I was tracking Hut 8’s quarterly earnings, one of North America’s largest Bitcoin miners. At the time, they were burning megawatts of electricity, stacking Bitcoin, waiting for the next halving moonshot.

Then, first came small mentions of “diversification into HPC.” Then “high-performance computing partnerships.” Then the name changes, i.e., Hive Blockchain dropping “Blockchain” completely. Bitfarms is becoming Keel Infrastructure. And suddenly it clicked: these companies were not only diversifying but also transforming.

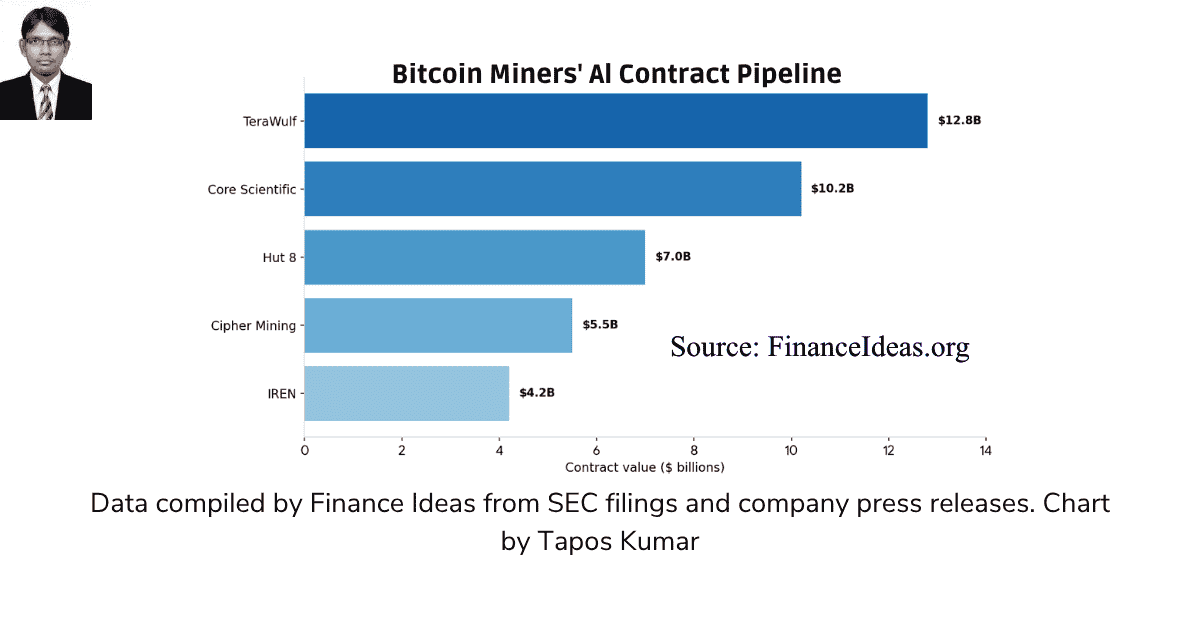

According to Finance Ideas, across the board, publicly listed miners have now signed more than $70 billion in AI and high-performance computing contracts. This figure exceeds the market caps of most major mining firms.

In my opinion, by the end of 2026, companies you know as Bitcoin miners will get more than 70% of their revenue from AI. Are you interested in learning how? Just continue reading.

Finance Ideas AI snippet box | Tapos Kumar

What are Bitcoin miners doing with AI?

According to my study, Bitcoin miners have turned to AI cloud computing to survive collapsing mining margins. Publicly traded miners have signed over $70 billion in AI and high‑performance computing contracts with companies like CoreWeave, Google, and Microsoft.

Let me share some facts:

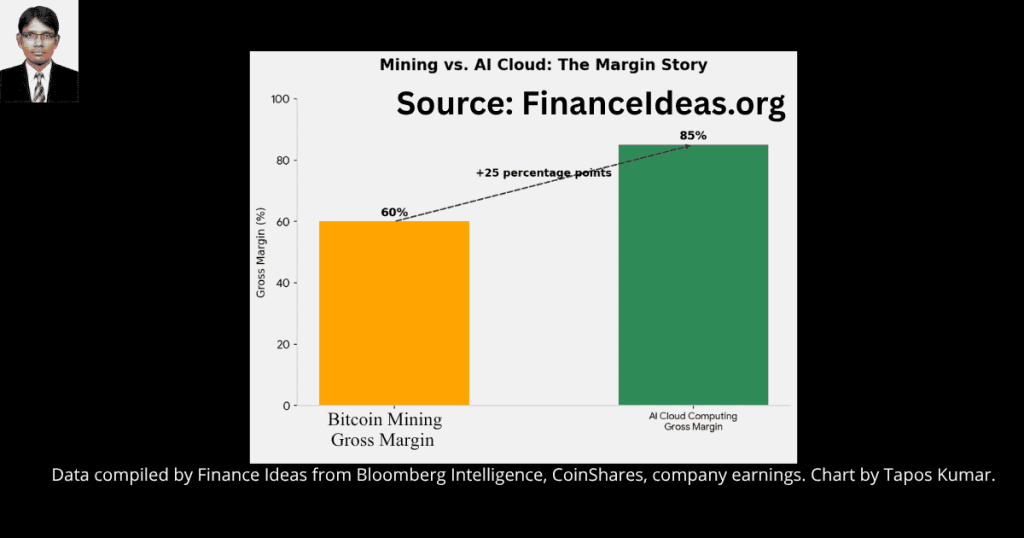

- Mining margins have dropped to about 60%, while AI cloud margins are in the mid‑80s.

- Hut 8 built modular “LEGO block” data centers that can switch power between Bitcoin mining and AI training.

- Cango launched EcoHash, a subsidiary dedicated to AI inference.

- Core Scientific signed a $10.2 billion, 12‑year AI lease with CoreWeave.

Related Articles

-

Bitcoin vs M2: Why the Old Liquidity Model Died (2026 Data)

- How high will Bitcoin go: Trump’s Secret Plan Revealed (2026 Update)

I found a crisis for BTC mining stocks?

Okay, let me share some facts. The weighted-average cash cost to mine one Bitcoin reached nearly $80,000 in Q4 2025, meaning that at today’s price of around $74,000, most large-scale miners are losing roughly $6,000 per coin they produce.

This is not only my analysis. CoinShares described Q4 2025 as “one of the most challenging periods for miners since the last halving,” citing both price pressure and record network difficulty.

The network hash price (a key measure of mining revenue) collapsed from roughly $36–38 per PH/s per day in Q4 2025 to around $29 in early 2026. For miners running current-generation hardware, you need electricity at $0.05 per kilowatt-hour or less just to break even.

Hashrate, the total computing power securing the Bitcoin network, has dropped roughly 14.5% from its October 2025 peak. Three consecutive negative difficulty adjustments (a pattern not seen since July 2022) suggest that some miners have simply unplugged their machines.

So, these are not simple business expansions into exciting new markets. They are survival moves by companies bleeding real money every single day.

Precisely how widespread is this exit? Large miners, including MARA Holdings, sold roughly $1.1 billion worth of Bitcoin in recent weeks (over 15,000 coins), partly to fund AI infrastructure. Bitfarms changed its entire corporate identity to Keel Infrastructure. Cipher sold off mining assets to focus on AI data center operations.

Mining gross margins have collapsed from above 90% during the 2021 bull run to roughly 60% today. AI cloud operations, in contrast, generate margins in the mid-80s. Electricity now consumes roughly 40% of mining revenue, pushing total costs into the low-to-mid 90% range. For AI cloud operators leasing high-powered chips, that figure is in the low single digits.

Based on the above facts, I want to say that transitioning to AI is not optional; instead, it is the only way to survive.

Hut 8‘s “LEGO Block” model?

In a March 2026 Benchmark-hosted fireside chat, CFO Sean Glennan described the company’s modular infrastructure approach as a “LEGO block‑type” model; facilities built with interchangeable components that can adapt among Bitcoin mining, AI training, and high‑performance computing depending on which yields the strongest returns.

Glennan outlined the strategy this way: power allocation drives returns, & not crypto price speculation. “The electron is a critical, scarce asset,” he said, emphasizing that Hut 8 wants to direct electricity toward whichever workload offers the best economics at any given moment.

The company’s Vega facility in Texas, initially built exclusively for Bitcoin mining, now supports AI workloads. Hut 8 signed a $7 billion, 15‑year AI infrastructure lease and is bringing massive capacity online at its River Bend site.

Benchmark has maintained a “buy” rating and a $85 price target on Hut 8 stock, specifically citing the River Bend lease and the modular infrastructure strategy as key drivers.

Management avoids building speculative capacity. Instead, the firm secures demand, financing, and power access before committing capital. The development pipeline spans roughly 10 gigawatts at various stages.

This case study suggests the following roadmap: build flexible power assets first, then decide which compute workloads to run. Hut 8 is positioning itself less as a miner and more as an energy infrastructure operator that happens to do some Bitcoin mining on the side.

EcoHash = Cango‘s AI inference play (I was just surprised by the facts)?

You may not have heard of Cango. The company previously operated a Chinese car‑loan financing business. In April 2025, it sold that business for roughly $352 million and turned entirely to Bitcoin mining. On April 13, 2026, just last week, Cango announced the launch of EcoHash Technology LLC, a subsidiary dedicated solely to high-performance computing and AI inference.

EcoHash officially began commercial operations on April 13, leveraging Cango‘s global energy footprint (sites in Oman, East Africa, Paraguay, Canada, and the US) to deploy standardized, plug‑and‑play compute modules paired with a proprietary orchestration platform called EcoLink.

Cango is dedicating space at its 50MW mining facility in Georgia as a “living showroom” for these modules. The company plans to replicate this model in Japan, California, Texas, and Tennessee.

Goldman Sachs Research warns that US data center power demand could reach 700 terawatt‑hours by 2030, largely driven by AI inference workloads, while the maximum available supply remains just above 300 TWh, hmm, a structural gap of roughly 400 TWh.

EcoHash‘s CTO, Jack Jin, said it in a better way: “Our proprietary orchestration layer, the central nervous system of our network, is built to enable intelligent, real-time resource allocation. This connects decentralized energy assets directly to the demands of LLM inference, generative AI, and a growing spectrum of compute‑intensive applications”.

What have I found from this case study? I don’t find this to be speculation. It is live infrastructure, in production, serving paying AI customers today. Cango understands that AI compute is the product & mining is the backup.

The $70 billion elephant in the room (Yes, true)

Publicly listed miners have announced more than $70 billion in AI‑ and HPC‑related contracts. Don’t trust me? Let me share some data that I have collected via a survey:

| Company | Notable AI/HPC Deal | Value (about) |

| Core Scientific | 12‑year agreement with CoreWeave | $10.2 billion |

| TeraWulf | Secured HPC revenue contracts | $12.8 billion |

| Hut 8 | 15‑year AI infrastructure lease | $7 billion |

| Total across public miners | Various announced contracts | $70+ billion |

The interesting part is = These contracts are not one‑off experiments. They are 10‑ to 15‑year deals with some of the largest hyperscale tech companies, including Google, Microsoft, and Anthropic. And they offer long-term revenue visibility, stable cash flows, and predictable margins for BTC mining.

And, the market has already started rewarding this divergence. Miners with secured AI contracts trade at roughly 12.3x 12‑month sales. And, pure‑play Bitcoin miners? 5.9x, i.e., less than half. Investors are paying double for AI risk, which creates a self‑reinforcing cycle. Higher valuations make it easier to raise debt and equity. Raising capital funds for more AI infrastructure attracts more contracts.

So, this is a flywheel & it will only accelerate.

The 4-year Bitcoin cycle is dead now (we need to look beyond mining)?

The Bitcoin halving cycle has dictated miner behavior for over a decade. Every four years, block rewards are halved, increasing production costs, driving inefficient miners out, and ultimately forcing the price higher to restore equilibrium.

That cycle is breaking. Yes, this is true & let me tell you why. This is true because miners are no longer purely miners. A company with a 12‑year AI contract worth $10 billion doesn’t need to hold Bitcoin reserves to survive the next halving. It does not need to sell coins at the bottom to cover operational expenses. It has predictable, dollar‑denominated revenue streams that are completely uncorrelated from crypto markets.

This is not my personal view; CoinShares also found similar things. CoinShares projects that by the end of 2026, some firms will derive as much as 70% of revenue from AI.

This changes the fundamental economic model that has underpinned the Bitcoin network for 15 years. For the first time, large portions of hashpower are becoming economically decoupled from Bitcoin‘s price. For these reasons, the question now is: what happens when 70% of a miner’s revenue comes from a source that has nothing to do with Bitcoin?

I do not yet have a perfect answer. If you have, share it in the comments. I want to know.

But I suspect the old halving‑driven price models are about to look very outdated. Wall Street is already beginning to value these firms as AI infrastructure companies with optional Bitcoin risk.

For investors, that means the valuation multiples could expand significantly if the transition proceeds efficiently. But it also means that, for the first time, a major Bitcoin price crash may not force a miner exodus, because miners will have other revenue streams to lean on.

How will the government respond to this change? US energy regulators are paying close attention. The Department of Energy has pushed the Federal Energy Regulatory Commission to write new rules for connecting large electricity consumers (AI data centers and crypto miners alike) directly to the power grid, with a completion target of April 30, 2026. Many large mining operations are positioning themselves as flexible grid resources, i.e., scaling back during peak demand to stabilize electricity markets, which is precisely the kind of demand response utility operators value.

At the same time, policymakers are awakening to the national security implications. President Biden’s January 2025 executive order on AI infrastructure directed the Defense and Energy Departments to lease federal lands for AI data centers, explicitly requiring that the facilities use “appropriate portions” of US‑made semiconductors. The order aimed to begin construction by January 2026 and reach full‑capacity operation by December 2027. Combined with ongoing regulatory pressure from the Office of the Comptroller of the Currency and growing DOE involvement in grid planning, this signals that Washington sees mining‑adjacent compute infrastructure as a strategic asset.

What should I do as a Crypto investor?

I have been getting this question a lot via Threads. Bitcoin miners ask me what they should do now for this transition. I conducted a market analysis using historical performance data. Now I will give you some tips based on findings.

First, look at miner stocks differently. Keep in mind that not all mining stocks are equal. You need to separate pure mining plays from firms that have successfully turned to hybrid or AI-first models. Several early movers have climbed to record highs, including TeraWulf, IREN, Cipher, and Hut 8. The market is already rewarding those with signed, long‑term AI contracts that offer multi‑year revenue visibility. Miner stocks can be extremely volatile, though, and past performance doesn’t guarantee future results.

Second, understand that Bitcoin network security may change. As mining operations become more dependent on AI revenue, the incentives that secure the Bitcoin network could change fundamentally. This is not inherently bad; a more economically diversified mining base might be more durable. But it is something anyone with significant Bitcoin holdings should monitor carefully. The hash rate has already declined by about 14.5% from its peak, and while Bitcoin’s difficulty adjustment mechanism will eventually rebalance, the path to equilibrium is uncertain.

Third, consider the asymmetric opportunity. Because the market broadly values these companies as miners rather than AI infrastructure providers, there may be a valuation gap. Investors are paying roughly double for AI risk, which further reinforces the incentive to complete the transition. If the transition accelerates, the multiple expansion could be significant. But if it stalls, AI-focused valuations could compress sharply.

Fourth, remember that the mining (energy) connection remains real. Even for miners heavily transitioning to AI, electricity costs are the single most important variable. US regulators are moving to streamline grid access, which could lower power costs for US-based miners relative to international competitors. Pay attention to which miners have locked in low‑cost, long‑term power purchase agreements. They will have the largest margins, whether they mine Bitcoin or rent AI compute.

Finance Ideas TL; DR | Tapos Kumar

Our study found that Bitcoin miners have signed over $70B in AI/HPC contracts in secret. By the end of 2026, some will get 70% of revenue from AI & this is not from mining. AI margins run in the mid-80s, while mining margins have collapsed to roughly 60%. Hut 8 built modular “LEGO block” data centers to switch power between AI and mining. Cango just launched EcoHash for AI inference. The companies you call “miners” are becoming the backbone of America‘s AI infrastructure, and Wall Street is paying double for the stock of those that complete the transition.

Download free Pdfs without E-mail

- Miner to AI Transition Primer-Tapos Kumar

- AI Mining Stock Screener-Tapos Kumar

- Mining AI Data Pack-Tapos Kumar

Frequently Asked Questions (FAQ) about Bitcoin miners AI compute providers?

Why are Bitcoin miners suddenly interested in AI?

BTC miners are suddenly interested in AI because mining alone is barely profitable right now. The average cost to mine one Bitcoin is about $80,000, which is higher than the current price of $74,000. As a result, miners were losing money on every coin they mined. On the other hand, AI cloud computing offers margins of 80%+ and long‑term contracts.

What does a modular LEGO block data center mean?

Hut 8 popularized the modular LEGO block. Think of a data center built with interchangeable containers. Each container can hold Bitcoin mining rigs, AI servers, or high‑performance computing nodes. If crypto prices crash, you swap mining containers for AI containers, without shutting down the whole facility. It is like changing a lightbulb instead of rewiring the house.

How much money have miners made from AI so far?

According to my analysis, it is over $70 billion in signed contracts, but most of that revenue will be recognized over 10‑15 years. So, the immediate cash flow is smaller. However, the valuation multiples have already doubled for miners with AI contracts.

Will Bitcoin mining stop if miners move to AI?

No, but some miners may reduce their hash rate. The network has already seen a 14.5% drop from its peak. But Bitcoin’s difficulty adjustment will eventually balance things out. Less efficient miners will drop out, and the remaining ones will profit. The move to AI is mainly for publicly traded miners with large capital bases. Smaller miners will keep mining.

Can any Bitcoin miner switch to AI overnight?

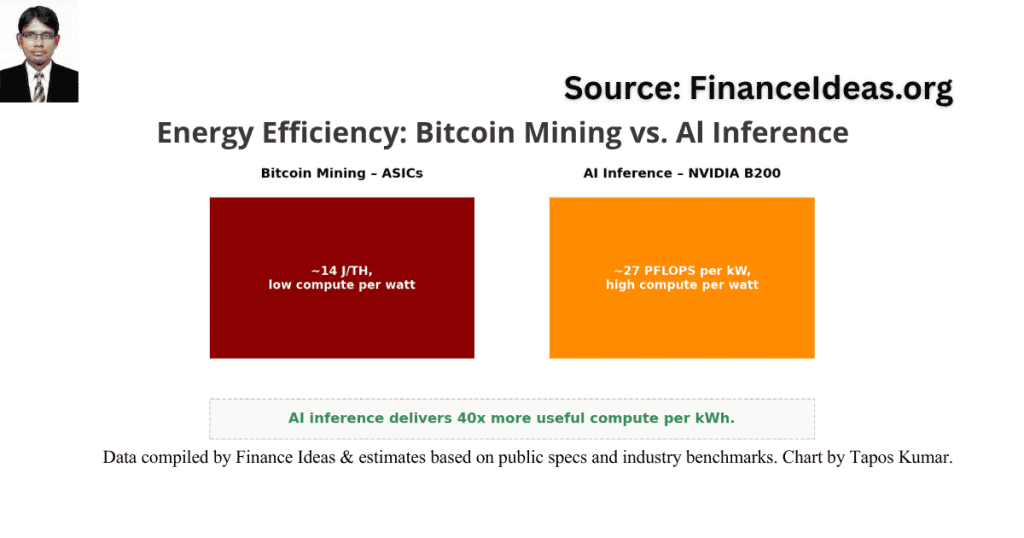

No. Let me tell you why. You need three things: high‑bandwidth fiber, liquid cooling (not just fans), and NVIDIA H100 or B200 chips (not ASICs). Most mining rigs use ASICs that can’t run AI models. Switching requires capital investment, hmm, often $500 million or more per facility. For this reason, only the major miners are making the move.

What happens to the Bitcoin halving cycle when miners have AI revenue?

You just asked a billion‑dollar question. Historically, halving events forced miners to sell coins to cover costs. If miners get 70% of revenue from AI, they don’t need to sell Bitcoin. That could reduce sell pressure after future halvings, potentially making Bitcoin less volatile but also changing the four‑year cycle that traders rely on.

What risks am I not hearing about Bitcoin mining?

According to my analysis, three big risks:

Dilution = Miners are issuing new stock and convertible debt to fund AI builds. So, your ownership percentage can be reduced.

Execution risk = Building AI data centers is hard. So, delays, cost overruns, and chip shortages are all possible.

Competition = Amazon, Google, and Microsoft are also building data centers. They have deeper pockets. Miners win on speed (existing sites) but not on scale.

Could Bitcoin mining become secondary to AI for these companies?

Yes, and for some it already is. Cango launched EcoHash as a separate subsidiary dedicated 100% to AI inference. Hut 8’s CFO said they want to be an “energy infrastructure operator” first, miner second. The naming changes (Hive dropping “Blockchain”, Bitfarms becoming Keel) are not cosmetic. They signal a fundamental identity change.

How does an ordinary crypto investor play this trend?

Hmm, two ways you can play:

Buy the stocks = TeraWulf, Hut 8, IREN, Core Scientific (but know the risks).

Buy Bitcoin itself = If miners hold more AI revenue, they may sell fewer coins, reducing sell pressure. That is indirectly bullish for the Bitcoin price.

Avoid = Miners with no AI contracts and high debt. They are the most likely to go bankrupt in a prolonged bear market.

What is one metric to track that no expert talks about?

According to me, the ratio of AI contract value to market capitalization. If a miner has a $7 billion AI lease (like Hut 8) but a market cap of only $2 billion, the market is pricing in zero success. That is either a huge opportunity or a huge red flag. So, compare the ratio across miners; the ones with the lowest ratio are either undervalued or about to fail.

Will this AI change make Bitcoin less decentralized?

Hmm, potentially. If most mining hashpower ends up controlled by a handful of publicly traded companies with AI contracts, that centralizes influence over the network. However, the same companies also have fiduciary duties to shareholders that are not aligned with Bitcoin’s ideals. This is an active debate among core developers. So, no direct answer yet.

What is the single main misconception about this trend?

According to my analysis, the main misconception is that miners are abandoning Bitcoin, but they are not. They are diversifying because Bitcoin mining alone is becoming unprofitable. The AI revenue lets them hold more Bitcoin rather than sell it to pay electricity bills. In the long run, this could make the Bitcoin network healthier, even if the miners themselves don’t look like miners.

Tapos’s last thought

I want to close my article with the following advice:

- First, audit your risk. If you own miner stocks or funds, pull the latest quarterly MD&A. Look for the term “HPC” or “AI inference.” Companies with multi‑year AI contracts are in a different risk category than those whose revenue is primarily mining-driven.

- Watch the early movers. Use TeraWulf, IREN, Cipher, and Hut 8 as bellwethers. Track their hash rate and their AI contract pipeline simultaneously. The ratio of those two numbers will tell you how far along each company is on the transition path.

- Monitor the regulatory pipeline. The DOE‘s April 30, 2026, FERC deadline is important. If grid access becomes quicker and cheaper, US miner margins expand across the board, i.e., for both mining and AI operations.

- Don’t forget the miners ‘balance sheets. The companies that are making this transition are funding it by selling Bitcoin reserves or issuing convertible debt. Therefore, dilution is important. So does the liquidation of Bitcoin treasuries. Read beyond the revenue headlines to understand each miner’s capital structure.

Many of you just read my article. Please share it with others & also leave comments if you can spare a few seconds. This will inspire me to write the next helpful article for you.

References & Sources

Below is the lists of sources that I have used to write this article:

- Goldman Sachs

- CFTC Announces Historic MOU with SEC for Crypto Asset Harmonization

- White House Executive Order

Disclaimer

This is not a Sponsored post & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not crypto investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, Finance Ideas will not be liable for this.