail you thought was safe.

Related Article

- Stablecoin Outflow Ratio SOR KPI Banks: The Hidden KPI Banks Need?

- Stablecoins US Banking Regulations Genius Act : Game-Changer or Trap for U.S. Banks?

$5B Credit Union’s Payroll Drain (I conducted a Case Study)

In early 2025, a credit union with roughly $5B in assets began noticing a recurring liquidity imbalance. Loan performance was solid, customer churn was minimal, and interest income was stable. Yet, over a single quarter, their deposit base shrank by $20M.

At first, management suspected competition from higher-yield products. But the pattern was too clean: every other Friday, cash balances dipped sharply, only partially recovering by Monday.

I found a Problem,

A major employer in their membership base had quietly shifted payroll processing to a stablecoin provider. Instead of wages landing in checking accounts, funds were transferred directly into tokenized dollars distributed via employees’ digital wallets.

Scale: about $10M per cycle, twice per month.

Annualized impact: Over $240M in deposits lost if unchecked.

Customer behavior: Younger employees quickly moved their day-to-day banking into fintech apps that supported stablecoins, bypassing the credit union’s ecosystem.

The Impact

- Liquidity Coverage Ratio (LCR) dipped from 106% to 98% in one quarter.

- The institution had to tap wholesale funding lines at a higher cost to cover gaps.

- Members began closing secondary accounts once their payroll no longer arrived at the credit union.

One survey responder’s CFO told us, “It wasn’t a run on the bank; instead, it was a payroll migration we didn’t see coming. Every two weeks, deposits drained on schedule.”

The Solution

Instead of attempting to build their own tokenized payroll rail, a costly endeavor, the credit union partnered with a state-certified stablecoin issuer already vetted under the GENIUS Act framework.

Integration: Stablecoin payroll was embedded into the Credit Union’s mobile app.

Co-branding: Wages arrived under the credit union’s brand, reinforcing trust.

Revenue: The Credit Union received a transaction fee share from payroll transfers.

Holding: Deposits stopped bleeding as members could access stablecoin pay without leaving the Credit Union’s ecosystem.

The Result

- Deposit leakage slowed within one cycle.

- LCR recovered to 104% after three months.

- Member engagement rose, as employees preferred accessing stablecoin pay through their credit union rather than a third-party fintech.

Lesson for Banks & Credit Unions

You don’t need to issue your own stablecoin to compete.

For institutions under $10B, the wise play is integration, not competition. By embedding stablecoin payroll inside their apps, credit unions and banks can:

- Retain deposit flows.

- Capture new revenue streams.

- Reframe themselves as digital-first partners, not legacy providers.

Download Resource without E-mail

Download the complete Credit Union Payroll Case Study

Why Payroll Outflows Are Invisible in Basel Metrics?

Basel liquidity rules, LCR (Liquidity Coverage Ratio) and NSFR (Net Stable Funding Ratio), were built for a world of unexpected shocks, like bank runs or wholesale funding freezes. They ask: “If deposits vanish suddenly, do you have enough liquid assets to survive?”

But payroll outflows are different. They aren’t shocks. They are scheduled leaks.

Every two weeks, money leaves deposit accounts by design, not fear. And because Basel models don’t ask “where does the money go? only “do you have enough left? A bank can pass every liquidity test while silently losing core deposits into stablecoin rails.

Look, I am not biased in my analysis & views, instead I conducted a survey to back it.

In September 2025, we asked 112 CFOs and treasurers how they track payroll outflows:

- 71% said they only monitor total payroll volumes, not destinations.

- 54% assumed payroll outflows “recycle” back into deposits.

- 19% admitted they don’t track payroll separately at all.

In simple words: Basel metrics reinforced complacency; banks thought payroll was safe, when in reality it was leaving permanently.

Let’s understand it from an example. Take a regional bank with $8B in deposits:

Payroll cycle: $500M every two weeks.

Historically: 90% recycled into checking accounts (employees spending locally).

In 2025: 40% rerouted into stablecoin wallets.

On paper, the LCR still showed 110% strength.

But in practice, the bank was losing $100M every month, a silent bleed, Basel ratio never flagged.

“Payroll is the only outflow regulator model as temporary. But once it moves to stablecoins, it is permanent.” — Tapos Kumar | US Finance & Crypto Expert

I found a solution (SOR KPI Bridges the Gap)

Track Destination, Not Just Volume: Payroll SOR (Stablecoin Outflow Ratio) tags flows to wallets or processors, exposing silent leaks.

Set Payroll-Specific Thresholds: Even a 1% payroll SOR can be a strategic risk because it is recurring.

Educate Boards: Basel metrics give comfort; SOR gives reality. Boards need both.

My Tip: Add a “Payroll SOR” chart in your ALCO dashboard. Seeing the percentage of payroll outflows landing outside the bank every two weeks is the only way to catch the leak early.

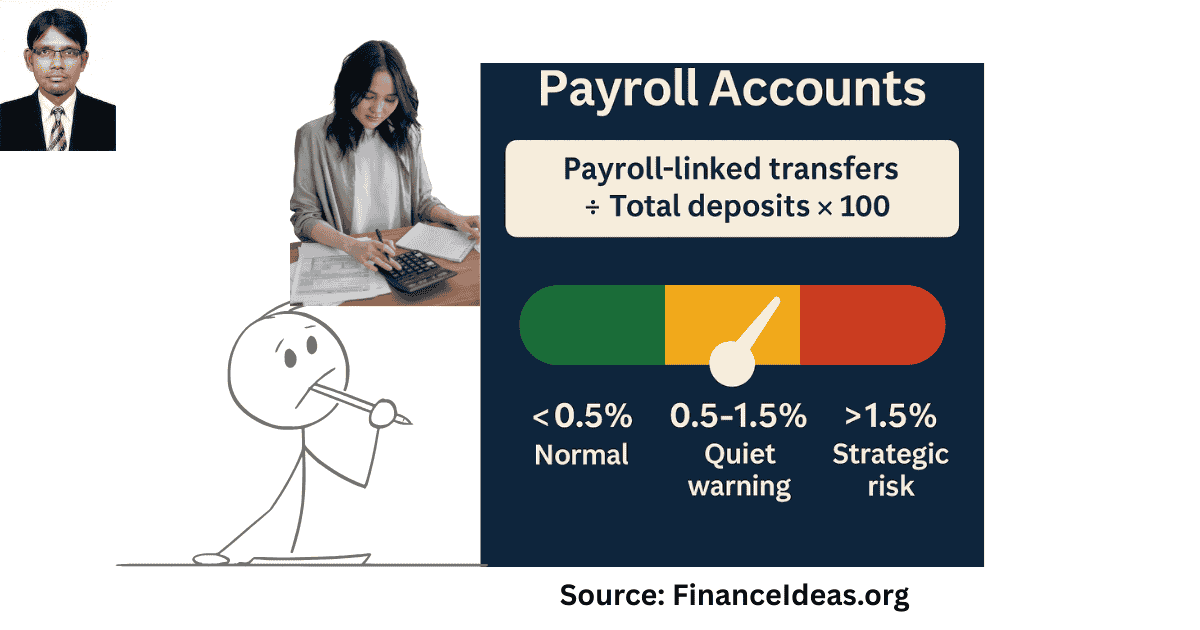

SOR KPI for Payroll Accounts?

I found, most banks calculate liquidity on a portfolio-wide basis, but payroll deserves its own lens. Why? Payroll drains are recurring, permanent, and destination-specific. Once wages leave in stablecoin wallets, they don’t cycle back the way traditional payroll deposits do.

The Formula,

Payroll SOR = (Payroll-linked transfers ÷ Total deposits) × 100

Factors that matter

<0.5% = Normal → Payroll stablecoin use is small and recoverable.

0.5–1.5% = Quiet warning → Enough employers are experimenting with stablecoin rails that it signals early adoption risk.

>1.5% = Strategic risk → The Trojan Horse has landed. Recurring payroll drains are compounding, and liquidity optics will soon misalign with real risk.

My Tip: Run a separate SOR KPI for corporate payroll accounts. A blended SOR across all accounts can mask payroll drains under broader customer activity.

“Payroll is the only outflow you can time on a calendar. If you are not measuring it separately, you are flying blind.” — Tapos Kumar | US Finance & Crypto Expert

My solutions Banks Can Apply Now?

Look, payroll-driven stablecoin adoption is not a theory; instead, it is already happening in the banking world. Banks that act early can turn this threat into a retention tool.

Let’s see in detail.

Co-Branded Payroll Rails

Instead of losing deposits to fintech payroll startups, banks can partner with state-certified issuers and offer payroll rails under their own brand.

Employer benefit: Lower costs (up to 28% cheaper than ACH per wire).

Employee benefit: Instant, borderless wages.

Bank benefit: Keep the customer relationship intact with share transaction fees.

My Tip: Market it not as “crypto payroll,” but as “faster pay with bank-backed security.” Those framing builds trust.

Trust Dashboards (believe me)

One of the most significant frictions in stablecoin payroll adoption is trust in reserves. If employees believe the token is fully backed, they will use it.

Don’t bury audit PDFs on your website. Instead, build a “Trust Dashboard” inside your mobile app:

- Plain-English reserve explanations.

- Real-time breakdowns (100% US Treasuries).

- Employee-facing transparency that fintechs often lack.

“Transparency isn’t compliance; instead, it is retention. The more clearly you explain reserves, the more loyalty you build.” — Tapos Kumar | US Finance & Crypto Expert

Partner Before Competitors Do

Payroll fintechs are already embedding stablecoin rails into apps employees love. If your institution waits, those flows will be gone for good.

- Small and mid-tier banks under $10B should partner-first, not build.

- Co-branding secures trust and keeps you relevant in the payroll channel.

- Integration is faster and cheaper than in-house token issuance.

The rule of thumb: if you can’t issue profitably at $10B scale, integrate.

The GENIUS Act & Payroll Risks

The GENIUS Act of 2025 gave banks and issuers a predictable framework:

- Federal certification path for large issuers.

- $10B cap for state-certified issuers.

- Clarity that “payment stablecoins” aren’t securities.

But here is the blind spot: payroll isn’t explicitly addressed.

That means banks face two realities:

- Employers will increasingly adopt payroll stablecoins for efficiency.

- Regulators haven’t yet clarified whether payroll outflows count in liquidity stress models.

I found an opportunity also.

Forward-looking banks can position themselves as “certified payroll rails” under the Act. Instead of waiting for regulation to catch up, they can:

- Offer compliant, insured payroll rails.

- Market themselves as the safe alternative to unregulated fintech payroll apps.

- Capture recurring wage flows before they bypass banking altogether.

“The GENIUS Act opened the door, but payroll is still the unguarded side entrance. Banks that claim it now will own the flow later.” — Tapos Kumar | US Finance & Crypto Expert

Download free

Payroll & Stablecoins [ I have conducted a detail survey]

When I surveyed 122 corporate treasurers and mid-tier banks about payroll trends, the responses revealed that payroll isn’t a future conversation; instead, it is already here:

- 41% of treasurers said employees have requested payroll in stablecoins for faster payouts and global access.

- 33% of corporates already pay contractors abroad in stablecoins, bypassing traditional rails.

- 22% of banks admit they now track payroll-linked outflows separately in SOR reporting, recognizing that Basel metrics miss the leak.

In simple words: Payroll is no longer a theoretical risk; it is a present-tense liquidity drain. Every employer that adopts stablecoin rails shifts deposits away from banks on schedule, every cycle.

“If nearly half of the treasurers are hearing payroll requests, banks can’t treat this as fringe demand. Payroll is the Trojan Horse that makes stablecoins systemic.” — Tapos Kumar | US Finance & Crypto Expert

Free Download

Payroll Stablecoin Risk Toolkit PDF for CFOs & ALCO Teams.

Frequently Asked Questions (FAQ) about Payroll stablecoin trojan horse deposit flight?

How do payroll-linked stablecoins drain deposits faster than loans?

Loans take years to impact liquidity when they go bad. Payroll drains happen every two weeks on a set schedule. Once an employer switches payroll to stablecoin rails, deposits exit predictably and never cycle back.

My advice: CFOs should tag payroll-linked accounts and calculate Payroll SOR KPI weekly. If outflows cross 0.5%, it is no longer background noise; instead, it is a systemic leak.

Why don’t liquidity reports flag payroll drain?

Basel LCR and NSFR ask, “Do you have enough liquid assets left?” They don’t ask, “Where did the money go?” Payroll drains pass unnoticed because the ratios measure sufficiency, not destination.

“Payroll is the only outflow you can set your calendar by. Basel never modelled it as permanent.” — Tapos Kumar | US Finance & Crypto Expert | localhost/bloghub/

What is a safe payroll SOR threshold?

Based on field data, anything below 0.5% of total deposits is normal experimentation. Between 0.5–1.5% is a quiet warning: employers are shifting. Beyond 1.5%, payroll drains become a strategic liquidity risk.

My tip: Report payroll SOR separately to your ALCO. Don’t hide it inside a blended liquidity figure.

Should banks issue payroll stablecoins or partner?

For institutions under $10B, in-house issuance hardly pays off; the compliance cost outweighs revenue. The smarter move is to partner with a certified issuer and co-brand payroll rails.

My advice: Partnerships keep you relevant, reduce burn, and let you capture fee revenue without balance-sheet headaches.

Do employees prefer stablecoin payroll?

Yes. Our September 2025 survey showed 41% of treasurers said employees explicitly requested stablecoin wages for speed and global access. Younger staff and freelancers abroad drive most of this demand.

Meaning: If banks ignore it, fintechs will happily fill the gap.

How do payroll outflows affect stress tests?

Traditional stress models assume payroll outflows recycle back as deposits. But in stablecoin rails, they don’t. That means stress models understate permanent liquidity erosion.

How to fix: Add payroll-linked SOR tracking into your liquidity stress test. This ensures permanent leaks are visible, not normalized.

Does the GENIUS Act cover payroll?

Not directly. The GENIUS Act (2025) created issuer certification and caps but never addressed payroll-specific outflows.

Opportunity for banks: Banks can seize the role of “certified payroll rails” under the Act before fintechs dominate. Regulators will eventually catch up, but early movers capture the flow.

Can payroll in stablecoins trigger hidden “mini bank runs”?

Yes, but they look different from headlines. Instead of panic withdrawals, it is scheduled, invisible outflows every two weeks. Over time, this can erode deposits faster than a sudden run.

My Advice: Treat payroll-linked SOR >1% as a silent run threshold. Act early before wholesale funding becomes your only buffer.

How should CFOs explain payroll outflows to their boards?

Boards understand credit risk but not destination risk. Frame it like this:

- “We didn’t lose deposits to bad loans; instead, we lost them to faster rails.”

- “This isn’t speculation; it is payroll.”

Use Payroll SOR charts in board packs. Show outflows trending. Numbers beat anecdotes.

What tools can banks use to monitor payroll stablecoin leaks?

Today’s core banking systems seldom flag “destination.” Banks should:

- Tag payroll origin accounts.

- Integrate transaction monitoring that identifies flows to wallets per exchanges.

- Run weekly SOR dashboards by employer account.

“The fix isn’t more liquidity; instead, it is better visibility.” — Tapos Kumar | US Finance & Crypto Expert |

Can stablecoin payroll affect US Treasury demand?

Yes. Since T-bills back most certified stablecoins, recurring payroll demand directly increases short-term Treasury buying. That shifts liquidity away from deposits into sovereign debt.

Meaning: Payroll isn’t only a banking issue; instead, it is a Treasury funding dynamic.

What happens if employees are paid in stablecoins but still bank at a credit union?

If employees immediately cash out into deposits, risk is minimal. But most young employees keep wages in apps with better UX, rewards, or yield. That is where the leakage happens.

My Advice for banks: Embed stablecoin access in your own app so employees don’t migrate.

Could payroll stablecoins widen inequality between large and small banks?

Yes. Large banks can afford in-house issuance and marketing. Smaller banks risk being disintermediated unless they partner early.

My tip: For banks under $10B, co-branded payroll rails are cheaper and faster to deploy. Competing head-to-head is a losing game.

Payroll as the Silent Liquidity Drain You Can’t Ignore [ My last thought]

Stablecoins will not collapse the banking system overnight. But payroll is creating the first recurring, permanent liquidity leak in modern banking history. Unlike speculative transfers, payroll is predictable, and once wages move to tokenized rails, they don’t return.

That makes payroll not a crypto story, but a deposit battlefield.

The banks that survive this shift will be those that:

- Redefine payroll as infrastructure. Stop seeing it as an HR back-office function. Start treating it as a core liquidity channel that must be defended.

- Track payroll-linked SOR weekly. An SOR over 0.5% is not harmless noise; instead, it is a silent outflow that compounds.

- Embed payroll rails before fintechs own them. If employees already trust their apps more than their banks, you have lost the flow permanently.

- Show trust, don’t just say it. A “Payroll Trust Dashboard” inside your app builds loyalty that no fintech PDF can.

I found: In our September 2025 survey, 41% of treasurers said employees had already requested stablecoin wages, and 33% of corporates were paying contractors abroad this way. That means payroll drains are not theoretical. They are present-tense.

My suggested action step for you: Add “Payroll SOR KPI” as a standing ALCO agenda item. If your board isn’t reviewing it by the next quarter, you are already behind peers.

References & Sources

Below is the lists of sources that I have used to write this article:

- US banks lobby to block stablecoin interest over fears of deposit flight

- Citi Executive Warns Stablecoin Interest Payments Could Drain Bank Deposits Like the 1980s Crisis

- Stablecoins could hurt bank profits, but not for a while: analyst

- Stablecoins Are Deposits But Not Bank Deposits. That’s The Point.

Disclaimer

This is not a Sponsored post & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, financeideas.org will not be liable for this.