Today, I will share an interesting chat. Last week, I was in an inbox chat on Threads with a NYC-based ex-hedge-fund professional.

He said that everyone is blaming the Fed, but Bitcoin isn’t moving. Why? I replied that Fed isn’t holding Bitcoin back. Yeah, BTC isn’t moving up, but this occurs for a different reason. He replied angrily, saying, “What is something that you know but I don’t know?” instead of being hedge fund folks.

I cooled him down & said that the man who figured it out first is Arthur Hayes, the BitMEX co-founder who called the 2021 top, the 2022 bottom, and now this: AI deflation is the single major threat to Bitcoin’s price in 2026.

Finance Ideas AI snippet box | Tapos Kumar

Hayes thesis in simple language?

For years, everyone thought Bitcoin‘s major risk was the Fed raising rates. Hayes says that is wrong. According to him, the actual risk is that AI will take white‑collar jobs (engineers, accountants, lawyers, marketers) faster than the economy can absorb them.

Let me share the chain reaction that Hayes predicts:

- AI replaces knowledge workers. Companies realize that one AI agent can do the work of five junior employees.

- Those workers lose $85,000–$90,000 salaries and drop to $28,000 in unemployment benefits. That is a 67% pay cut overnight.

- They cannot pay their credit cards, car loans, or mortgages. So, defaults spike.

- Banks get crushed. Hayes estimates banks could face up to $527 billion in loan losses.

- The Fed has no choice but to print trillions to bail out the banking system.

- Bitcoin explodes, but only after the crash.

“Bitcoin could fall below $60,000 if an AI‑driven credit shock causes a liquidity crisis,” Hayes warned in his April 2026 essay.

That is not a prediction, I think. That is a roadmap. And we are already on it.

Related Articles

-

Bitcoin vs M2: Why the Old Liquidity Model Died (2026 Data)

- How high will Bitcoin go: Trump’s Secret Plan Revealed (2026 Update)

Why do I think AI is different this time?

In the American mainstream media, even in popular podcasts, you see experts discussing the agentic threat to jobs. Their headlines usually say this: “AI will take your job.” I know what you were feeling at that time, so I don’t need any explanation.

Now the question is, what is Agentic AI? Agentic AI is a reasoning model capable of performing complex tasks autonomously.

So, the company can adopt automation for complex tasks. The surprising fact is that this is happening in America now. Now companies are replacing knowledge workers with Agentic AI, & surprisingly, this is not impacting factory workers so much. Hayes calls it a “deflationary bomb ticking below the surface”.

The anecdote that made Hayes stop trading?

In his April 16 essay, Hayes shared a story that shook him. A crypto‑gaming entrepreneur automated his entire engineering workflow using nothing but Claude AI agents. One engineer shipped a product in four days that was expected to take six months. The result? Half the company’s staff will be let go within the next few weeks.

This isn’t a one‑off; instead, it is happening everywhere.

The raw numbers about automation for Agentic AI (2025–2026)?

Are you doubting me? Look, I don’t spread hype information. I write neutrally after analyzing facts. Therefore, I will share some data that I have collected from credible sources so that I can prove my view:

| Metric | Value (about) | Source |

| AI‑linked tech layoffs worldwide (2025) | 70,000 | LinkedIn analysis |

| AI‑cited layoffs in the US (2025) | 55,000 | Challenger, Gray & Christmas |

| AI‑cited layoffs in the US (2026, year‑to‑date) | 54,836 | Challenger, Gray & Christmas |

| Tech jobs lost in March 2026 alone | 15,000 | US Department of Labor / BLS |

| Companies planning to replace workers with AI (2026) | 40% | Challenger survey |

| AI‑exposed US jobs (1.43B weighted exposure score of 4.9) | 143 million | MIT AI Exposure Index |

The scary part I have discovered from these data is this: this is just the beginning & more automation is imminent. I am just reading the World Economic Forum’s prediction. According to the World Economic Forum, about 92 million displaced people are expected by 2030, a figure issued before the 2026 acceleration. Now tell me, do you trust me? If no, then say why in the comment box.

The income cliff?

This is the moment Hayes gets very direct. According to Finance Ideas, the median US knowledge worker earns between $84,000 and $91,000 annually. If they lose their job and file for unemployment, their income drops to around $27,000 per year.

That is a $57,000–$62,000 hole in their household budget. They will not stop spending; instead, they lean into consumer credit, such as credit cards, personal loans, HELOCs, etc.

Then they default, and that is when the banking system breaks.

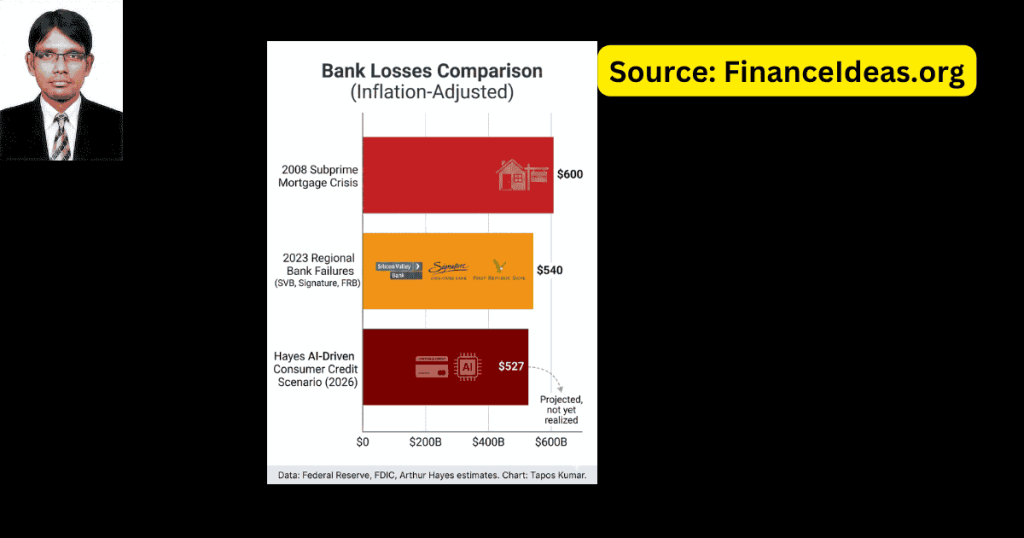

Banking system under siege & this is a $527 billion question?

Hayes draws a direct line from AI job losses to bank failures. And he is not alone.

Goldman Sachs has raised concerns about AI-driven job displacement, noting that displaced workers face reduced earnings and slower career growth for years after losing their jobs.

Then, Federal Reserve Governor Michael Barr broke tradition on February 17, 2026, warning that rapid AI diffusion could permanently lift the natural unemployment rate. “AI could cause long‑lasting dislocation of workers, implying higher unemployment even in a healthy economy,” Barr said.

Hayes‘s estimate: Banks could face up to $527 billion in losses from consumer loan defaults caused by AI displacement.

To put that in perspective:

| Crisis | Bank Losses -About (Inflation‑Adjusted) |

| 2008 Subprime Mortgage Crisis | ~$500‑700 billion |

| 2023 Regional Bank Failures (SVB, Signature, First Republic) | ~$540 billion |

| Hayes’s AI‑Driven Consumer Credit Scenario | ~$527 billion |

Hayes warns that this scenario could mirror the regional bank failures seen in early 2023, but on a larger scale, driven by the perceived inevitability of AI-driven disruption.

In my opinion, unlike 2008, when losses were concentrated in mortgage‑backed securities, AI-driven defaults would hit unsecured consumer credit: credit cards, personal loans, and auto loans. Those are held directly on bank balance sheets, not sliced and sold to investors. When those defaults spike, banks eat the loss immediately. There would be no bailout from bondholders & no time to prepare.

That is why Hayes calls it “game over for the fugazi fiat fractionalized banking system.”

The Fed’s inevitable response & when the printer turns on?

This is the phase where I found Hayes’s framework turns bullish, but not yet. Let me explain why.

The Fed hates deflation more than inflation. Why? Because deflation makes debt more expensive in real terms. A $500,000 mortgage doesn’t shrink when prices fall. Your income does. That is how depression starts.

So, when consumer defaults spike and banks start failing, the Fed will have no choice but to print money, hmm, massive, unprecedented amounts of it.

Hayes calls Bitcoin a “liquidity alarm” for this exact reason. In a March 2026 podcast, he explained: “Bitcoin ‘s performance tells us there isn’t enough dollar liquidity in the market right now. That is why it has been underperforming for 6 to 9 months”.

His prediction: Bitcoin could trade between $80,000 and $100,000 while markets debate the Fed’s next move, but he sees a rally to $124,000 and, shortly after that, to $200,000 once money printing begins in earnest.

He has also reiterated his $250,000 Bitcoin target for 2026 and projected $500,000 to $750,000 by the end of 2027.

But Hayes is not buying yet. His fund, Maelstrom, did “fuck all trading in the first quarter” of 2026. His response when brokers ask what he wants? “It is a no‑trade zone”.

He won’t deploy new capital until the Fed injects liquidity &, not talks about it, not signals it, but does it.

What does this mean in my opinion? The Fed will print. But not yet. And until then, Bitcoin is stuck in a range, or worse, heading lower.

I built a roadmap to the bottom based on Hayes?

I just took Hayes‘s three scenarios from his April 2026 essay & also added my prediction. Let’s read them:

Scenario one = War ends, AI continues.

If the Iran war ends immediately, Bitcoin might bounce to $80,000–$90,000, Hayes says. But the “AI agentic deflation bomb yet ticks below the surface.” Until the Fed provides liquidity to plug the hole in banks’ balance sheets, Bitcoin will not meaningfully rise.

My position: This is the most likely short‑term path. A relief rally to $80‑85k, followed by renewed downside as AI layoffs accelerate.

Scenario two = Iran controls the Strait.

If Iran successfully restricts shipping and collects tolls in yuan or Bitcoin, countries will sell dollar assets to raise yuan. This could cause a sell‑off in treasuries and stocks. “Bitcoin will struggle to rally meaningfully,” Hayes warns. Only when things get bad enough will Bitcoin rise as expectations of a bailout become consensus.

My position: This is the chaos scenario. Bitcoin drops first, possibly below $60k, then explodes once the Fed panics.

Scenario three = Full‑scale war

If the US destroys Iran‘s ability to interdict shipping, Hayes warns Iran will take the Gulf’s energy production down with it. Commodity prices spike. Central banks print to subsidize food and energy. Bitcoin rallies, but at great cost, including the prospect of WWIII.

My position: This is the black‑swan scenario. Bitcoin moons, but everything else burns. Yeah, not a comfortable trade.

When AI deflation becomes Bitcoin‘s best Friend?

Yes, AI deflation crashes Bitcoin first. But then it becomes the biggest bullish catalyst in history. This is not only me who is talking about this. Two major voices are already making this argument.

Cathie Wood = Deflationary Disorder

At Bitcoin Investor Week (February 2026), ARK Invest CEO Cathie Wood argued that Bitcoin is a hedge not just against inflation but against a coming wave of technology‑driven, productivity‑led deflation.

“If these technologies are so deflationary, it is going to be tough for the traditional world, hmm, used to 2% to 3% inflation, to adjust,” Wood said. They will have to embrace these technologies faster than expected”.

She warned that the Fed, relying on backward‑looking data, “could miss this and be forced into a response when there is more carnage out there”.

In that scenario, Bitcoin’s decentralized design and fixed supply become strategic advantages. “Bitcoin is a hedge against inflation and deflation,” Wood said. “The confused part of this is disruption all over the place”.

Joe Burnett = $11 million by 2036

Joe Burnett, Vice President of Bitcoin Strategy at Strive (Nasdaq: ASST), published a report projecting Bitcoin will reach $11 million per coin by Q1 2036, with AI‑driven deflation serving as the central mechanism.

Burnett‘s argument: AI-powered automation will drive sustained price declines across goods and services, creating deflationary pressure. In a fiat system built on debt, that is destabilizing. Policymakers will expand the money supply to prevent a deflationary spiral, steadily inflating the value of scarce assets.

“As AI drives real‑economy deflation, central banks and fiscal authorities expand liquidity to prevent a deflationary spiral,” Burnett wrote.

My opinion: Burnett‘s model assumes Bitcoin captures roughly 12% of total global financial assets by 2036. It currently accounts for about 0.2%. That is a 176‑fold increase. The implied CAGR of about 53% has historical precedent; Bitcoin averaged 60% CAGR from 2015 to 2024.

The Synthesis?

Below, I have explained how these pieces fit together:

| Phase | What Happens | Bitcoin Impact |

| Phase 1 (Now – Q3 2026) | AI displaces workers → defaults spike → banks bleed | Bitcoin drops to $55‑65k |

| Phase 2 (Late 2026 – 2027) | Fed prints trillions to bail out banks | Bitcoin rallies to $100‑150k |

| Phase 3 (2028 – 2030) | AI productivity gains accelerate → structural deflation | Bitcoin becomes the only safe haven → $250k‑540k |

| Phase 4 (2030 – 2036) | Central banks print perpetually to fight deflation | Bitcoin captures 10‑15% of global assets → $1.5M‑11M |

Finance Ideas TL; DR | Tapos Kumar

Arthur Hayes argues AI is displacing knowledge workers at scale, causing consumer credit defaults and a banking crisis. The Fed will print money sooner or later to stop it, but not before Bitcoin drops first. His framework: AI deflation → credit crisis → bank losses → Fed prints → Bitcoin moons. Then, what is the problem? The “drop first” part is happening right now.

Download Free Pdfs resources without E-mail

Frequently Asked Questions (FAQ) about Arthur Hayes AI deflation Bitcoin?

Why does Hayes think AI is a bigger threat than the Fed?

This is because the Fed’s actions are a response to AI. AI is the cause. Most analysts focus on rates. Hayes focuses on labor markets and credit, where the actual damage is happening.

Does Cathie Wood agree with Hayes?

Yes and no. She agrees AI will cause “deflationary chaos” and that Bitcoin is a hedge. But she is more bullish sooner, arguing the Fed is already behind the curve.

Is this different from past crypto winters?

Yes. Past winters were driven by Fed rate hikes or exchange collapses. This one is driven by structural labor displacement. That means the recovery could be slower, but the ultimate upside could be larger because the money printing will be bigger.

What happens to altcoins in an AI deflationary scenario?

Hayes predicts most Layer 1 blockchains outside Ethereum and Solana will fail. He is called out specifically by Monad for a significant price correction. Stick with Bitcoin, Ethereum, Solana, and maybe hype.

Should I buy AI‑related crypto tokens instead?

Hayes warns against it. AI crypto tokens are speculative and unproven. In a credit crisis, they will get crushed first. He said that Bitcoin is a haven within crypto.

How does the Iran war fit into Hayes’s AI thesis?

Two separate forces. AI is structural (long‑term). Iran is geopolitical (short‑term). Both are keeping Bitcoin in the “no‑trade zone” like AI by destroying jobs, and Iran by creating commodity uncertainty.

What is the move index, and why does Hayes watch it?

The MOVE Index measures volatility in the US bond market. When it rises above 130, it signals stress in the Treasury market, which historically forces the Fed to intervene with liquidity.

Could the Fed refuse to print and let banks fail?

Hmm, politically not likely. The 2023 regional bank failures showed the Fed will backstop the system.

How does liquidity affect the 2028 Bitcoin halving?

Hayes argues the four‑year halving cycle is dead. “Liquidity now runs everything,” he says. The halving will reduce supply, but macro liquidity will determine price.

What is the one chart I should watch?

US consumer credit delinquency rates (credit cards, auto loans, personal loans). When they spike above 2010 levels, the AI default wave has begun. That is your signal that the Fed is about to print.

Is this article fear‑mongering?

No. It explains a framework that one of crypto’s most successful traders is using right now. Hayes isn’t selling. He is just not buying. And that is a signal, not a prediction, in my view.

Tapos’s last thought

Hayes is not buying. So, you shouldn’t buy aggressively. Let me tell you what you should consider.

The Hayes Strategy

- Do almost nothing. Hayes‘s fund did minimal trading in Q1 2026 beyond slowly increasing its long position in Hyperliquid (HYPE).

- Wait for the Fed to print

- Buy when banks start failing. That is the signal that money printing is imminent.

- Hold gold and select altcoins in the meantime. Hayes has been adding only to gold and hype.

My recommendations for you

| Investor Type | Strategy |

| Short‑term trader | Stay in cash or stablecoins. Trade ranges ($68‑78k) with tight stops. Don ‘t fights the “no‑trade zone.” |

| Medium‑term swing trader | Wait for $60‑65k. That is your first entry. Add more if we hit $55k. |

| Long‑term holder (3+ years) | Dollar‑cost average now, but keep dry powder for $55‑60k. The 2030 thesis ($250k‑540k) is intact. |

| Aggressive (high risk tolerance) | Watch the move Index (bond volatility). Hayes says when it rises above 130, money printing will occur. That is your signal to go long. |

Then, watch these 3 signals:

- Fed balance sheet expansion with rate cuts. Hayes calls stealth QE through “Reserve Management Purchases” the real liquidity driver.

- Bank earnings reports, yes, watch for rising consumer loan loss provisions. That is the AI default wave materializing.

- Unemployment claims among professional services (tech, finance, legal). A sustained spike above 300k weekly is the canary.

Last advice: You should sit on 40% cash, 40% Bitcoin, 20% gold. No new Bitcoin purchases until we see $62k or Fed capitulation. This will help you sleep well.

References & Sources

Below is the lists of sources that I have used to write this article:

- BLS Employment Projections (2024‑2034) – Official US labor forecasts

- Artificial Intelligence: OMB Action Needed to Address Privacy-Related Gaps in Federal Guidance

- S.Amdt.4109 – AI-Related Job Impacts Disclosure Amendment (to H.R.4016)

Disclaimer

This is not a Sponsored post & the purpose of this article is only education. By reading this, you agree that the information of this blog article is not crypto investing advice. Do your own research before making any financial decision. Therefore, if you lost any money, Finance Ideas will not be liable for this.