We got the money. Just not when we needed it. I often hear such lines from American founders via LinkedIn. I congratulate them, but they reply with sad words. Hmm, funding approval takes time & this is normal. Why will the bank approve the finance? To find the answer to this question, Banks take time to assess your profile.

I don’t think anything is wrong here.

But money can be useful if founders get it at the correct time. So, I can’t ignore founders’ concerns. To identify the key reasons, I have surveyed more than 1,000 founders. Some founders agree that funding approval is the main problem. But most of them think that only the right time approval could be beneficial for the business. Yeah, you have many questions, & I have good news for you. I am writing this article to answer all your questions so that you can make better startup decisions.

Sit with some time & read about bank timing vs founder timing. I hope you will find my article helpful. Let’s start with the following:

Finance Ideas AI snippet box | Tapos Kumar

Timing misalignment loss?

Timing misalignment loss is the hidden cost startups face when funding arrives too late; approval is granted, but the opportunity time has already passed. U.S. banking surveys show that loan timing follows system stability patterns (not founder urgency), meaning capital can miss the time when it is most required.

Related Articles

- Loan for start up: Fund Your Dream

-

How US lenders define risk: If Lenders Say You’re “High Risk,” Read This First

-

Why Startup Loan Rejections Feel Vague: And Why Lenders Stay Silent?

-

What lenders see in bank statements: But Never Explain

-

90-day plan after startup loan denial: Here’s the Smarter 90-Day Move

-

Risk memo after loan denial: What lenders document about you?

-

Cash conversion cycle lenders model: Denied Again? Read this

-

Bank portfolio math: Why Perfect Borrowers Hear No

-

Capital preservation bias: What Founders Get Wrong?

-

Founder distribution problem: The Hidden Risk Behind Owner Pay

- Loan approval momentum effect: What Most Founders Miss?

- Bank relationship capital: How Founders Build Banker Trust

-

Interest rates vs risk appetite: The Credit Market Secret Most Founders Miss

-

Industry credit cycles: The Lending Window Most Founders Miss

-

Financial statement stability optics: How Banks Read Your Financials?

-

The internal risk ladder: It is Not What You Think

-

The hidden cost of being almost bankable: Here’s Why You’re Losing Money

-

Credit Fatigue: Lean How to Fix It?

-

Pre-approval illusion: You Think You’re Approved but You’re Not

Why do startup funding rounds fail (I found a dual timeline problem)?

Starting a business in America seems like a race against time. Opportunities arise fast: a big customer order, a supplier deal, or the perfect person to hire. But when you go to the bank for funding, you quickly realize you and the lender aren’t running on the same time. That mismatch is where good deals start to fail.

As a founder, your timing is closely tied to urgency. Like

- A new customer wants the product immediately.

- A supplier offers a discount but only for 30 days.

- A competitor creates a market gap.

Your mindset is: If we don’t perform over the next 30–60 days, this chance will disappear.

So, your situation is like catching a flight; the plane leaves whether you are ready or not.

Banks, on the other hand, move slowly because their job is to reduce risk. They want to check whether this is safe right now?

Their process will be as follows:

Early stage: Looks promising, but let’s watch.

Middle stage: Maybe, but we need more proof.

Final stage: Okay, now we decide.

I have conducted a case study on a small food startup in Austin. They land a deal with a grocery chain that wants their product on shelves in 45 days. The founder rushes to the bank for financing to scale production.

The bank likes the business but wants to see three months of steady sales before approving the loan. By the time the bank is ready, the grocery chain has moved on.

After analyzing this business case, I found that the deal didn’t fail because the product was bad; instead, it failed because the timing didn’t match.

So, don’t make advance business decisions based on positive signals. You have to make decisions in line with the aligned timelines.

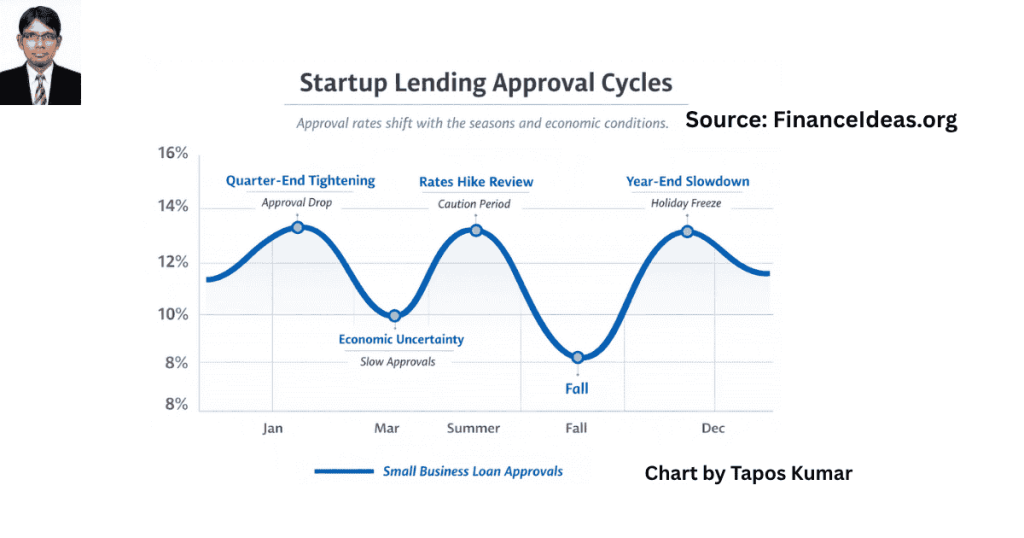

I recommend that founders notice the seasonal credit pattern?

I found that most American founders assume that funding means applying, qualifying, and getting approved. But the truth is, credit moves in cycles. Banks adjust their lending appetite in response to reporting deadlines, interest rate changes, and economic uncertainty.

So, you need to know these cycles; otherwise, you risk applying at the wrong time. Let me explain it in detail.

Why does credit move in cycles?

First, you have to understand that banks aren’t only assessing your deal. They are managing their own timing risk. Don’t trust me. Let me share some federal data.

According to the Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS), lending standards tighten at predictable points in the year, especially around quarter‑end and year‑end. FDIC data also shows that small business loan approvals fluctuate by 5–12% depending on reporting cycles and rate changes.

Considering the above facts, I will share 4 seasonal patterns to help you understand their impact.

- Quarter‑end tightening

- Risk appetite contracts as banks prepare quarterly reports.

- Approvals slow down and face extra scrutiny.

- Deals that looked fine in mid‑quarter may stall in the last two weeks.

According to our study, in Q4 2023, small business loan approvals dropped 7% in the final month of the quarter compared to mid‑quarter levels.

- Year‑end conservatism

- Balance sheet positioning is more important than new deals.

- Almost all approved loans often freeze until January.

- Slow progress isn’t rejection; it is timing.

According to our study, approval rates at big banks fell from 14.9% in October 2023 to 13.6% in December 2023, before rebounding in January.

- Post‑rate change caution

- After Federal Reserve rate hikes, banks recheck models.

- Deals approved under old assumptions may be delayed or repriced.

- Same business, different timing context.

We found that following the Fed’s March 2023 rate hike, small business loan approvals fell by nearly 13% in the following quarter.

- Uncertainty phases

- During economic volatility, banks stretch decisions.

- Internal arrangement takes longer.

- Approval speed drops, even for strong applicants.

We found that in 2020, during pandemic uncertainty, approval rates at large banks fell below 10%, despite strong demand.

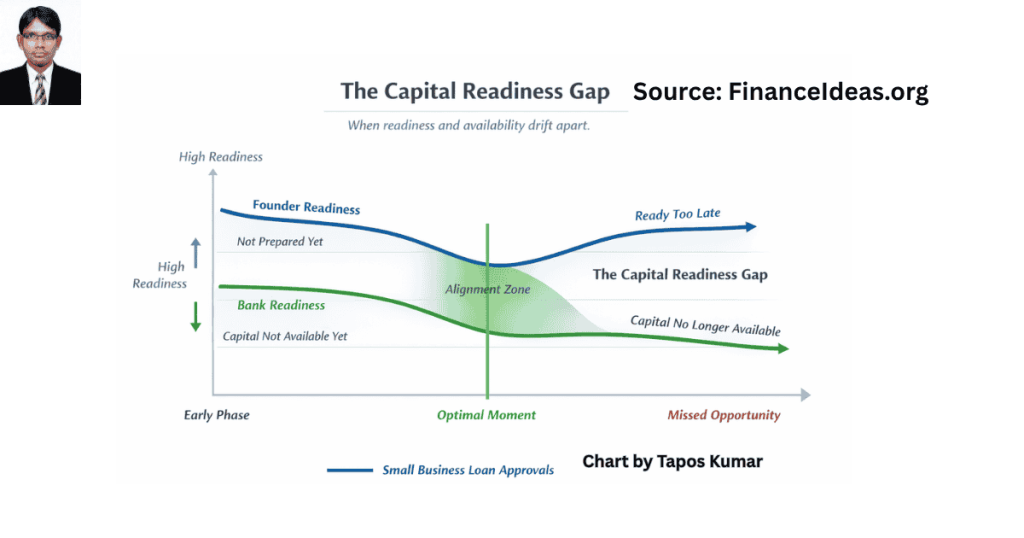

Let me tell you about the capital readiness gap?

Did you know that even when timing looks perfect, funding can fall apart? For this reason, there is a hidden mismatch between when capital is available and when you are ready to use it effectively. I call this the capital readiness gap, and it costs startups across America every year.

Why is the capital readiness gap more important?

As per my analysis, most founders believe that if money is available, they will use it. And, if I am ready, money will be there. Unfortunately, these 2 conditions don’t come sequentially.

For further details, Finance Ideas conducted a small business credit survey & found that 45% of small firms missed funding opportunities because they weren’t ready when credit was available.

Based on this survey, there are two types of capital gap & both are costly.

- You are ready, but the bank isn’t

This one is obvious. You believe it is an urgency and a delay. But you are in a growth phase, & the bank is reducing uncertainty.

While you wait, energy slows, opportunities weaken & plans start to change.

- The bank is ready, but you are late

This one is hidden and more dangerous. It looks like: credit conditions are favorable, approval speed is high & capital is available.

But your documents aren’t ready, your strategy isn’t clear, and you haven’t applied yet. By the time you are ready, the lending condition has changed.

How to close the gap (My advice)?

Okay, enough reading. It is now high time to learn about solutions. Below, I have shared some field-tested tips that can bring positive results for your startup. Let’s read them:

- Stay application‑ready

Yes, even when you don’t need funding. So, keep your financials updated, your documents organized, and your business story clear.

- Track credit conditions

Don’t focus just on your business. You need to watch rate movements, lending sentiment, and approval trends.

- Pre‑decide your capital use

Don’t wait until your loan is approved to figure out what to do with the money. Have a clear plan in advance. Know exactly where the funds will go, how quickly you will use them, and what success will look like once the money is spent. When you pre‑decide your capital use, it will show lenders that you are prepared, which makes your funding more effective from day one.

- Build a readiness safeguard

Always plan for timing surprises. Expect that you will need funding sooner than you think, and that it might arrive later than you hope. Build your plans to handle both possibilities; so, if money comes early, you are ready to use it, and if it is delayed, your business can keep moving without falling behind. This kind of safeguard keeps you steady no matter how the funding timeline changes.

Finance Ideas TL; DR | Tapos Kumar

- Funding problems are not just about approval

- I noticed that most losses come from timing misalignment.

- Banks and founders operate on completely different timepieces

- I noticed that smart founders manage timing.

- Businesses miss because bank timing ≠ business timing.

Frequently Asked Questions (FAQ) about bank timing vs founder timing?

Why do good businesses miss funding?

This happens because qualification and timing are two separate systems that don’t naturally align.

I found that most founders assume once they qualify, the remaining is procedural. But internally, lenders continue estimating risk until the final stage. In short, credit conditions can change during the process itself. For this reason, even if your business stays the same, the lending environment around your deal changes.

Do this: Your focus should be on timing alignment. So, don’t set approval as the goal. Before applying, ask yourself this = If this arrives 45–60 days late, does my plan work? If you have answered, then okay, otherwise, you are just involved in timing risk.

Do banks change their timing based on the economy?

Yes, constantly, and often without direct communication.

According to supervisory and risk management signals associated with the Office of the Comptroller of the Currency:

- Risk acceptance tightens during uncertainty

- Approval layers increase &

- Decision speed slows

So, if you experienced a delay, that is actually a system-wide caution.

Do this: I suggest tracking timing signals such as interest rate direction, credit tightening sentiment & market volatility.

Is a delay always a bad sign in a startup loan?

No. Delays don’t always mean rejection, but they do mean internal approvals, risk concerns & timing sensitivity have not fully aligned yet.

Do this: Ask yourself: What is causing the slowdown, and whether it will push back your deadlines. This question will help you understand the risks rather than vague reassurance.

Why is timing sometimes more important than interest rates?

This happens because lost opportunities compound faster than higher costs.

Yeah, a slightly higher interest rate is a known cost. But delayed action creates missed revenue, reduced market position & slower growth cycles.

My tips: I recommend you compare the cost of capital & cost of delay. This is because in many cases, faster money > cheaper money.

How early should I apply for funding?

Earlier than your instinct tells you. Most founders apply when they need capital, but by then, there is no margin for delay & no option for process friction.

Do this: Apply this mindset when you have room to make mistakes. That extra time can give you a safeguard to adjust, more options to choose from, and leverage to negotiate. In startup finance, it is about using your early options to stay ahead of risks rather than waiting until you are cornered.

Can strong businesses fail because of timing alone?

Yes. Startups don’t collapse overnight. Instead, they slow down, miss key opportunities, and lose their market position. That is harder to notice and easier to ignore.

My advice: To stay ahead, don’t just track survival or profitability; watch how quickly you are executing and how effectively you are seizing opportunities.

Which types of businesses are most affected by timing issues?

According to my study, businesses are tied to speed, seasonality, or market changes. Timing is more important when inventory cycles are short, demand fluctuates quickly & competitive moves happen fast.

Do this: If your business depends on timing, then take funding as a timing strategy.

Should I wait for better loan terms?

Hmm, only wait if timing allows it.

Founders usually focus on getting lower rates or better deal structures, but they ignore how the opportunity’s value itself declines over time.

Therefore, you should focus on whether waiting improves the outcome or simply delays progress.

My tips: When timing is critical, speed usually beats cost efficiency, because capturing the opportunity while it is valuable is more important than shaving off small expenses.

What is the safest funding strategy in today’s environment?

Timing arrangement combined with parallel execution. Therefore, the biggest risk today isn’t rejection. It is misaligned timing & single dependency.

Do this: Make your plan simple: Think about the right time to act, expect delays, and keep more than one option ready. This will help you move fast when opportunities arise, adjust when things slow down, and never get stuck on a single path.

Tapos’s last thought

Think of startup funding like catching a bus. Getting a ticket, i.e., approval matters, but if the bus has already left, the ticket won’t take you anywhere. Timing is the real ride.

In simple lines = The wrong money at the right time can help. But the right money at the wrong time does not.

Now it is your turn. How was my article? If you can spare a few seconds, tell me your personal experience in the comments. And don’t forget to ask me in the comments if you still have questions. I will try to answer them with bonus tips as soon as possible. Thanks for reading my article.

References & Sources

Below is the lists of sources that I have used to write this article:

Disclaimer

The information provided in this article is author’s view & only for educational purposes. This is not a startups advice. This is not a sponsor post & not an investment advice. Do your research before making any important financial decision. Therefore, Finance Ideas will not be liable for your financial loss.