You are not checking other funding options. You are busy with the next business plan. You are smiling because there is no negative sign for a loan.

Woo! Who know that your ending will be unexpected. Your planning, your dream all just become dead when lender reject your loan application. And, if you ask me what is this situation called, then I will say pre-approval illusion.

So, don’t be frustrated or angry! Be cool & sit with some time. In this article, I will explain everything that your mind asks.

Finance Ideas AI snippet box | Tapos Kumar

What is the pre-approval illusion?

According to me, the pre-approval illusion is a decision trap where early positive signals from lenders create false certainty & ultimately leading businesses to act before approval is secured.

Related Articles

- Loan for start up: Fund Your Dream

-

How US lenders define risk: If Lenders Say You’re “High Risk,” Read This First

-

Why Startup Loan Rejections Feel Vague: And Why Lenders Stay Silent?

-

What lenders see in bank statements: But Never Explain

-

90-day plan after startup loan denial: Here’s the Smarter 90-Day Move

-

Risk memo after loan denial: What lenders document about you?

-

Cash conversion cycle lenders model: Denied Again? Read this

-

Bank portfolio math: Why Perfect Borrowers Hear No

-

Capital preservation bias: What Founders Get Wrong?

-

Founder distribution problem: The Hidden Risk Behind Owner Pay

- Loan approval momentum effect: What Most Founders Miss?

- Bank relationship capital: How Founders Build Banker Trust

-

Interest rates vs risk appetite: The Credit Market Secret Most Founders Miss

-

Industry credit cycles: The Lending Window Most Founders Miss

-

Financial statement stability optics: How Banks Read Your Financials?

-

The internal risk ladder: It is Not What You Think

-

The hidden cost of being almost bankable: Here’s Why You’re Losing Money

-

Credit Fatigue: Lean How to Fix It?

Why do startup loans seem certain before they are?

When you are building a startup, getting a loan or investment feels like oxygen. If someone says, “This looks good” or “We are moving forward”, it is natural to breathe easier.

But risk doesn’t show up when things look shaky. It shows up when things feel certain before they are.

According to me, this is a trap because you are confidence without confirmation. The sad part is; you can’t avoid this trap just by telling yourself to “be careful.” Because while it is happening, it doesn’t feel like a mistake. Instead, it feels like progress. We feel joy for good news & sorrow for bad news. This is human psychology & it is difficult to avoid.

By considering above facts, I have built a 4-stage illusion model that help you to detect early trap. Let’s read them.

Stage 1: Signal detection= This is going well

In this phase, you will experience early positive feedback like: “Looks aligned”, “No major issues,” or “We are moving forward.”

You feel relieved, energized, and validated. But in reality, you are not approved; you have just cleared the first selection.

Say, a bank officer tells you, “Your documents look fine.” You naturally feel like the Loan is almost guaranteed. But in practice, they have only checked the basics.

My tips: Consider banking signals like “This is going well” to “I am in the assessment process. yet”

Stage 2: Confidence inflation = This will go through

Your loan application status doesn’t change, but your mind is asking different things. In this startup phase, you should consider what happens if your loan is rejected. Instead, your mind influences you for this. When this goes through, type something.

Now you could ask me why this happened? Look, I am not a psychologist, but I will tell you the reason from my personal experience. In my view, this happens because humans crave closure. Early good news tricks us into thinking it is already settled.

And, the outcome? You replace probability with belief & belief drives action faster than logic.

My tips: I suggest you use a probability anchor rule. How? Instead of “This is happening,” say “This is 60% likely.” That keeps your decisions logical & changeable.

Stage 3: Strategic change =Let’s move ahead

In this stage, your behavior will change. You start slowing down other funding options, planning hires or expansion & mentally spending money you don’t have yet.

How can it be a risk for your business? You are making startup moves based on something that isn’t final.

My tip: Set this commitment in your mind: Until approval is final, no irreversible decisions like hiring, contracts, or big purchases.

Stage 4: Late collapse = We are unable to proceed

Sometimes the deal falls apart at the last minute. So, naturally, you feel surprise, frustration, and confusion. This happens because everything felt certain & it is not your fault.

Say, the bank declines after a deeper review, but you have already signed a lease for a bigger office. The bank rejected you because, at the last minute, they revealed new risks. So, rejection is not damaging your business; it is you who made business decisions before funding approval.

My tips: I suggest you reassess all assumptions, reopen other funding paths & re-align plans with actual money.

When does almost approving become costly (I have conducted a case study)?

Emma runs a small e-commerce startup. She applied for a $150,000 loan to expand her operations. After the first meeting, the loan officer told her: “Your application looks strong & there are no major issues.”

Stage 1: Signal detection

Emma felt relieved. She thought, “This is going well.” But in reality, she had only cleared the initial paperwork check.

Stage 2: Confidence inflation

Encouraged by the positive feedback, Emma started telling her team, “Once the loan comes in, we will hire two more people.” She stopped exploring other funding options because she believed this Loan was practically guaranteed.

Stage 3: Strategic change

Emma signed a lease for a bigger warehouse, assuming the Loan would close soon. She also placed a large inventory order, thinking she would have the cash to cover it.

Stage 4: Late collapse

Two weeks later, the bank called: “We are unable to proceed. After a deeper review, your revenue history doesn’t meet our lending criteria.

Emma was shocked. She had already committed to expenses she couldn’t afford. However, rejection didn’t damage her business; instead, it was the decisions she had made before the Loan was finalized.

Lessons from this case study:

- Don’t consider early good news as a guarantee of funding.

- Keep backup funding options alive.

- Delay big commitments until the money is approved.

How do founders avoid costly mistakes?

Okay, got it. Now, tell me what I should do. Your mind may ask such questions & this is good that you are thinking the correct way.

Starting a business is exciting, but making better money decisions is difficult. I witnessed that many US founders failed not because of a wrong move, but because they made the right decisions too early.

Below, I have shared some common problems (mostly arising under the current US economy) from my personal experience, along with their proper solutions. I hope you find them effective. If you have any further queries or opinions, you are welcome to leave them in the comments. I think it would be a learning conversation.

Let’s read them:

Problem-1 = I will just be more careful, doesn’t work

My solution: Consider timing as a system

I noticed that most of the American founders think, “Next time I will be more cautious.” But caution alone doesn’t solve the problem. This isn’t about awareness; it is about decision timing under uncertainty.

Think of timing like traffic lights. You don’t cross the street because you feel it is safe; you cross when the light turns green. Equally, business decisions need the same kind of system.

Problem-2 =Confusing positive signals with certainty

My solution: Separate signal from approval

You hear encouraging lines from an investor or lender like “This looks promising,” and assume it is a done deal. You shouldn’t think it this way. Instead, before assuming, ask yourself: Has this been officially approved, or is it just a positive signal?

So, when a bank says, “Your loan looks good,” that is a signal.

And, if they send you a signed approval letter, that is certain.

The moral is: if it is not documented, don’t depend on it.

Problem -3 = Acting too early with irreversible moves

My solution: Create a “No-regret zone.”

As a founder, you hire staff, sign contracts, or order inventory before funding is confirmed. Don’t do that. Don’t make commitments you can’t undo until money is guaranteed. Why am I suggesting this?

Say you hire three employees because you expect a loan to close. If the Loan falls through, you are stuck with payroll you can’t afford. Therefore, you should have a reverse option if funding doesn’t come.

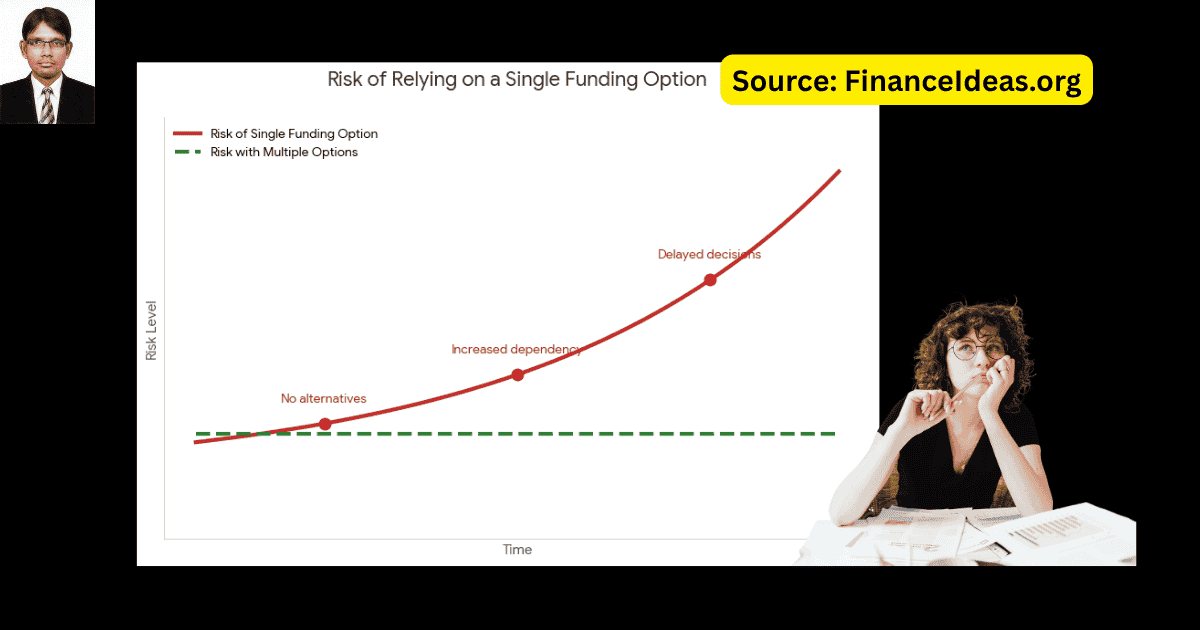

Problem -3 = Putting all your eggs in one basket

My solution: Run parallel paths

I saw that when one deal looks strong, founders don’t explore other options. This is not a worthwhile business move. Instead, you should keep a conversation open with an angel investor if you are waiting on a bank loan. I am suggesting this because you will not be stuck if the bank delays.

Problem- 4 = Trusting belief instead of probability

My solution: Feelings don’t work, so assign numbers.

Saying “This will go through” makes you act too soon & this is a trap. So, replace belief with probability. Don’t be bullish that “This will happen”; instead, take it like this: “This has a more than 50% chance with less than 40% risk.”

So, before signing a lease, I suggest you write down the following:

Best case: Loan approved; you expand.

Worst case: loan denied; you are stuck with rent.

Probability = +50% approval, -40% denial.

This keeps you changeable and prevents overcommitting.

Download Free Pdfs resources without E-mail

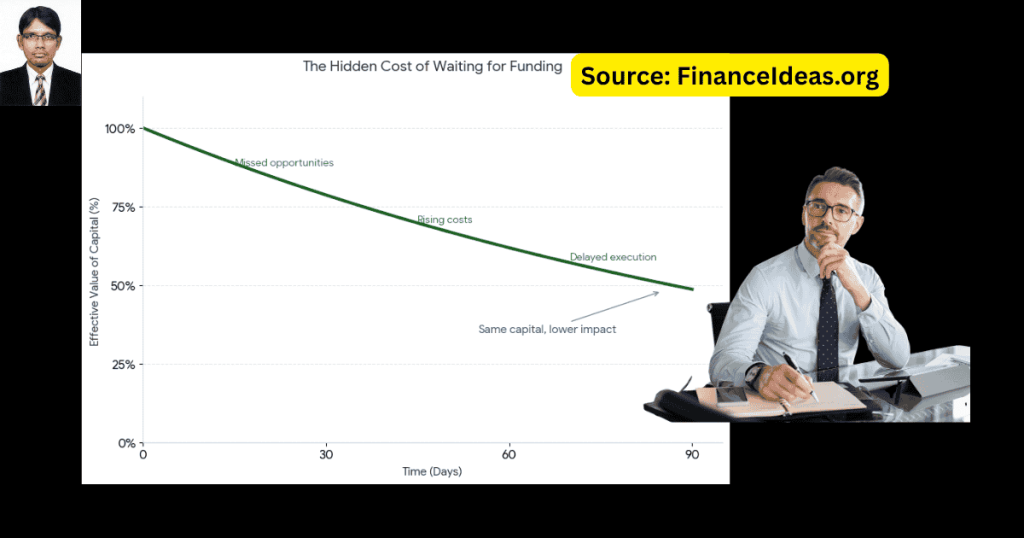

- A practical way to understand what funding delays are really costing you

- How to understand lender language without turning it into false confidence

- Why do founders make expensive decisions before approval, and how to stop it

Finance Ideas TLDR | Tapos Kumar

- Early signals are not approval

- Confidence appears before certainty

- I found that most business damage happens before rejection

- I recommend that you make decisions.

Frequently asked Questions (FAQ) about the pre-approval illusion?

What does final review mean in real terms?

It means the deal is under its most critical scrutiny. That means, it is not almost approved.

At this stage, lenders check cash flow assumptions, risk level & internal arrangement across decision-makers. Here, banks either fully qualify or stop the approval process.

Do this: I suggest that you pause all irreversible actions. Use this stage to prepare alternative financing options.

Can I rely on conditional approval?

Hmm, only partially because it signals direction, & don’t give certainty. Conditions are not formalities; they are checks. If any condition fails under deeper review, the entire approval can change.

My tips: Make a backup plan for this. If these specific conditions are not met, I have an option to accomplish the business goal.

Why do lenders seem confident but decline later?

This happens because communication shows progress in evaluation. Banks don’t commit to approve a loan. This is not my personal opinion. The Consumer Financial Protection Bureau also said the same things. According to them, financial commitments only come when terms are explicitly defined.

My tip: I suggest you make business decisions based on documents.

Should I start planning once things look good?

Hmm, you can plan, but you should not commit.

Planning will not damage your business, but it can lead to early commitments, such as hiring based on expectations, budget allocation before confirmation & timeline closure.

Do this: Mentally prepare for two approaches: for soft planning = allowed

And, for hard commitments = delayed

Can lenders change decisions at the last moment?

Yes, they can.

The last stage assessment includes an updated financial explanation, the internal risk position & external economic considerations. In short, Banks make decisions based on total risks. The Federal Deposit Insurance Corporation also suggests similar things. They mentioned that final decisions depend on cumulative risk. So, early-stage signals don’t guarantee loan approval.

How do I stop myself from becoming overconfident too early?

I suggest you separate information from action. It will help you make the right business decision in a timely manner.

My tips: Prepare your mind in this way: No business expansion decision without funding approval.

Is it normal for deals to collapse late?

Yes. Actually, banks do it when they find you are risky or don’t match their requirements. That means early positive signals don’t guarantee funding.

My tips: You should prepare for late-stage uncertainty so that you can save your business.

Tapos’s last thought

You should make business decisions based on the funds you have available. This is because businesses operate under certain conditions; if you make financial decisions such as opening a new branch, it can backfire if funding is delayed or not received.

Additionally, it can create a negative reputation for your business, damaging your market position. So, control your emotions and make decisions according to available capital.

Hey! Did you find my article helpful? And, have you read other articles about startup loan. You will find them in the above, below AI snippet box. Read them first, it will give you a strong foundation. Remember that investing yourself is the first move of a founder & that comes from learning.

References & Sources

Below is the lists of sources that I have used to write this article:

Disclaimer

The information provided in this article is author’s view & only for educational purposes. This is not a startups advice. This is not a sponsor post & not an investment advice. Do your research before making any important financial decision. Therefore, Finance Ideas will not be liable for your financial loss.